NOVELTY OF FACTOR INVESTING – DOWNSIDE VOLATILITY

By Solactive

Since the financial crisis in 2008, more and more emphasis is put on risk management. But, how do investors quantify the risk of an investment? Generally, it is quantified by standard deviation, which measures the dispersion around the mean return and punishes negative and positive deviations equally. Positive returns, however, do not jeopardize your portfolio and as such shouldn’t be penalized. One alternative is to use downside volatility, which only considers negative returns. The Solactive White Paper series, “The Downside of Low Volatility” and “Minimum Downside Volatility Indices”, have demonstrated that over the long term, a downside volatility strategy can generate convincing performance. But, how have low downside volatility strategies (factor investing) and minimum downside volatility strategies (portfolio optimization) performed very recently?

DOWNSIDE VOLATILITY – A YEAR-TO-DATE REVIEW

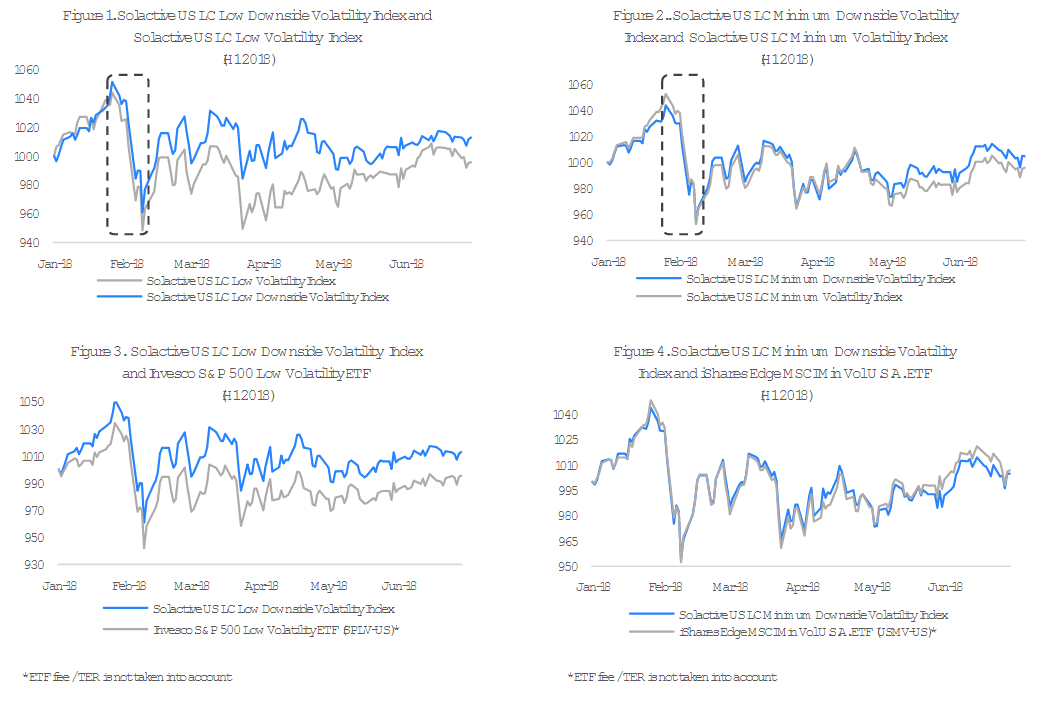

Tense geopolitical climate in Europe, constant threat of a pending “trade war” initiated by the US, denuclearization negotiations in the North Korean Peninsula, the first half of 2018 has witnessed bursts of turbulence and alerted investors against risk. That leads to the question how downside volatility strategies, which intend to reduce risk, performed in H1 2018? Year-to-date performance in Figure 1 to Figure 4 illustrates the defensive nature of downside volatility strategies:

- Compared to plain volatility strategies, the Solactive US Large Cap (LC) Low Downside Volatility Index generated a positive annualized return of 2.52% with a smaller standard deviation (12.82% vs. 13.41%) and a smaller maximum drawdown (-8.61% vs. -9.41%), while a plain low volatility strategy would have lost 0.86

![]()

| Table 1. Performance Measures : US LC Low Downside Volatility, Low Volatility, Minimum Downside Volatility, Minimum Volatility* (H1 2018) |

||||

| Solactive US LC Low Downside Volatility Index | Solactive US LC Low Volatility Index |

Solactive US LC Minimum Downside Volatility Index | Solactive US LC Minimum Volatility Index | |

| Mean | 2.52% | -0.86% | 0.92% | -0.83% |

| Standard Deviation | 12.82% | 13.41% | 12.89% | 12.47% |

| Downside Volatility | 10.30% | 11.61% | 10.53% | 10.22% |

| Sharpe Ratio | 0.20 | -0.06 | 0.07 | -0.07 |

| Sortino Ratio | 0.24 | -0.07 | 0.09 | -0.08 |

| Maximum Drawdown | -8.61% | -9.14% | -8.62% | -9.51% |

| * Measures are per annum. | ||||

- The Solactive US LC Minimum Downside Volatility Index reported a positive annualized return of 0.92%. Its Sharpe ratio (0.07 vs. -0.07) and the maximum drawdown (-8.62% vs. -9.51%) are significantly improved, compared with a plain minimum volatility strategy.

- The largest ETF tracking a low volatility index in the US (Ticker: SPLV-US) produced a negative annualized return of -0.90%*, which was in line with our low volatility index, and was outperformed by the Solactive US LC Low Downside Volatility Index by 3.41% (not taking into account fees / TER).

- The largest ETF tracking a minimum volatility index in the US (Ticker: USMV-US) had a slightly higher return of 1.32*, which is partially due to the inclusion of small-caps. However, the Solactive US LC Minimum Downside Volatility Index had a slightly smaller downside volatility (10.53% vs. 10.65%) and an improved maximum drawdown (-8.62% vs. -9.13%).

Compared with plain volatility strategies, downside volatility strategies generate better returns, with improved risk metrics and Sharpe ratios. They rely on downside volatility’s ability to punish undesirable negative returns only.

More benefits can be seen, if we zoom in the graphs and look at what happened during the large drawdown at the end of January / in early February (Figure 5 and Figure 6): Downside volatility strategies not only lost less in the market turmoil but were also the first ones to recover. In other words, downside volatility strategies showed better resilience and faster recovery compared to plain volatility strategies.

CONCLUSION

To conclude, downside volatility strategies harvest the low risk premium without compromising upside potential. Over a short period of time, it showcases overperformance compared with plain volatility strategies. Particularly, in turbulent markets downside volatility strategies save the portfolio from large drawdowns, while providing momentum for further resurgence.