This year’s introduction of the U.S. Treasury’s floating rate notes (FRNs), which may help investors limit interest rate risk without credit risk, are currently yielding, on average, approximately 0.10%, as of April 23, 20141.

For investors seeking the low interest rate sensitivity found with FRNs, but who may have a tolerance for investment-grade corporate credit risk, the floating rate notes found in Market Vectors Investment Grade Floating Rate ETF (FLTR) may offer an alternative option with a yield of about 0.80%, based on its underlying index, Market Vectors US Investment Grade Floating Rate Index2 (MVFLTR Index).

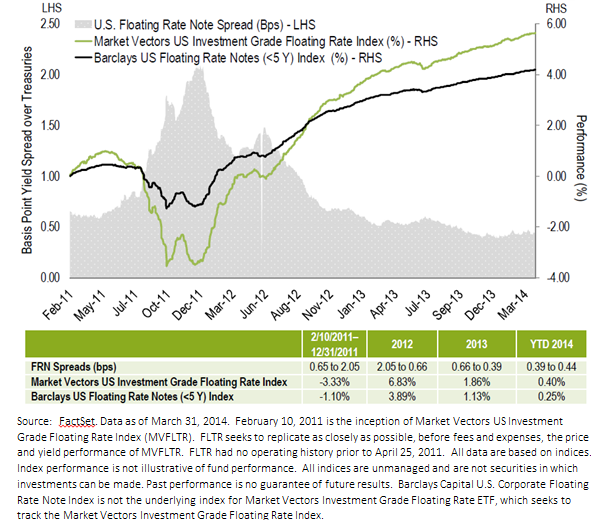

MVFLTR Index comprises corporate FRNs and is constructed with an allocation bias to notes slightly further out on the maturity curve. While its average years to maturity does not affect interest rate duration3 because of the FRN coupon-adjustment feature, it generally results in slightly higher credit spread duration4 than do other corporate floating rate note indices, which may also include government agency FRNs, as found with the Barclays US Floating Rate Notes (<5 Y) Index5.

FRN Index Performance

2/10/2011 – 3/31/2014

{kind=link}

As a result, MVFLTR Index has provided higher total returns during stable or improving credit markets, since January 2012 for example, but also underperformed when credit spreads widened, as in times of economic stress seen in 2011.

For an investor with a constructive outlook on the economy and who may be expecting short-term interest rates torise as a result, FLTR may be an option to consider for higher relative yield compared to government and shorter-maturity FRNs.

Investment grade corporate floating rate notes are sometimes mistaken for floating rate bank loans, which are otherwise known as leveraged loans, and are collateralized, floating rate, sub-investment grade bank loans. Corporate floating rate notes are investment-grade securities that trade just like other corporate bonds and notes.

Each of these asset classes helps limit interest rate risk by paying a floating rate of interest, typically tied to a Libor6 rate, plus additional margin for credit risk.

Alternatively, the U.S. Treasury floating rate notes are sans credit risk, and are also available through recently launched exchange-traded funds (ETFs). However, investors seeking access to Treasury FRNs may have larger yield appetites than this instrument may be able to offer.