An article in CFA Institute reports that, although academic research has touted the benefits of “smart-beta,” investing, this research “largely ignores transaction costs that reduce returns significantly.”

The article offers data reflecting the “flood” of academic papers on factor investing, “which provides the theoretical foundation of smart beta allocations,” but adds that creating factor portfolios in academia is “very different from building investable smart beta exchange-traded funds (ETFs).” This is due in large part to the different methods used to construct factor portfolios and smart beta products—so “realized returns from investable products might differ considerably from the theoretical returns.”

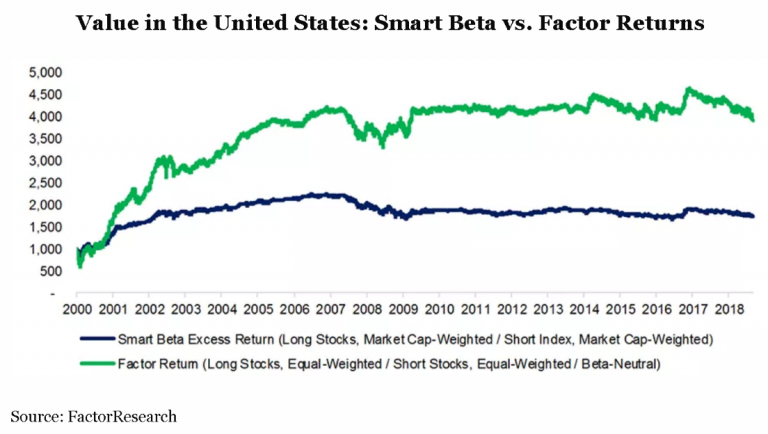

Factor portfolios, the article explains, represent long-short groups of stocks ranked by a certain factor, while smart beta ETFs “are simply index products with factor tilts.” It uses the example of the value factor to provide an example:

The chart shows that the “long-short value factor outperforms smart beta. So, investors looking to capture factor returns based on the research would likely be disappointed by the much lower excess return generated by smart beta.”

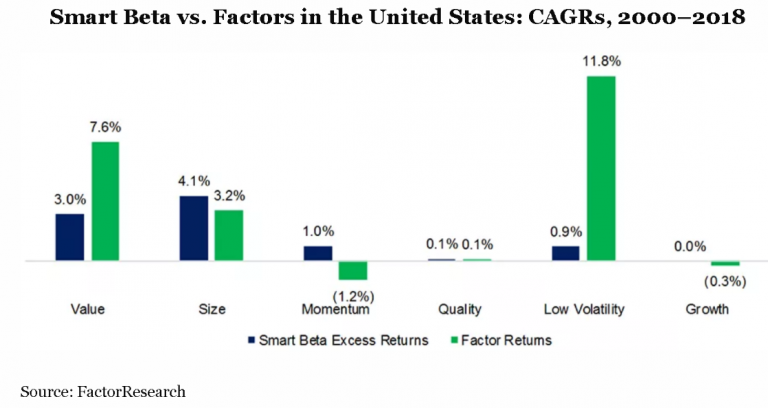

The article reports that when other factors in the U.S. stock market are analyzed, the same trends are reflected:

“Investors should adjust their expectations of low-volatility smart beta ETFs,” the article concludes, adding, “Given low betas, such products might still preserve capital better than other strategies in down markets, but the expected excess returns will be significantly lower than those highlighted in the research papers.”

For more market trends, visit ETF Trends.