With 2012 in the rear view mirror, our team has been getting a lot of questions from clients who want to know how the various bond sectors fared for the year – and what we can learn from this information.

Concerns such as rising interest rates, credit issues in municipal bonds and a Greek default all drove investor behavior throughout the year.

While some of these events did come to pass, how did the reality of bond sector performance match up with investor fears?

We took a look at the most well-known fixed income sectors to find the three biggest surprises in bond returns last year.

{kind=link}

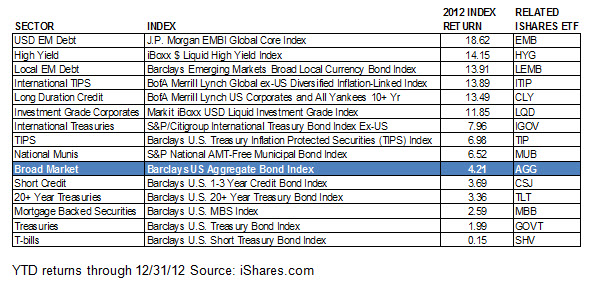

- Long duration. As the great “interest rate debate”raged on, investors spent much of the past year avoiding longer duration bonds, fearing that a sudden rise in rates would wipe out their value. However, rates continued to fall (not rise) and longer duration indexes actually outperformed their shorter duration counterparts.Risky assets, particularly emerging market bonds and high yield, also benefited from the low interest rate environment. Both sectors experienced double digit returns as investors flocked to them as a source of yield and diversification. The returns attributed to the high yield market were primarily due to declining credit spreads, which went from 6.99% to 5.11% by the end of 2012. Credit spreads are a measure of the additional amount of yield the market demands for taking on the credit risk of the issuer. When credit spreads decline, the market is anticipating less concern about credit risk and, as a result, bond prices on credit risky bonds generally rise.

- Munis. While some municipalities did have defaults (including some California cities), most muni bonds continued to perform well. Broad national municipal bond indices, such as the S&P National AMT-Free Municipal Bond Index, returned 6.52% in 2012. Demand was strong for municipal bonds as investors were looking for tax efficient income.

- International. As for Greece, we did see many investors avoiding European bond exposures due to the country’s default and ongoing funding concerns for the other periphery countries. But the broader international treasury index, which includes about 55% eurozone exposure, returned 7.96% in 2012. Even with a Greek default, international treasuries had strong returns as rates fell from distressed levels.

So despite the concerns, all of these ‘troubled’ sectors actually fared better than expected for the year. In fact, munis and international bonds actually beat the broad fixed income market at 4.21%. Not surprisingly, low yielding, traditionally safer havens like T-bills and US treasuries were the bottom performers for the year.

The lesson here? Surprises in investing may be inevitable, but some generally accepted rules of thumb – such as the importance of diversification and the costs of hiding in less risky assets – can help investors navigate those surprises.

Karen Schenone is a fixed income strategist at BlackRock Financial Management.