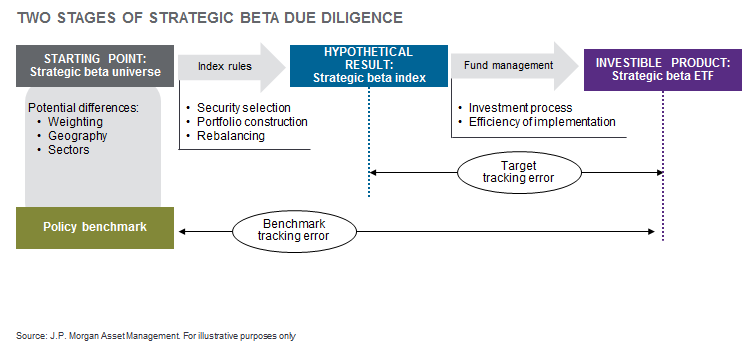

Specifically, we begin at a starting point of a smart beta universe to have a general weighting, geography and sector allocations. The process then implements indexing rules of security selection, portfolio construction and rebalance to achieve a hypothetical resulting smart beta index. The next step involves fund management to include the overall investment process and efficiency of implementing the strategy. We then get the end investible product or smart beta ETF that is able to hit the market. Afterwards, the fund will be monitored for tracking errors to its underlying index over time to bring the ETF back in line with its benchmark.

Larry Whistler, President and Chief Investment Officer of Nottingham Advisors, also explained how investor habits have evolved over time as single factor and multi factor smart beta strategies are growing in popularity. We are witnessing greater demand for multi-factor strategies and ETFs as a way to smooth out the ride and diminish the potential pitfalls of focusing too much on a single smart beta factor. For instance, Whistler mentioned how single factors like minimum volatility may exhibit a higher degree of tracking error, whereas a multi factor combination would reduce the divergence from tracking errors.

The end result is something like the JPMorgan Diversified Return International Equity ETF (NYSEArca: JPIN). The underlying index diversifies risks that are less likely to be rewarded while overweighting areas that are more likely to produce positive results. Staines pointed out that JPIN’s performance from index inception to index launch has exhibited improved risk-adjusted returns relative to traditional market cap-weighted benchmarks like the MSCI EAFE Index.

“Since inception, JPIN has performed as designed, keeping pace with the cap-weighted index on the upside but has captured less of the downside,” Staines said.

Financial advisors who are interested in learning more about smart beta strategies can watch the webcast here on demand.