By Alejandro Saltiel, CFA

Associate Director, Research

Quality stocks have lagged across the globe this year, as expected in the early stages of an economic recovery.

The WisdomTree US Quality Dividend Growth Index (WTDGI) selects companies that look attractive across measures of profitability like ROE and ROA, and earnings growth prospects, and weights them by their dividend stream. The WisdomTree US Quality Dividend Growth Fund (DGRW), seeks to track the price and yield performance of WTDGI, before fees and expenses.

Its fundamental strategy has allowed WTDGI to gain exposure to dividend growers and help avoid exposure to companies at risk of cutting or suspending dividend payments.

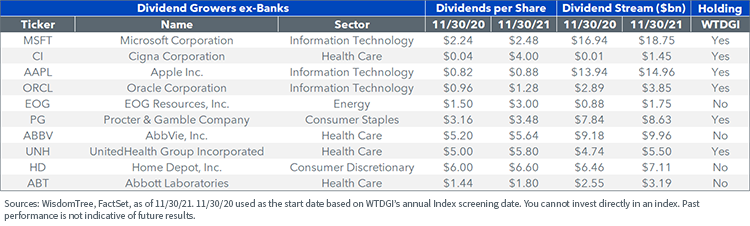

After a year of flat dividend growth, economic growth this year supports dividend growth across all sectors. Out of the 20 largest dividend payers in the S&P 500 Index, 18 have grown their payments over the past 12 months.1 Banks, which were precluded by regulators from increasing payouts in 2020 due to the COVID-19 pandemic, are among the fastest growing. Excluding banks, WTDGI held more than half of the top 20 largest dividend growers found in the S&P 500 Index in 2021.

Methodology Update—The Rise of Intangibles

WTDGI is rebalanced annually to reset exposure to these companies and to adapt to changing economic conditions. Prior to this year’s reconstitution, we announced an update to WTDGI’s methodology, improving on our original process created more than eight years ago. The growing number of negative equity companies that were ineligible for inclusion in WTDGI underscored the need for an update.

Since 2017, the number of companies with negative equity has continued to grow—today more than 30 companies in the S&P 500 fall under this classification. This is partly due to undervalued assets on their balance sheets (brand value, patents, property values, etc.) and maximizing capital efficiency through dividends and share buybacks. Companies with negative equity are commonly involved in the franchising, data, or real estate businesses or are companies with large research and development budgets.

Some of these companies have strong business models and histories of dividend growth, as can be seen in the table below. As the number of negative equity companies continues to increase, we wanted to update the methodology to give them a fair chance to be included in WTDGI.

WTDGI selects eligible companies using a weighted combination of three factors: medium-term estimated earnings growth, historical three-year average ROE, and historical three-year average ROA. This most recent update gives companies with negative equity a median ROE score if they’ve had positive dividend growth over the past five years, making them eligible for inclusion if their growth and ROA numbers warrant it.

Here are some of the major changes after WTDGI’s December reconstitution.

Fundamentals

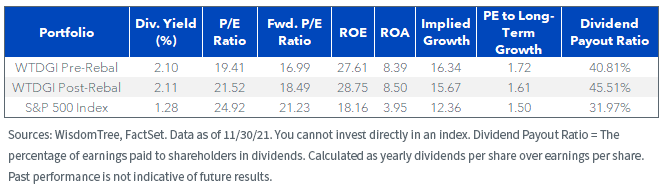

After its annual reconstitution, WTDGI improved both its profitability and valuation metrics. ROA improved to 8.50% and ROE improved by over 100 basis points to 28.75%. Both significantly exceed comparable metrics for the S&P 500 Index.

Along with improved quality metrics, the post-rebalance basket shows higher implied growth as measured by earnings retention times ROE. WTDGI also has a 0.84% higher dividend yield than the S&P 500 with a 13% discount in forward valuation:

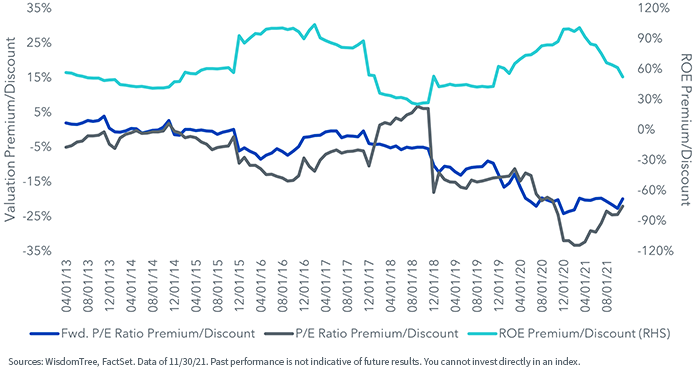

WTDGI is trading at its largest forward valuation discount versus the S&P 500 Index since its inception in April 2013. The chart below shows how both the trailing P/E ratio discount and ROE premium, on the right-hand axis, remain at attractive historical levels.

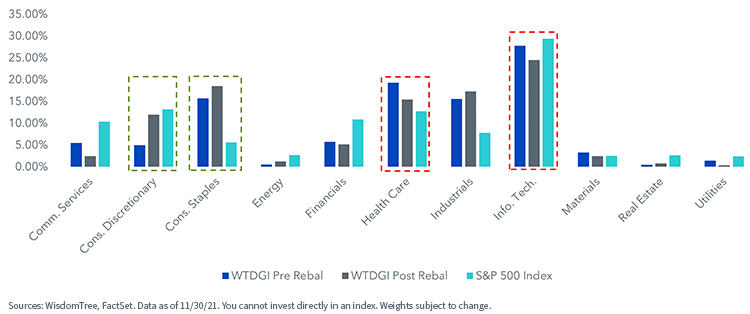

Sector Exposure

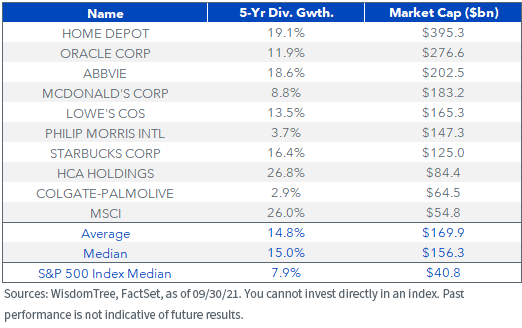

During this latest reconstitution, the Consumer Discretionary sector had the biggest weight increase, as the economy continued to rebound after the COVID-19 slowdown last year. The addition of negative equity but large dividend growers like Home Depot, McDonald’s and Starbucks led the way. The Consumer Staples sector also saw an increase in exposure driven by the addition of Philip Morris and Kimberly-Clark Corporation.

Noteworthy weight reduction came from the Health Care and Information Technology sectors. Companies with large weight reductions were Pfizer, Bristol-Myers Squibb and Intel Corp.

Overall sector tilts versus the S&P 500 Index remain consistent as WTDGI remains underweight in Financials and Consumer Discretionary while being overweight in Industrials, Health Care and Consumer Staples.

Conclusion

Heading into 2022 with an eye on volatility in the latter part of the economic recovery, we believe that having exposure to a basket focused on profitability and growth fundamentals can provide investors with improved risk-adjusted returns.

1 Sources: WisdomTree, FactSet. Data from 11/30/20–11/30/21.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.