Most cyclical asset prices fell after Fed Chairman Bernanke announced that the Fed, on certain conditions, projects an end to quantitative easing (QE) by the middle of 2014.

Prices of precious metals fell sharply as a hardening of QE removal expectations hit gold and silver prices, and platinum and palladium prices were pulled down by a broad-based sell-off of cyclical assets. A rebound of the US dollar exacerbated the sell-off. While tactical sentiment towards gold and silver prices will likely remain negative as long as interest rate expectations continue to rise and the US dollar continues to strengthen, there are reasons for contrarian investors to look favourably on precious metals.

At current levels gold, silver, platinum and palladium are estimated to be trading around or below their respective marginal costs of production. In addition, physical buyers at current prices – particularly of gold – have started to step in again. Short gold futures positioning on COMEX is at an all-time high and nearly every broker is now negative gold. Therefore, while further downside in the short-term is possible, investors with longer-term time-horizons may start to look at the recent sell-off as a longer-term accumulation opportunity.

Gold hit by rising tactical shorts, but opportunities open for contrarian investors. As long as the Fed continues to re-affirm its commitment to reduce QE in the coming months it seems likely that gold prices will remain weak. However, it is far from certain, in our view, that the US is on a sustainable recovery path. There is also little evidence of rising inflation and the US unemployment rate has declined largely because of a reduced participation rate rather than rapid growth of new jobs. As highlighted by the IMF, a substantial reduction in stimulus at this point in the cycle could prove to be premature. The more than doubling of US 10-year government bond yields to a 22-month high, the strength of the US dollar and reduced fiscal stimulus, risks dragging US growth sharply lower later this year. If this occurs, the Fed will likely step back from QE reductions. With gold positioning so negative, this has the potential to stimulate a strong short-covering gold price move.

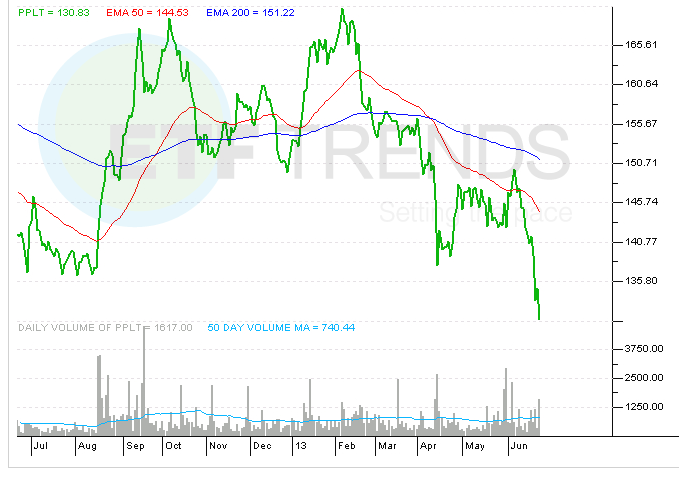

Platinum trades 25% below estimated marginal cost of production. Platinum and palladium prices also fell last week. However, unlike gold and silver, the main reason for their price declines is likely have been related to a general reduction by investors of “risky” cyclical assets in reaction to expected reduced liquidity injections by the US Fed later this year. In our view, however, to the degree that the Fed ultimately reduces its easing policy because of continued recovery of the US economy (though we have our questions about this scenario, as highlighted above), both platinum and palladium should benefit. On our analysis, the marginal cost of production of platinum is around $1,800/oz. With platinum now trading at a 25% discount to this level, without a substantial price rally, producers will likely continue to scale back production of both platinum and its by-product palladium.

ETFS Physical Platinum Shares (NYSEArca: PPLT)

{kind=link}