Of all the investment topics I’ve discussed with clients, whether to invest in gold usually elicits the most divergent opinions. As an investment that is almost impossible to value, people’s views on gold are often more a matter of philosophy than empirical fact. But for better or worse, following the most dramatic sell-off in years, gold’s role in a portfolio is back in focus.

From the close on April 9th through the close on the 15th gold prices sank by more than 17%. Since the 15th gold prices have stabilized, with some evidence of fundamental buying entering the market. Investors unnerved by the sell-off are asking if this is the time to sell, while those who have been waiting for an opportunity to get into the market are asking if this is the right time to buy. Here’s my take:

- Talk of value in the gold market is meaningless. Among all the asset classes gold is particularly hard to value given, as is the case with other commodities, there is no cash flow to discount. In addition, there is little industrial demand for gold.

- Historically, a little gold has improved a portfolio. What we do know, however, is that at least historically there has been some benefit in holding small amounts of gold — around 1% to 2% — in a portfolio. As a physical asset and an historic store of value, gold tends to behave differently than paper assets and helps to diversify a portfolio.

- The correlation between gold and stocks is falling. The diversification benefits of gold have increased over the past year. For much of the post bubble period, gold, along with other commodities, often moved in tandem with stocks. This was the “risk-on” trade. As recently as last September, the correlation between physical gold and the S&P 500 was over 0.5 (based on trailing one-year of weekly data). This correlation was extremely high by historical standards. Today, with more differentiation in markets, the correlation has dropped back down to near zero. While gold prices are struggling, at the very least the asset class is once again offering some real diversification.

- All else equal, central bank buying is supportive of gold. Another consideration is that while gold is hard to value, it has performed better in certain environments. Historically, gold has done best when real or inflation adjusted interest rates are low to negative, as they are today. The reason is: when real rates are low there is less of an opportunity cost, in the form of foregone income, to holding gold. To the extent central banks, including the Fed and BOJ, maintain an accommodative monetary policy; all else equal this should be supportive of gold.

Our view is that investors, who include gold in their portfolio for diversification reasons and as an inflation hedge, should maintain that position, and for long-term investors a small allocation to gold could be reasonable. While there is no objective method to deciding if gold is “cheap” or “expensive” at these levels, following the sell-off the metal is obviously a bit cheaper to own.

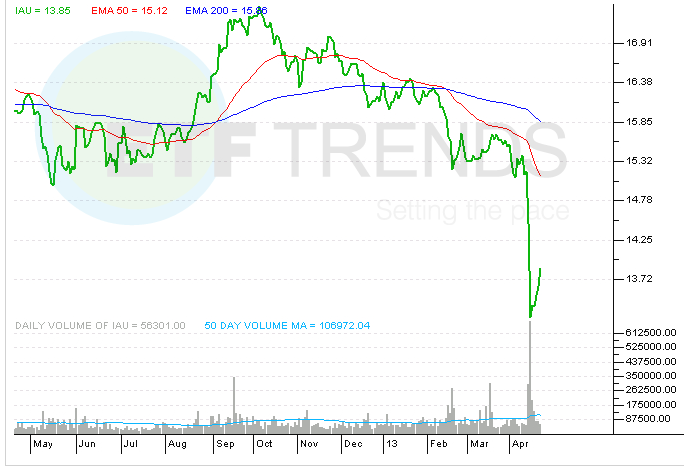

iShares Gold Trust (NYSEArca: IAU)

{kind=link}

Russ Koesterich, CFA, is the iShares Global Chief Investment Strategist.