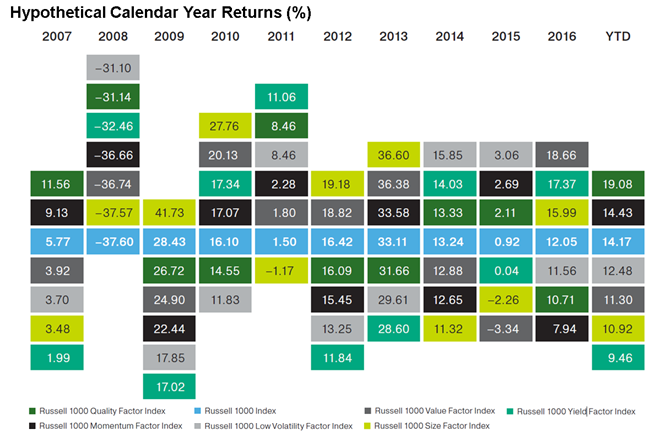

Low volatility refers to stocks that exhibit low volatility tend to outperform higher volatility stocks. The factor is selected by standard deviation of five years of total returns.

Momentum refers to stocks that rise or fall in price tend to continue rising or falling in price. The factor screens for cumulative 11-month return.

Lastly, yield refers to higher yielding stocks tend to outperform low-dividend-paying stocks. The factor is based off 12-month trailing dividend yield.

Investors can gain targeted exposure to these factors through single factor, smart beta ETFs, such as Oppenheimer Russell 1000 Momentum Factor ETF (Cboe: OMOM), Oppenheimer Russell 1000 Quality Factor ETF (Cboe: OQAL), Oppenheimer Russell 1000 Size Factor ETF (Cboe: OSIZ), Oppenheimer Russell 1000 Value Factor ETF (Cboe: OVLU), Oppenheimer Russell 1000 Low Volatility Factor ETF (Cboe: OVOL) and Oppenheimer Russell 1000 Yield Factor ETF (Cboe: OYLD).

“Of these six factors, each has a history of delivering long-term excess returns, both on a cumulative basis and from a risk-reward perspective,” Rolf Agather, Managing Director of North America Research at FTSE Russell, said.

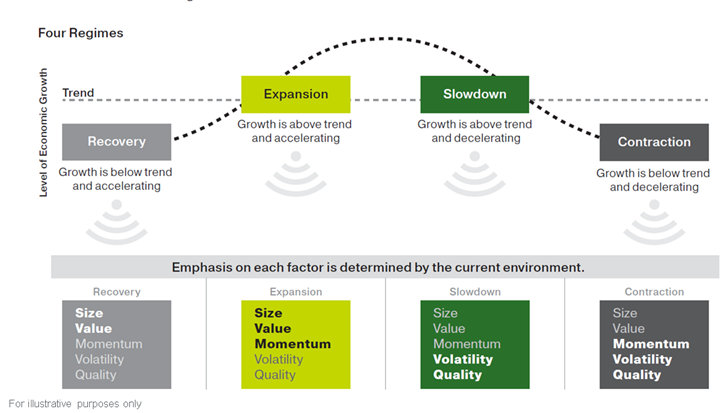

![]() However, over various market cycles and periods, the various smart beta factors may exhibit varying levels of performances as the macroeconomic backdrop plays an important role in determining what does well, Agather said. Investors, though, may combine the factors into a multi-factor strategy to potential diversify the risk and still participate in any upside potential. Since the various factors exhibit low to modest correlations to one another, investors would benefit from combining several factors.

However, over various market cycles and periods, the various smart beta factors may exhibit varying levels of performances as the macroeconomic backdrop plays an important role in determining what does well, Agather said. Investors, though, may combine the factors into a multi-factor strategy to potential diversify the risk and still participate in any upside potential. Since the various factors exhibit low to modest correlations to one another, investors would benefit from combining several factors.

“Investors have come to understand that a multi-factor approach can provide additional diversification benefits because the security selection process seeks to identify stocks that are favorable on multiple characteristics,” Agather said. “A multi-factor approach combines several factors in one portfolio in an effort to improve client outcomes.”

Investors who want a more diversified approach may consider a portfolio that combines the various academically proven factors into a single investment strategy, such as Oppenheimer Russell 1000 Dynamic Multifactor ETF (Cboe: OMFL) and Oppenheimer Russell 2000 Dynamic Multifactor ETF (Cboe: OMFS). The multi-factor OMFL selects companies in the Russell 1000 Index through exposure to a subset of the low volatility, momentum, quality, size and value factors. OMFS provides access to companies in the Russell 2000 Index through exposure to the same factors.

Financial advisors who are interested in learning more about a multi-factor approach can watch the webcast here on demand.