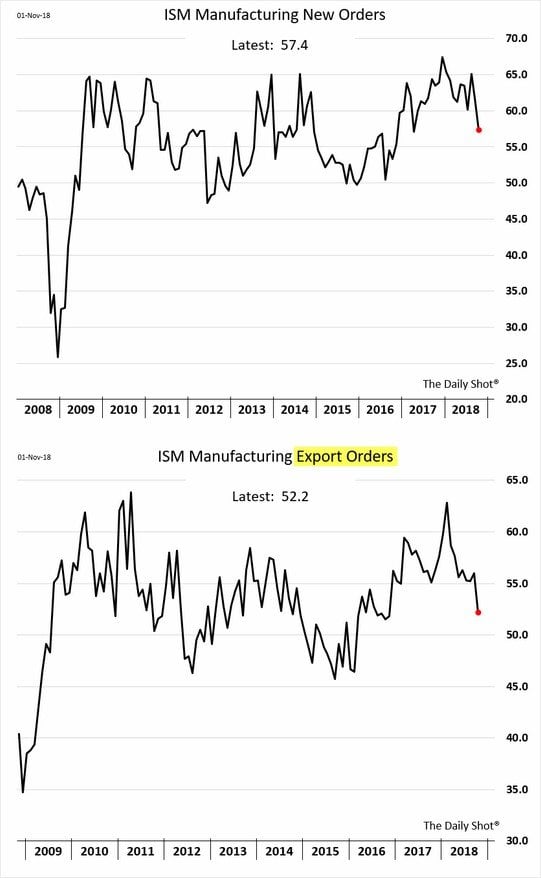

…and November’s ISM survey data…

…indicate that a looming U.S. economic slowdown stretches beyond just “housing.” These higher rates should result in declining corporate profit margins and an increase in defaults, while 2019’s earnings compared to 2018’s won’t be advantaged by year-over-year tax cuts (as 2018’s were vs. 2017’s), thereby making for much tougher comps. I thus continue to believe that—broadly speaking — stocks will continue to slide (albeit with a few upside bounces along the way).

And yet as I’ve often said, I’d far prefer to be buying stocks than shorting them, and thanks to the recent market correction I’m finally starting to see some “microcap value” out there. In that light, let’s start this month with the long positions…

New to the fund for November are shares (still under accumulation, so I’m not yet ready to provide a name) in a microcap tech company in turnaround mode. This company has 40%+ gross margins and although it’s losing some money it has no debt and nearly seven years of cash burn (at the current rate) in the bank, and we’re buying it at an enterprise value of approximately just 0.05x (i.e. 5% of) revenue! As soon as we’re done accumulating the stock (it averages fewer than 50,000 shares a day and trades in the low single digits so it’s taking a few weeks to buy as much as I’d like), I’ll be happy to share the name with you. Hopefully that will be in next month’s letter.

For more investment strategies, visit the Rising Rates Channel.