Given that Treasury yields are at multi-decade lows as a result of deflation fears and the Federal Reserve’s open market operations designed to keep interest rates where they are, one might expect investors to start piling into higher yielding sovereign debt.

For those that have, it appears as though the trend still favors positioning into U.S. government paper as opposed to sovereign issues.

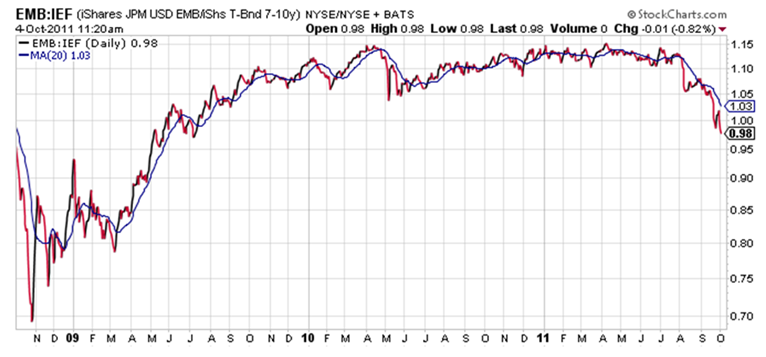

Take a look below at the price ratio of the iShares JPMorgan USD Emerging Markets Bond Fund (NYSEArca: EMB) relative to the iShares 7-10 Treasury Bond Fund (NYSEArca: IEF).

As a reminder, a rising price ratio means the numerator/EMB is outperforming (up more/down less) the denominator/IEF. A falling ratio means the opposite, whereby the numerator/EMB underperforms the denominator/IEF.

Chart source: StockCharts.com.

{kind=link}

The ratio collapsed in early August as the summer crash of 2011 I had been calling for as early as June occurred. [Summer Stock Crash]

Effectively, yields rose in sovereign debt while Treasury interest rates dropped at the same time in a classic flight to safety trade. The reasoning for the weakness may be because of contagion concerns over a default in Greece affecting more than just Europe, but Brazil, Mexico, Russia, Turkey, and the Philippines, which make up over 37% of the ETF’s country holdings.