For a little more than a year, I’ve been advocating a long-term overweight to Australian equities as part of my preference for smaller, developed “CASSH” (Canada, Australia, Switzerland, Singapore and Hong Kong) countries that exited the financial crisis in far better shape than Europe, Japan or even the United States.

Since the start of 2012, this view has generally worked well. Australian equities – as measured by the S&P/ASX 200 index – are up more than 16% from 12 months ago.

Now, however, all is not so well down under. While I’m maintaining my neutral near-term view of Australia for now, here’s why I’m closely watching the market for a possible downgrade.

- Australia is not as cheap as it was six months ago. Australian equities are trading for nearly 2x book value. While this represents a discount to US stocks, Australia is now trading at a premium to most developed markets.

- Growth remains soft. Australia has been hurt by falling commodity prices, particularly for iron ore. This drop in prices has had a negative impact on Australia’s terms of trade and has undermined the country’s business investment and household income. As such, in its recent statement, the Reserve Bank of Australia (RBA) downgraded its 2013 growth outlook to 2.5% from 2.75%.

- Australia has become a two-speed economy. Australian monetary policy has become complicated by the fact that the country’s mining sector is growing at a very different rate than the rest of the economy. After an aggressive round of rate cuts, the RBA is now taking a pause to determine if its recent policy easing will be sufficient to ensure a pickup in the non-mining sector.

- Australia has an over indebted consumer. One factor holding back the non-mining portion of the economy: too much consumer debt. Much like US consumers, Australian consumers are in the process of repairing their balance sheets. As this process unfolds, consumption will remain soft.

To be sure, for investors focused on the longer term, Australia still has many factors in its favor. The country has an exceptionally low debt burden, a budget close to balanced, a profitable corporate sector and a sustainable pension system. In short, like its other CASSH counterparts, Australia suffers from fewer long-term economic imbalances than the United States, Europe and Japan. In addition, thanks to its large banking sector, Australia offers the second highest dividend yield among developed countries. In light of the country’s benign inflation outlook and attractive budget situation, Australia still has more monetary and fiscal policy flexibility than many other developed markets.

But for shorter-term investors, Australian equities look pricey considering the four factors I cite above. As such, until I see cheaper prices or better growth prospects down under, I advocate maintaining a benchmark weight to the Australian market. In addition, I’m closely watching Australia’s growth estimates and reports. Any further softness would lead me to downgrade my near-term view of the country’s stocks.

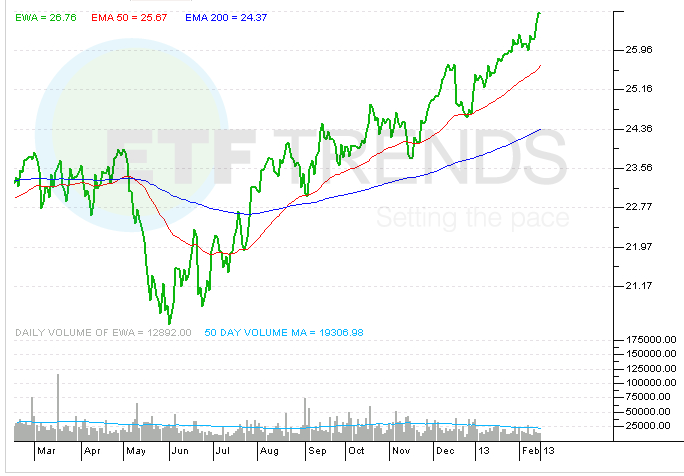

iShares MSCI Australia (NYSEArca: EWA)

{kind=link}

Russ Koesterich, CFA, is the iShares Global Chief Investment Strategist.