In a recent blog, we detailed our bullish views on the Asia Pacific ex-Japan region, given how a historical analysis showed a favorable return environment following similar price points in the past.

In this piece, we conduct a similar analysis for Australian equities (MSCI Australia Index)—a major developed country in this region. Australia is currently noted for two key attributes:

- Natural Resources: Australia is rich in natural resources, and this fact, combined with a close proximity to China, creates an important economic relationship between the two countries. Australia can supply a significant proportion of China’s demand for these resources.

- Strong Sovereign Balance Sheet: Australia is one of a dwindling number of developed market countries currently maintaining a AAA credit rating from Standard & Poor’s2, partly due to a debt-to-gross domestic product (GDP) ratio of less than 30%, according to the International Monetary Fund’s October 2012 estimates.

Australian equities have outperformed Asian equities (represented by the MSCI AC Asia Pacific ex Japan Index) by over 10% for the last 12 months (as of 2/28/13).

Looking at historical valuations of Australian equities, we conclude that Australian equities are currently selling at relatively low valuations based on historical ranges (which matched our findings for Asian equities in the prior blog), as we will detail in the historical analysis below. [Australia ETFs: Downgrading Down Under]

{kind=link}

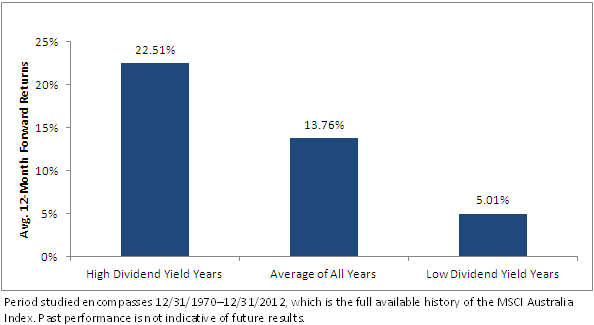

- The current trailing 12-month dividend yieldfor February 28, 2013, is 4.00%, while the median value for all 42 available year-end values for the MSCI Australia Index is 3.71%. Year-end values above this figure were classified as High Dividend Yield Years, and those below this value were classified as Low Dividend Yield Years. This means we are currently in a high dividend yield period relative to the history of Australian equities.

- The average return for High Dividend Yield Years was more than 17% better than the average for Low Dividend Yield years, and nearly 9% better than the average of all 42 available calendar years. Of course, there is no guarantee that this result will repeat itself, but we believe it worth mentioning, especially since it is based on more than four decades of return history.

Particular Risks in Focus: Financials & Materials

While we have outlined a way to look at Australian equities from a positive perspective through the use of the MSCI Australia Index, many might cite the heavy exposure of that Index to financials (49.02%) and materials (21.08%)2. While the index is weighted by market capitalization, WisdomTree has created an Index specifically geared to counter the potential sector concentration risk of weighting Australian firms on the basis of their market capitalizations. Instead, the WisdomTree Australia Dividend Index weights the 10 largest qualifying companies from each of the industry sectors on the basis of their dividend yields, resulting in a combined weight to the Financials and Materials sectors of less than 35%3.

Australia’s Currency