I believe that 2013 promises to stand in contrast to the linear upward moves for municipal bonds in 2012. There appears to be conflicting expectations about new issue supply, so my conservative view is to say that volume has the potential to be +/- 10% of that of 2012.

Much depends on a solution out of Washington concerning taxes, entitlements and federal support for state and local government programs.

My outlook anticipates that municipal bond tax exemption should remain in place for individual investors and allow municipalities continued access to the capital markets, as has been customary since the early 20th century. The uncertainty includes a possible return to stimulus, such as the Build America Bond program.

Even if some of the tax benefit was capped at 28%, the muni market already seems to be anticipating higher nominal rates in the second half of 2013, and an adjustment could happen very suddenly if new legislation regarding muni tax exemption is passed.

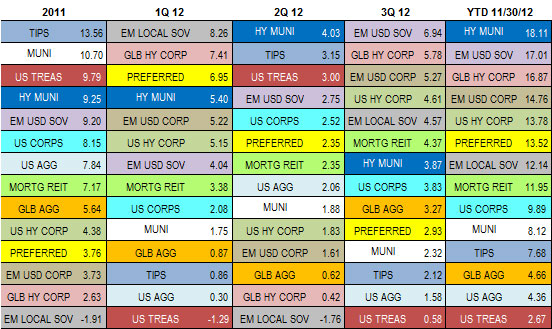

This year was more profitable for muni investors than was predicted at the beginning of the year. Year-to-date index returns of 8.12% for the Barclays Municipal Bond Index and 18.11% for the Barclays Municipal High Yield Index summarize a story that includes spread narrowing, curve flattening and large inflows to municipal funds (nearly $50 billion YTD). Though there were more credit downgrades than upgrades, I believe 2012 will deliver fewer defaults or credit impairments than the prior two years. [Muni ETFs Extend Losing Streak on Tax Jitters, Bond Flood]

Overall, I believe municipals will continue to offer investors potential opportunity in terms of yield and return in 2013. However, there may be less of a total return opportunity than we’ve seen in 2012, since quality spreads have narrowed throughout 2012 and the curve could flatten in a meaningful way in the 1–10 year segment.

Historical Fixed-Income Index Returns (%)

{kind=link}

James Colby is a portfolio manager and senior municipal strategist at Market Vectors ETFs.