If you’ve been following the news this year about exchange traded products (ETPs), you’re already aware that a big theme has been the significant growth the industry has experienced, particularly in the fixed income space.

Bond ETPs are driving industry flows now more than ever, garnering a 30% share year-to-date through September. This growth has driven ETPs to post their strongest year-to-date inflows in history.

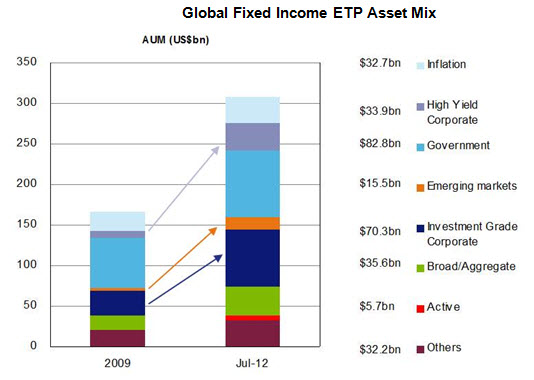

Within the fixed income category, it’s interesting to see how the ETP asset mix has evolved over time – and how it tends to reflect current market and economic conditions. For example, since 2005 we’ve seen a shift from government bond and inflation-related securities (such as Treasury Inflation Protected Securities, or TIPS) to riskier assets like high yield and investment grade corporate bonds (see below).

Given the current low-yield environment, it’s no surprise to see investors being willing to take on more risk in an attempt to reach income objectives. [Emerging Market Bond ETFs for Yield, Diversification]

But what may come as a surprise is the upward trend we’ve seen in emerging market (EM) bond ETP inflows so far this year.

{kind=link}

In fact, this has been building for quite a while – as you can see in the chart below, starting in January 2010, inflows for EM bond ETPs have been mostly positive on a monthly basis. The category has taken in over $6bn in net new assets already in 2012 and now accounts for 5% of the fixed income ETP universe, up from less than 2% going into 2010.