![]()

Source: Bloomberg, Accuvest

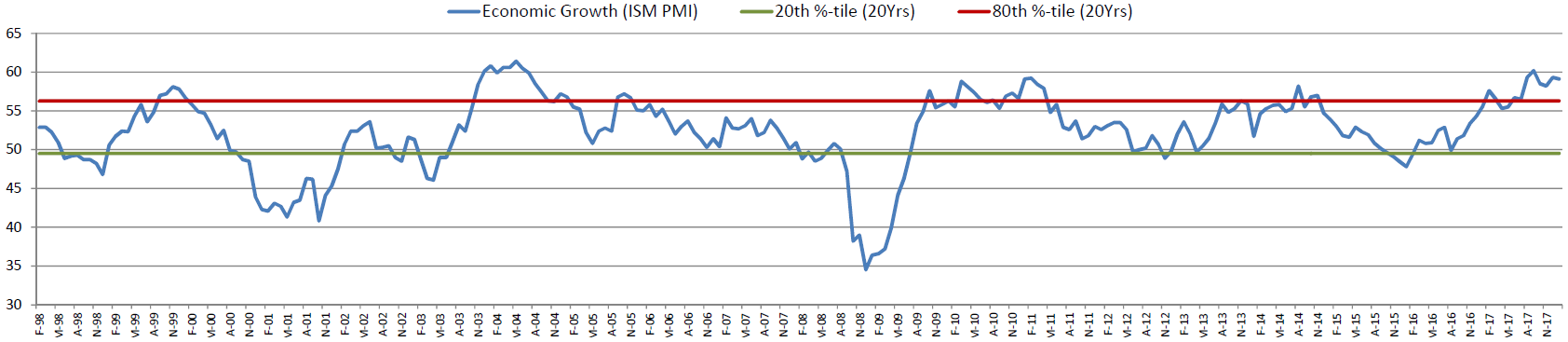

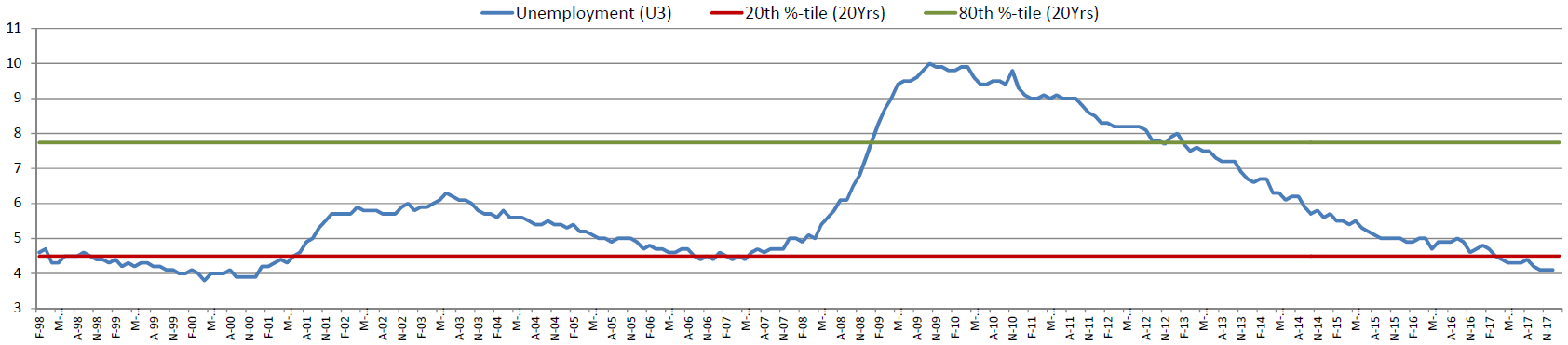

Furthermore, US unemployment is very low. The current level of unemployment is 4.1%, which equates to 95th percentile relative to the last 20 years. Once again, the trend here is positive, with unemployment moving 0.2% lower over the last 6 months. (see chart 3)

Chart 3: US Unemployment Rate

Source: Bloomberg, Accuvest

The extreme levels are the qualifier, but the challenge for investors is in measuring and monitoring the persistence of these trends. As long as valuations and the economy keep expanding, equities can continue inflating.

So what does all this mean for portfolio strategy? What must be done to manage the price risk now inherent and building up in US equity markets? Considering the elevated levels and strong trends, we recommend the following strategies:

- Diversify Globally. The US economic cycle (as judged by age, magnitude, valuations and unemployment) is more mature than those in Europe, Japan, and most Emerging Markets. Increasing portfolio exposure to international economic cycles mitigates the risk inherent in the US market cycle, while maintaining exposure to global economic growth – the primary driver of equity returns. Non-US countries with accelerating economies and attractive relative valuations include: South Korea, Turkey, Italy, Mexico, Spain, Poland, Austria, Brazil, Australia, and Taiwan. (For more information on Country Rankings visit Accuvest.com)

