Rob Arnott expressed an intriguing observation in an interview at IndexUniverse.com. The founder of Research Affiliates explained that the cyclically adjusted P/Es for U.S. stocks and for emerging market stocks are roughly 24 and 13 respectively.

At the previous bull market height of 2007, however, U.S. stocks were much cheaper than emerging market counterparts; at that time, U.S. stocks collectively chimed in with a cyclically adjusted P/E of 26 while emergers rang the bell at 37.

The Case-Shiller cyclically adjusted P/E (a.k.a. CAPE) uses a 10-year rolling average where inclusion of “outlier” data from the 2008-2009 financial collapse may distort the value of the metric. Indeed, the folks at Motley Fool estimated that current CAPE overstates S&P valuation by 38% when outlier data is removed. Yet the more important finding may be the fact that, with or without data adjustments, emerging market stocks may be sporting a sale price that is nearly 2/3 of the value commanded six years ago.

Slowdown fears and outright economic contraction concerns have adversely impacted funds like Brazil (EWZ), Russia (RSX), India (EPI) and China (GXC) for several years. Moreover, central bank policies in the developing world have been less stimulative than the policies of developed countries, causing many to back away altogether. In truth, those that have invested in up-n-coming regions over the last 12 months have more often felt the stabbing pain of the proverbial falling knife, not the the sweet sensation of biting into a Brazilian papaya.

{kind=link}

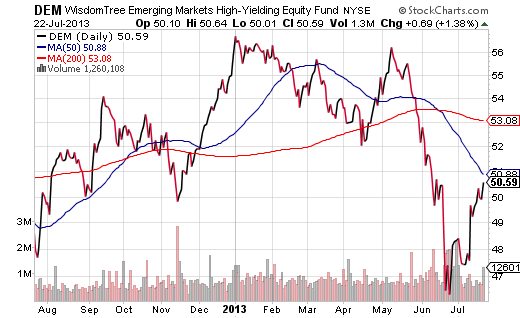

Nevertheless, some emerging market assets may finally be turning the corner. For example, iShares MSCI Malaysia (EWM) has produced a respectable 15% year-over-year. Its current price is holding above a 50-day and 200-day trendline. In addition, the 50-day intermediate term moving average has stayed above the longer-term 200-day; technical analysts see the development as noteworthy because a bearish “cross-under” has been avoided.