As of the end of August, from a market-cap perspective, 61% of global equities were invested in the U.S., with China, Europe, Japan, and other international markets comprising the remainder. Assuming most advisors have a 60% equity/40% fixed income asset allocation split, then the average portfolio should have approximately 25% dedicated to international equities.

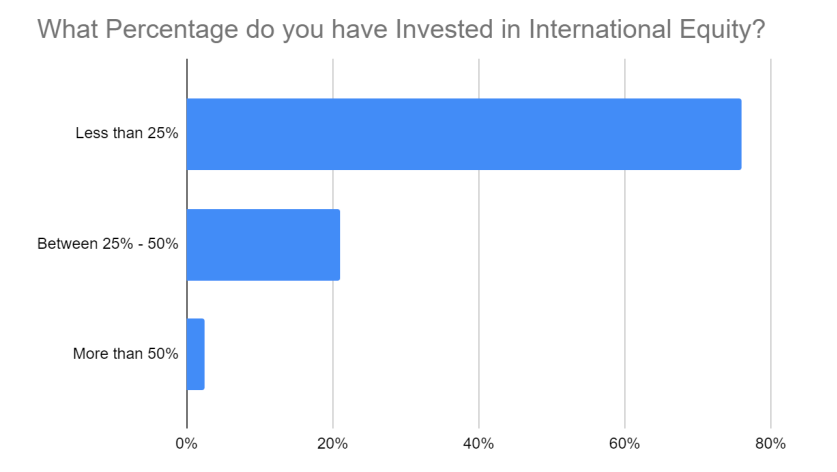

In a webcast last week hosted by VettaFi and asset manager DWS, we asked advisors what percentage they had invested in international equity. While 76% answered less than 25%, a meaningful 21% selected between 25% and 50%, and 2.5% were more aggressively invested internationally with over 50% invested overseas.

International equities have been hit hard in 2022, due in part to the global economic slowdown and the strength of the U.S. dollar. The iShares MSCI EAFE ETF (EFA), which invested in many developed international markets, was down 21% in the first eight months of the year. However, currency-hedged versions of the same strategy held up much better. The iShares Currency Hedged MSCI EAFE ETF (HEFA) and the Xtrackers MSCI EAFE Hedged Equity ETF (DBEF) were down 8.4% and 8.7%, respectively. That’s more than 1,000 basis points that would have been protected by hedging simply through an ETF without much of an added cost. DBEF and HEFA have expense ratios of 0.35%, only three basis points more than EFA’s.

Despite strong recent performance, there’s just $7.5 billion invested in these two ETFs, much less than the $44 billion in EFA, let alone the $84 billion in the iShares Core MSCI EAFE ETF (IEFA), which has slightly larger exposure to developed international small-caps than EFA.

There were 28 currency-hedged equity ETFs that managed $16 billion in assets as of late May, or equal to just 1% of the international equity ETF market.

One reason for the limited assets might be that advisors and end clients do not understand what currency-hedged ETFs are. A currency-hedged ETF invests directly in stocks or bonds, or an ETF that owns them, issued in non-U.S. securities, but minimizes the impact of fluctuation in the local currency relative to the U.S. dollar. The fund hedges the yen, the euro, and other currencies, protecting against their weakness. Therefore, the performance of the ETF is only impacted by how the local securities perform. When the dollar is strong, as it has been in 2022, then the hedged product performs well, but when the dollar is weak, the inverse occurs.

Currency-hedged ETFs used to be very popular in the mid-2010s as firms like WisdomTree, DWS, and iShares made the case for the hedging strategy and ETFs like DBEF, HEFA, and the WisdomTree Europe Hedged Equity Fund (HEDJ) performed well by offering equity exposure with a reduced currency impact. However, in the last six or seven years, these ETFs have bled assets as investors redeemed shares and chose simpler unhedged international equity ETFs.

The average advisor is either unaware of these ETFs or appreciative of how they could be helping reduce the volatility and downside of their international equity allocations in 2022.

For more news, information, and strategy, visit the Global Diversification Channel.