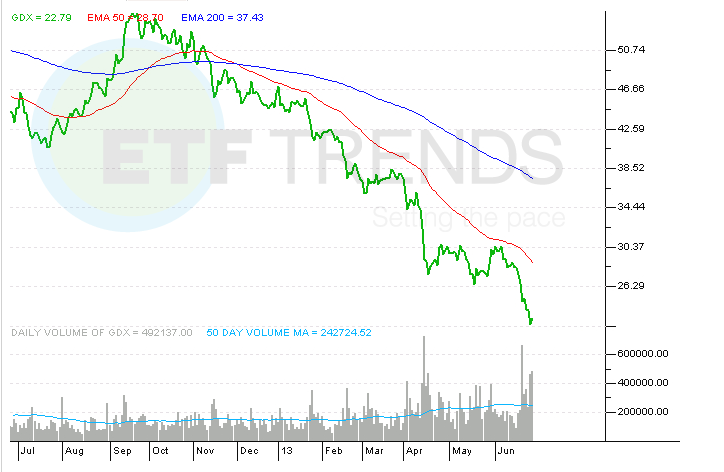

This is how bad things have been for gold mining ETFs in the second quarter: The group’s largest fund, the Market Vectors Gold Miners ETF (NYSEArca: GDX), is up 7.1% on above-average volume Friday and even with that, the fund will see a loss of more than 30%.

Some of the other mining ETFs that were taken to the woodshed in the second quarter, such as the Market Vectors Junior Gold Miners ETF (NYSEArca: GDXJ) and the Global X Silver Miners ETF (NYSEArca: SIL), are also enjoying fantastic Friday performances. However, investors should be cautious because these bounces may be of the dead-cat variety. [Miner ETFs Take a Header]

Barrick (NYSE: ABX) is trying to sell assets to raise cash and that comes after the company sold $3 billion worth of bonds in April. The company had $12.5 billion of net debt as of March 31, report Liezel Hilll and Cecil Gutscher for Bloomberg.

Gold Fields (NYSE: GFI) told Bloomberg the “industry is not sustainable at $1,230 an ounce” while adding “We’re going to need at least $1,500 an ounce to sustain this industry in any reasonable form.”

Bloomberg notes that corporate bonds from miners such as Barrick, Goldcorp (NYSE: GG) and Kinross (NYSE: KGC) have been trading like junk bonds although those companies have investment-grade ratings. Along with Goldfields, those stocks represent about a third of GDX’s weight. [Gold Miner ETFs Eye 2008 Lows]

Miners being at risk of only breaking even, or worse, losing money on production comes as the industry has been under pressure to be more transparent about its output costs. Earlier this week, the World Gold Council released new guidelines that will force miners to reveal to shareholders a more telling picture about production costs.

A lack of uniformity in terms of reporting costs has scared some investors away from the sector. For example, gold miner ABC Inc. may report net cash costs while miner XYZ Corp. may only report costs related to realized sales.

The World Gold Council wants miners to report “all in” costs, which include a wider range of factors such as permitting fees, royalties and related fare.

When gold prices were soaring, miners were not under as much pressure to reveal their true costs of doing business. Now with gold clinging to $1,200 an ounce and production costs for many miners believed to be in the $1,100 to $1,200 an ounce range, share price declines are revealing miners’ costs whether the companies like it or not.

Market Vectors Gold Miners ETF

{kind=link}

ETF Trends editorial team contributed to this post.

The opinions and forecasts expressed herein are solely those of Tom Lydon, and may not actually come to pass. Information on this site should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product.