Recently, we shared our prediction that the US ETF industry could experience more than 100% growth in the next five years, from current assets of $1.5 trillion to $3.5 trillion by the year 2017.

There are several key drivers fueling this growth, including increased institutional usage, the growth of the self-directed investor market and the notable opportunity that exists in the fixed income (FI) category.

This last topic is something we’ve discussed at length on the iShares Blog. As more and more investors become comfortable with bond ETFs and, more importantly, aware of the benefits they can provide, we’re seeing a large increase in adoption on the FI side. In fact, bond ETFs now account for 17% of global ETP assets up from just 5% in 2005.

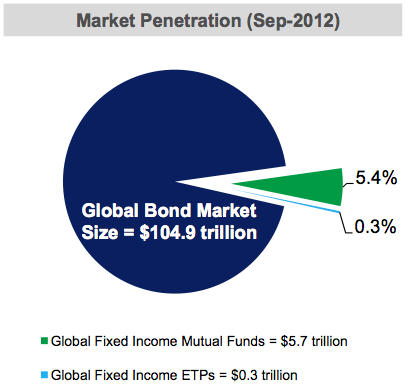

But even with this increased adoption, global assets in the FI ETF space only account for 0.3% of the underlying global bond market. You read that right – it’s really only 0.3%, and traditional mutual funds (which had a considerable head start) only weigh in at 5.4% (see below).

{kind=link}

So what exactly does this mean for current and future bond ETF investors? The first implication is that there is obviously a lot of runway for future growth, and as bond ETFs grow in assets there can be potential benefits for investors (increased secondary market liquidity, for example). In addition, we should continue to see the trend of ETF providers exploring uncharted territories in the bond market, allowing investors to gain new, different and precise exposures through an ETF vehicle.