With the economy ramping up and earnings growth doing the same, it can be tempting to get aggressive with equity allocations.

However, blindly overweighting riskier assets doesn’t ensure desirable outcomes. Advisors looking to ratchet up equity exposure can turn to tailored allocations, such as the aggressive sleeve of the Strategic Allocation Model Portfolio, which is part of WisdomTree’s Modern Alpha series of model portfolios.

“Our Strategic Model Portfolios are traditional equity, fixed income, and multi-asset models built to address long-term client investment objectives,” according to WisdomTree. “Ranging from conservative to aggressive, these portfolios capture our long-term asset allocation philosophy, while allowing for periodic dynamic tilts as market conditions change. These portfolios seek to offer the potential for competitive risk-adjusted performance versus appropriate passive benchmarks without the higher costs associated with traditional active management.”

Aggressive Indeed

The aggressive corner of Strategic Allocation Model Portfolio is 80% invested in equities.

Moreover, those allocations are diverse, with 20% devoted to ex-U.S. developed markets exchange traded funds and 12% directed toward emerging markets ETFs.

Some of the model portfolio’s domestic exposures are also levered to rising earnings – a credible near-term theme.

“During the month of April, analysts increased earnings estimates for companies in the S&P 500 for the second quarter. The Q2 bottom-up EPS estimate (which is an aggregation of the median EPS estimates for Q2 for all the companies in the index) increased by 4.2% (to $43.73 from $41.98) during this period,” says FactSet’s John Butters.

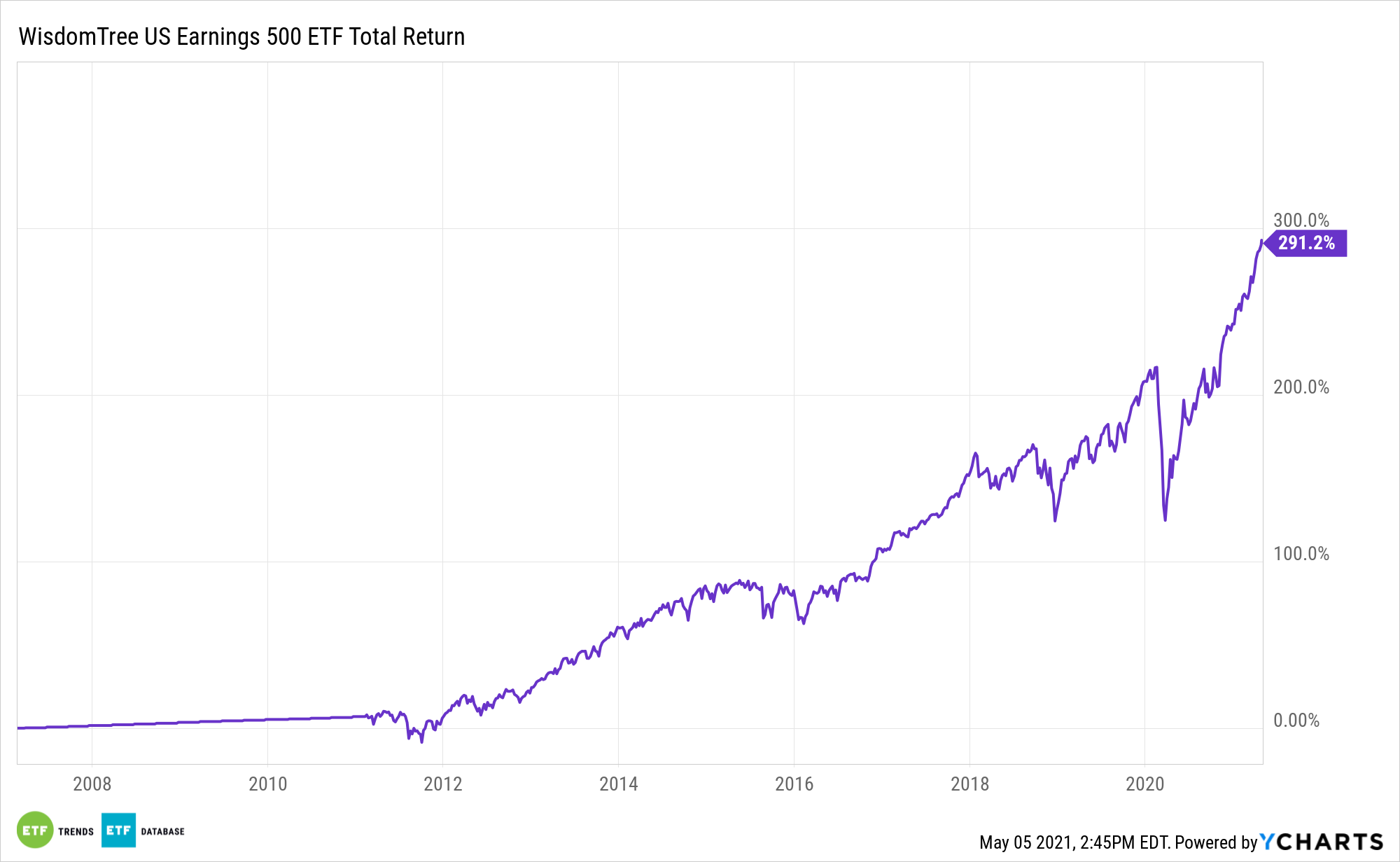

Related to that outlook, it’s worth noting that the WisdomTree Earnings 500 Fund (NYSEArca: EPS) is one of the premier components in this model portfolio.

EPS targets an earnings-weighted index that screens for positive cumulative earnings over the most recent four fiscal quarter period, and assigns weights to components to reflect the proportionate share of the aggregate earning’s each company generated, so those with greater earnings have larger weights.

“In fact, the second quarter marked the second-highest increase in the bottom-up EPS estimate during the first month of a quarter since FactSet began tracking this metric in 2002, trailing only Q1 2018 (+4.9%). It also marked the fourth straight quarter in which the bottom-up EPS estimate increased during the first month of the quarter,” adds Butters.

For more on how to implement model portfolios, visit our Model Portfolio Channel.

The opinions and forecasts expressed herein are solely those of Tom Lydon, and may not actually come to pass. Information on this site should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product.