I have written previously about the signs that investors can watch for to get an idea of when interest rates may be headed higher. One of these signs is a change in bond purchase patterns by central banks such as the Federal Reserve.

At last week’s meeting the Fed announced that the Fed Funds rate would remain low and that it would continue with its bond buying program, commonly referred to as Quantitative Easing, or QE.

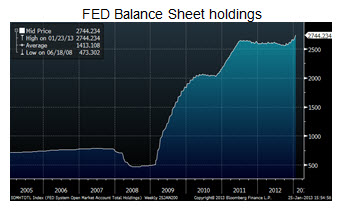

As the Fed continues its purchases and its holdings of fixed income securities grows, many investors are wondering what will happen when the Feds stance changes.

They are wondering what happens when the Fed not only stops buying bonds, but also starts raising rates and selling the bonds that it currently hold?

Here is a snapshot of just how big the Fed’s balance sheet — or their holdings of bonds and other securities — has become:

{kind=link}

A recent paper by researchers at the Fedsuggests that when the Fed does start to enact tighter monetary policy that it will move in a series of steps as outlined below. (Keep in mind that the paper was written by researchers at the Fed and may not reflect the views of the Board of Governors, which sets monetary policy.)

1) Stop reinvesting the maturing principal from the bonds it currently holds

2) Communicate new guidance on the Fed Funds Rate out to the market

3) Begin raising the Fed Funds Rate