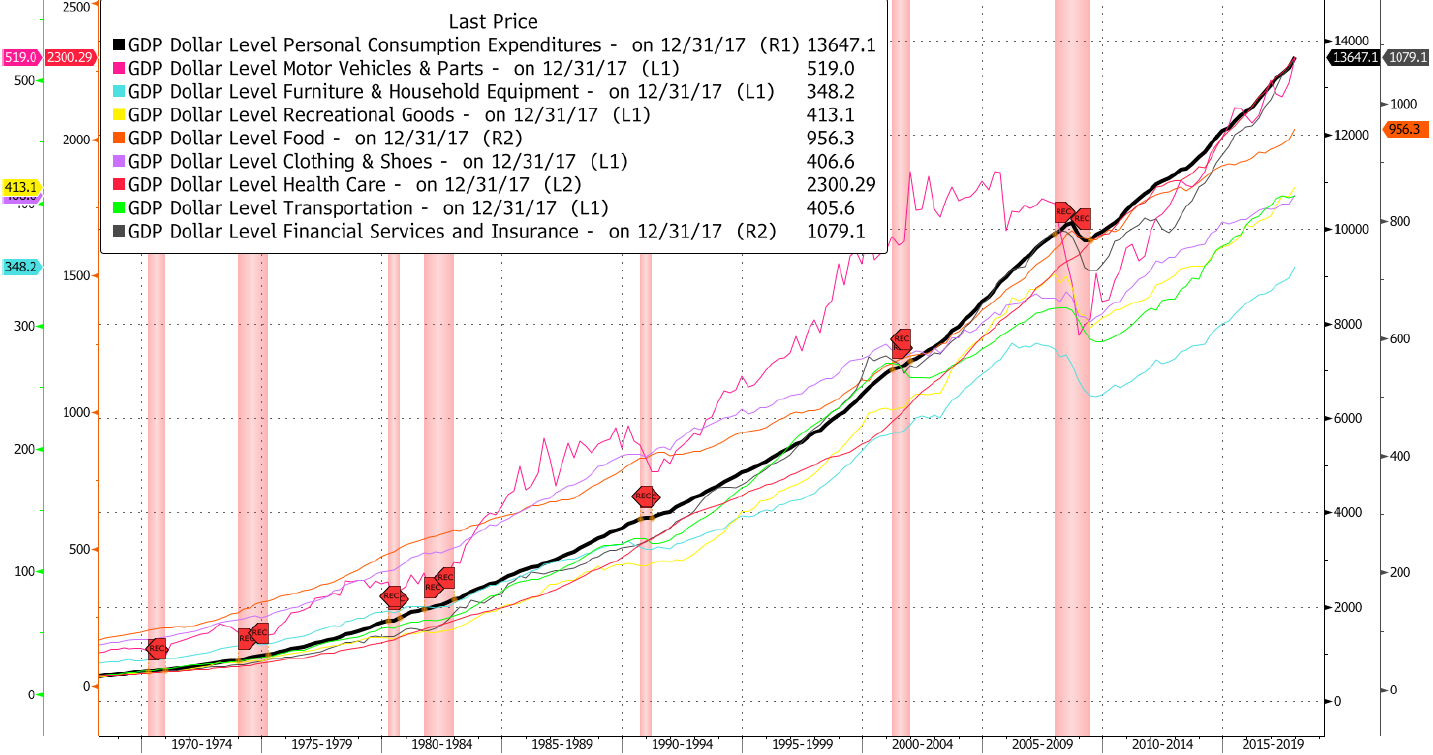

- Trust in the Consumer. Personal consumption (PCE) is resilient to economic and market cycles. While the patterns of personal consumption shift, aggregate consumption rarely retreats (see chart 4). To best exploit the resilience of personal consumption we recommend a core US equity portfolio constructed with multi-factor security selection and attention to shifting brand loyalty and pricing power. Blending undervalued sustainable dividend payers with emerging brands exhibiting sales growth and margin expansion has been especially effective. A final advantage of the “Alpha Brand” approach to late cycle risk is the increased investor conviction that comes with highly recognizable investments. Capital appreciation, over a full market cycle, necessitates a willingness to endure price volatility and an ability to maintain a long-term investment focus. (For more information on Alpha Brands visit Accuvest.com).

Chart 4: Personal Consumption Expenditure & Sub-Components vs. US Recessions (Shaded in Red)

- Follow the Trend. With anything cyclical, there is value in monitoring the trend. If equity valuations and the economy begin to contract, broader re-allocations will be warranted. It is near impossible to say how much longer these measures will trend higher or hold their ground. Act accordingly, and use the trend following to stay properly exposed and manage late cycle risk.

Historically, asset price exuberance and extended economic momentum has come with higher inflation. Higher inflation tends to coincide with higher interest rates and “hawkish” monetary policy. More often than not, bull markets die by high interest rates and cost inflation. Bubbles follow patterns, but maybe this time will be different…stay tuned.

This article was written by James Calhoun, Portfolio Manager – Brands suite of investments at Accuvest, a participant in the ETF Strategist Channel.