Meanwhile, the cost for would-be homeowners to finance the purchase of a home or existing homeowners to refinance their current home continues to get more expensive as mortgage rates have edged up 1 percentage point higher in 2018. According to Daniel Silver, an economist at JPMorgan Chase & Co., rising mortgage rates is “likely to weigh on the existing home sales data in upcoming reports over the next several months.”

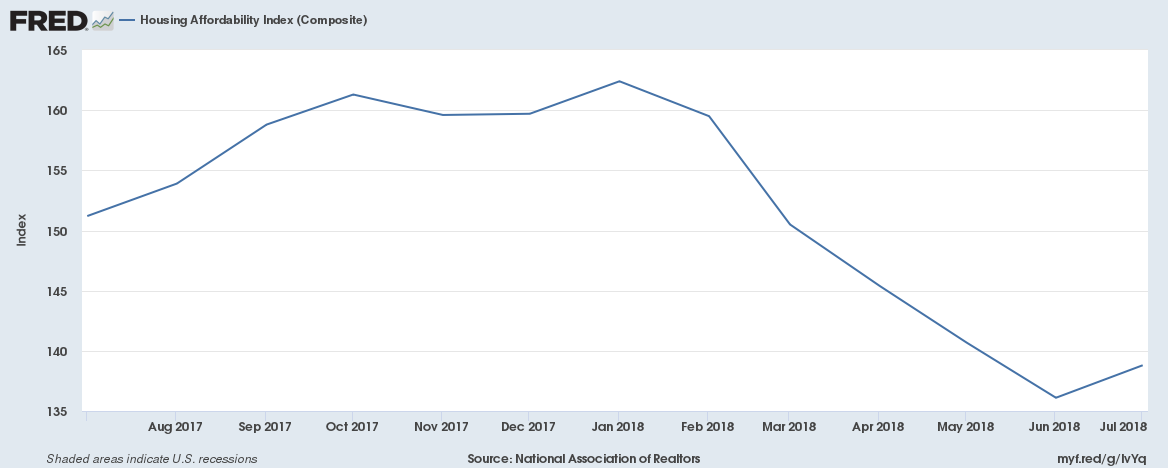

Housing Affordability Heads Lower

Since hitting a peak in January, the housing affordability index has been on a downward trajectory, which could go even lower as the Federal Reserve continues its rate-hiking path, which is expected to run through the end of the year and possibly most of 2019. Just last month, the Fed increased the federal funds rate for a third time this year by 25 basis points, bringing it to 2.25.

The rate hikes have been paired with a marked increase in real estate prices, which have dampened real estate activity. According to the NAHB/Wells Fargo Housing Opportunity Index (HOI), this combination of high prices and interest rates helped to bring down housing affordability thus far this year.

![]()

After the financial crisis and subprime mortgage collapse, home prices took an unceremonious fall as millions of homes faced foreclosure and were sold at heavily-discounted prices. Home prices hit a floor around 2012 and began to recover at accelerated levels, pricing out many prospective homebuyers.

The national median home price jumped from $252,000 in the first quarter of 2018 to $265,000 in the second quarter — the highest quarterly median price in the history of the HOI series.

“The recovery in housing has been really slow to get back on track,” said Mark Vitner, managing director and senior economist at Wells Fargo Securities. “The numbers are all moving in the right direction, but they’re not moving there very quickly and I don’t think that’s going to change all that much.”

For more real estate trends, visit ETFTrends.com