In the aftermath of Hurricane Sandy, more than just the massive property destruction has been revealed to municipal participants as needing dire attention. National and local infrastructures have been weakened and are at the mercy of natural disasters that now seem to be occurring more regularly.

From power supply and transportation to drinking water, Sandy exposed most of the projects and programs that constitute “public purpose” and define municipal finance as damaged and in need of repair.

After Wednesday’s announcement of the resignation of the chief operating officer of the Long Island Power Authority, New York Governor Andrew Cuomo commented, “I believe LIPA has been beyond repair for a long, long time. I don’t believe you can fix it. I believe it needs to be overhauled and you need a new system.” This is only the beginning of what I believe promises to be a contentious period for governors and regional managers alike. In the Mid-Atlantic, where over 8 million customers throughout 21 states lost power, there will be a need for restoring infrastructure. In my opinion, traditional tax-exempt financing supplemented with proceeds from insurance and federal grants will likely fund reconstruction.

If that sounds like business as usual, think again. This nation’s economy still appears to be teetering on the edge. Unemployment is currently at 7.9%, business formation and investment are low, the fiscal cliff looms and Washington lawmakers are toying with reducing, if not eliminating, the tax-free advantage of municipal bonds. At a time when municipalities need every opportunity to continue to access the capital markets, the possibility of higher financing hangs overhead.

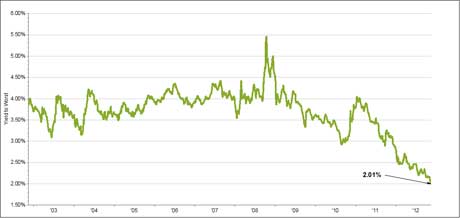

I see the municipal market at a crossroads. Order is needed but confusion seems close at hand. Yields are at or close to all-time lows just when confidence in the process needs affirmation rather than undermining. With year-to-date returns above 7%, municipal bonds generally have performed better than expected. Now is not the time to pull the plug. And, if recent flows into municipals are any indication, investors have not yet lost the desire for this asset class.

{kind=link}

Source: FactSet, as of 11/14/12. Based on yield-to-worst of the Barclays Municipal Bond Index.

The Barclays Municipal Bond Index is considered representative of the broad market for investment grade, tax-exempt bonds with a maturity of at least one year. Yield to Worst measures the lowest of either yield-to-maturity or yield-to-call date on every possible call date.