By Jeremy Schwartz, CFA, Global Head of Research; Kara Marciscano, CFA, Senior Research Analyst

In 2006, WisdomTree launched its first family of fundamentally weighted Indexes, challenging the market capitalization-weight status quo.

Allocating weights based on dividends or earnings challenged the efficient market hypothesis by suggesting that rebalancing to fundamentals could enhance returns. Our fundamentally weighted alternative helps manage valuation risk inherent to cap-weighted strategies that give stocks with higher multiples higher weights and allow those stocks to run without rebalancing on relative value.

We weight our Domestic Core Equity Indexes by earnings because we believe it can lower the price-to-earnings (P/E) ratios—a key metric for guiding risk and returns expectations.

Our team is dedicated to research and new factors to improve strategies, and our Domestic Core Equity family has incorporated an extra layer of risk reduction. The enhancements aim to limit exposure to outlying companies whose earnings may not reflect higher risk and lower quality.

The Core of Our Domestic Core Equity Family Is Unchanged

Our Domestic Core Equity family, which includes the WisdomTree U.S. LargeCap, MidCap and SmallCap Indexes, provide broad earnings-weighted exposure to profitable U.S. companies.

The annual rebalancing mechanism still resets weights based on the concept of relative value, which helps maintain a lower P/E ratio, and to ensure investors do not overpay—a topic of importance given the market’s recent run.

Implementing New Risk Constraints

Our risk constraints marry fundamental and technical analyses—utilizing earnings, quality and price information—to provide a more balanced view than a single metric alone.

- Composite Risk Scores (CRS) – constructed as 50% quality (12-month static and 3-year trends in profitability metrics) and 50% momentum (6- and 12-month returns adjusted for volatility).

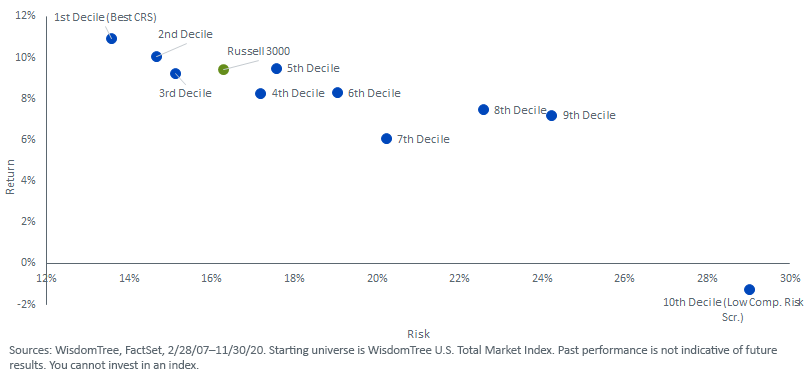

Stocks (profitable or not) are ranked across two distinct U.S. universes, separated by size into a large-/mid-cap group and a small-cap group. The stocks ranking in the bottom 10%, or the worst decile, are excluded from our core equity Indexes, eliminating exposure to companies indicated to be lower quality, lower momentum and higher risk.

WisdomTree U.S. Total Market Index – CRS Deciles – Risk/Return Characteristics (2/28/2007 – 11/30/2020)

- Active Sector Constraints – In addition to our existing 25% sector cap, we are introducing +/- 5% active sector constraints. This means sector weights will be limited within 5% of the sector exposure of a market capitalization-weighted version of our core equity Indexes.

- Individual Security Constraints – We are limiting the degree to which our core equity Indexes can be over-/under-weight in individual securities. Relative to the market capitalization-weighted version of our core equity Indexes, the weight of an eligible company will be equal to or between 0.33x and 3x its market cap weight.

2020 Rebalance Results

In mid-December, our Domestic Core Equity Indexes completed their annual reconstitution.

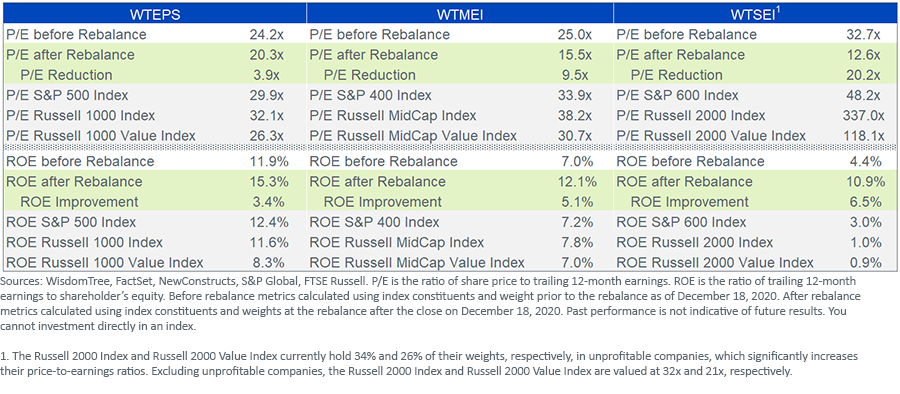

P/E ratios were decreased across the core family for the 14th consecutive year, and all Indexes are currently priced at significant discounts to their benchmarks.

As intended, the combination of earnings weighting and the exclusion of the worst-ranking CRS decile results in our core Indexes exhibiting high-quality characteristics, with aggregate return on equity (ROE) above their benchmarks.

2021 Positioning

2020 was a banner year for expensive, unprofitable stocks. Negative earners and the highest P/E stocks within the Information Technology (e.g., cloud computing stocks Twilio +244% and DocuSign +200%), Consumer Discretionary (e.g., Overstock +580%, Tesla +743%, Etsy +302%) and Communication Services (e.g., Pinterest +253%) sectors were the top-performing subsets of the Russell 3000 Index.[1]

According to Bloomberg, the 502 unprofitable and cash-burning companies within the Russell 3000 Index have returned 40.6% year-to-date, while the average return of the subset of companies with positive profits and cash flow was only 15.6% on average.[2]

These groups benefited from the “stay-at-home trade” at the expense of cyclical stocks linked to the reopening of the U.S. economy.

But that may be changing.

Since September 2020, value outperformed growth by 5.3%, as profitable and lower-valuation Financials, Utilities and Materials stocks rebounded.[3]

Looking ahead into 2021, these valuation-sensitive, earnings-weighted strategies are better positioned for the reopening of the U.S. economy than their market capitalization-weighted peers, and they bring nice valuations to boost.

Originally published by WisdomTree, 1/6/21

1 Sources: WisdomTree, FactSet, for the period 12/31/19–12/31/20. As of December 31, 2020, WTEPS, WTMEI and WTSEI did not hold Twilio, DocuSign, Overstock or Tesla. As of December 31, 2020, WTEPS held a 0.02% of its total weight in Etsy.

2 Sophie Caronello, “It’s Profitable to Be Unprofitable in a Boon for DoorDash: Chart,” Bloomberg, 12/9/20. https://blinks.bloomberg.com/news/stories/QL3DSHT1UM1D. Accessed 12/18/2020.

3 As measured by the performance of the Russell 3000 Value Index and the Russell 3000 Growth Index for the period August 30, 2020 to December 31, 2020.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Tripp Zimmerman, Michael Barrer, Anita Rausch, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Kara Marciscano, Jianing Wu and Brian Manby are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.