U.S. dividend-paying equities are one of the most hotly contested spaces for the development of indexes. However, I’d caution against generalizations that are too wide, because:

• U.S. dividend payers (as represented here by the WisdomTree LargeCap Dividend Index) as a whole have valuations that are broadly similar to those of the broad markets (as represented by the S&P 500 Index).

• Yet many dividend-focused indexes concentrate on a narrow slice of the broader equity market and miss certain dividend payers altogether.

• Dividend-paying stocks can be found in all corners of the market, from traditional high-dividend-yield “value ” oriented slices to the “growth ” segment of the market.

• I’d encourage the exploration of new growth-oriented segments of the dividend market, given the mix of current valuations and the expected growth potential.

Are Dividend Stocks Expensive?

Many question whether high-dividend-yield stocks are expensive due to investors’ flocking to dividend stocks with the current low interest rate environment. WisdomTree has a broad array of domestic equity Indexes consisting solely of dividend payers so we can address this question specifically for both large caps and small caps—as well as dividend stocks with greater growth potential relative to broadly inclusive indexes of dividend payers.

{kind=link}

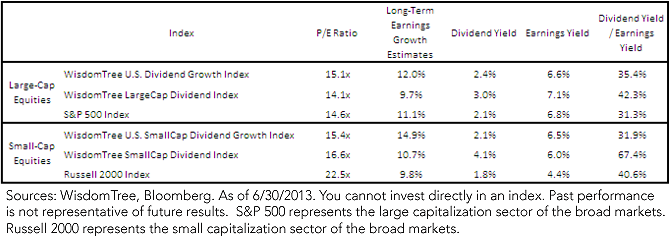

For definitions of terms and indexes in the chart, please visit our glossary.

Large-Cap Picture: The WisdomTree LargeCap Dividend Index, which includes the 300 largest regular dividend payers in the United States, has a lower P/E ratio than the S&P 500 Index, which does not consist solely of dividend payers. The WisdomTree U.S. Dividend Growth Index, which focuses on primarily large-cap, dividend-paying equities with growth characteristics, has a slightly higher P/E ratio than the S&P 500 Index, but it also has higher long-term earnings growth expectations as well as a higher dividend yield. In large-cap equities, it is therefore difficult to classify dividend payers—both broadly and those with growth potential—as “expensive,” if the baseline is the S&P 500 Index.

Small-Cap Picture: The WisdomTree SmallCap Dividend Index, which includes the bottom 25% of the market capitalization of the WisdomTree Dividend Index, has a lower P/E ratio than the Russell 2000 Index. The WisdomTree U.S. Small Cap Dividend Growth Index, which focuses specifically on those stocks in the WisdomTree SmallCap Dividend Index that have growth characteristics, also has a lower P/E ratio than the Russell 2000 Index, as well as significantly higher long-term earnings growth expectations. Similar to the large-cap picture, the picture of small caps as of June 30, 2013, makes it difficult to broadly classify dividend stocks as “expensive.”

We believe that the small-cap segment of the dividend-paying market deserves special attention. In addition to the highest long-term earnings growth expectations of any of the indexes in the chart, it is worth noting that these are the only two U.S. equity Indexes (the WisdomTree SmallCap Dividend Index and the WisdomTree U.S. Small Cap Dividend Growth Index) that focus solely on small-cap dividend payers1 . While the large-cap space is without question much more competitive, looking to the small-cap space may provide a diversification benefit at what we believe to be an attractive price.

Next page: Defensive sectors