With the tremendous volatility markets have experienced over the past few months, I am often asked for my thoughts on where equities will go next. In truth, I am still bearish given the still strong deflationary message the bond markets are signaling independent of expectations of further quantitative easing, or QE3, from the Federal Reserve.

However, I do think that if one wanted to position into equities, it might be worth considering that on a relative basis emerging markets, and in particular China, may give the most outperformance potential in the near term.

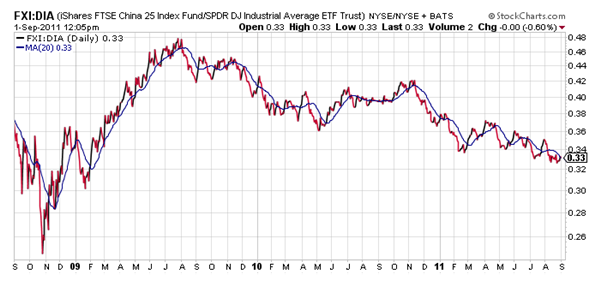

Take a look below at the price ratio of the iShares FTSE China 25 Index Fund (NYSEArca: FXI) relative to the SPDR Dow Jones Industrial Average ETF (NYSEArca: DIA). As a reminder, a rising price ratio means the numerator/FXI is outperforming (up more/down less) the denominator/DIA.

Chart source: StockCharts.com.

{kind=link}

There are a few things I’d like to point out here. First, while the ratio bottomed in late October 2008 and powerfully outperformed the U.S. in the early part of 2009, the great economic powerhouse topped out all the way back in July of 2009, underperforming the Dow for the next two years.

The ratio appears to be bottoming out now, and could be on the verge of a strong outperformance move. Note that this ratio can still trend higher even in a bear market – it just means that China may go down less or even up slightly in a declining equity environment, depending on the magnitude of the outperformance.