In September, most of the world’s major central banks doubled down on their bet to suppress long-term rates. With yields close to historic lows, and in many cases below the level of inflation, many investors responded by turning to high yield.

Indeed, I have argued that in this environment fixed income investors have no choice but to either accept lower income or more risk and given that, investors should consider focusing on credit risk rather than duration.

I still believe that marginal credit risk makes sense, particularly for aggressive yield-hungry investors, but the recent rally in high yield suggests that downside risks may be starting to outweigh the potential benefits. [High-Yield ETFs: Rotation from Junk to Quality]

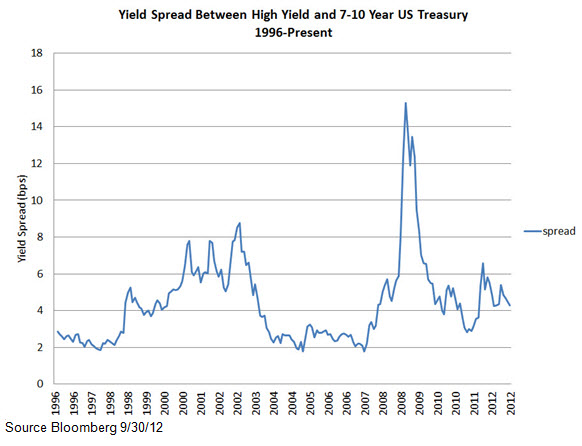

Since the spring, the spread between the Barclays High Yield Index and the 10-Year Treasury note has narrowed from 608 basis points at the end of May to 475 basis points today:

{kind=link}

The rush into high yield and the contraction in spreads is understandable. In a “low-for-long” environment yield hungry, fixed-income investors have few other alternatives. In addition, many investors who would typically have a higher equity allocation have opted for “equity light” exposure through high yield. That said, the recent rally in fixed-income has pushed spreads well below their long-term average – 535 basis points – and to their lowest level since July 2011.