As investors and analysts seek to explain the negative performance in emerging market assets, most have centered their focus on external vulnerabilities, particularly current account (C/A) balances, international reserves and portfolio flows.

As part of our discussion, we would like to not only present current data but also explain why investors should pay particular attention to the current account balance, especially in developing economies.

For most investors, discussions about a country’s current account balance appear to fall more in the realm of monetary economists and academics than of asset allocators and portfolio managers.

Unfortunately, in today’s global environment, focusing on the details can matter a great deal to your portfolio’s bottom line.

Why Does a Country’s Current Account Balance Matter?

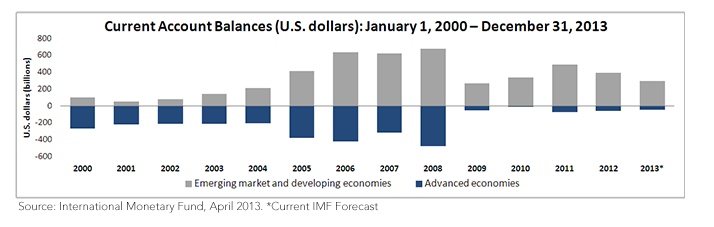

Before jumping into the data, it may be useful to take a step back and review what the current account actually measures or implies. Essentially, the current account represents the difference between the value of the exports of goods and services and the value of the imports of goods and services. Put more simply, is a country buying more goods from abroad than it is supplying to global markets? The reason why investors and analysts are concerned about expanding current account deficits is that—as is the case for nearly all imbalances—eventually they will have to normalize, and potentially in a destabilizing way. This occurs because the balancing entry for a current account deficit is generally a capital account surplus, which essentially means borrowing from abroad to finance current consumption (more imports, fewer exports).

If recent history has taught us anything, it is that credit-fueled consumption is unsustainable in the long run. Exports still account for the majority of the gross domestic product (GDP) of emerging markets (EM), and domestic consumption is likely not yet large enough to maintain attractive rates of growth, should exports decline. This has the potential to cause economic stress—the exact opposite of what creditors want to see when making the decision to lend. And what happens if short-term financing dries up? Investors rush for the exits, magnifying these external vulnerabilities and putting pressure on the country’s currency and local asset markets.

{kind=link}

The Macroeconomic Double Standard