According to some recent analysis by our marketing team, our clients are less likely than average to open emails that have the word “tax” in the subject line. I thought about that fact when writing the title of this post – if people knew that the topic was tax efficient investing, would they be less likely to continue reading?

It’s understandable to have a strong aversion to the T-word, especially if you’re still reeling from the bill you had to pay last April 15th. But that’s exactly why it’s better to address tax efficiency head-on and year-round, rather than waiting for a certain time of year when, frankly, it may be too late to do anything about it. If you’re not consistently investing with an eye toward tax efficiency, chances are there’s a “hole” in your investment bucket.

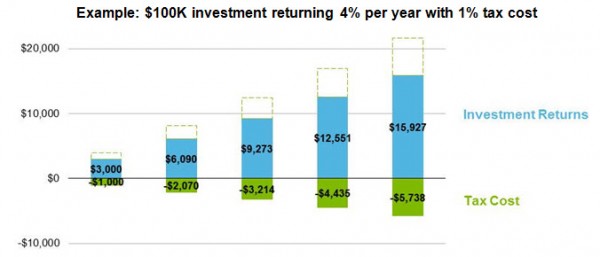

Simply stated, taxes can have quite a negative impact on your portfolio’s return. Just look at the illustration below, which shows the hypothetical growth of a $100,000 portfolio returning 4% per year. Even a relatively conservative 1% tax cost can cause leakage in returns, preventing you from keeping more of what you earn.

{kind=link}

So how do you go about patching that hole in your bucket? First and foremost, it’s important to understand that not all investments are created equal from a tax-efficiency standpoint. This is where many ETFs can have an advantage, because if they’re benchmarked to an index, the portfolio turnover tends to be relatively low. The less selling that goes on in the fund, the fewer the opportunities for capital gains to be realized.