Source: Richard Bernstein Advisors LLC. FRB. For Index descriptors, see “Index Descriptions” at end of document.

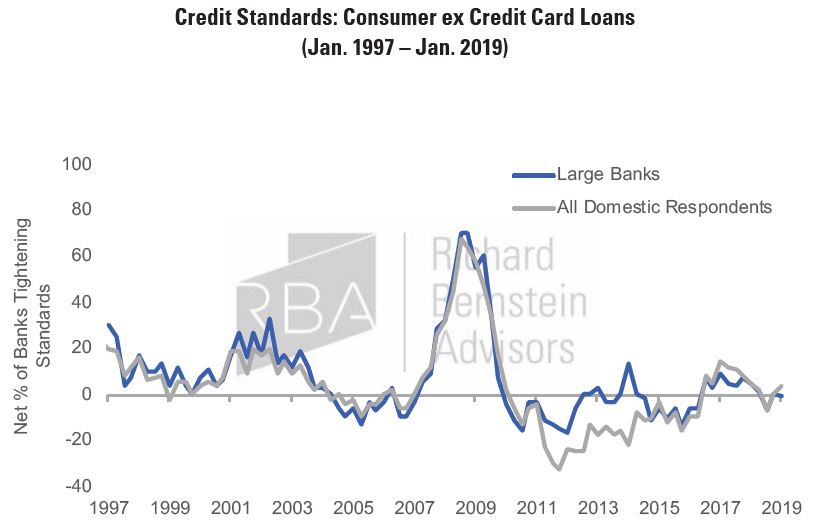

CHART 5:

Credit Standards: Consumer ex Credit Card Loans

(Jan. 1997 – Jan. 2019)

Market implication: watch banks not the Fed The Fed has recently indicated that the equity market’s volatility has influenced the path of monetary policy, and many investors have suggested that a swift and sudden decline in equity prices would cause the Fed to ease. The markets, however, seem skeptical.

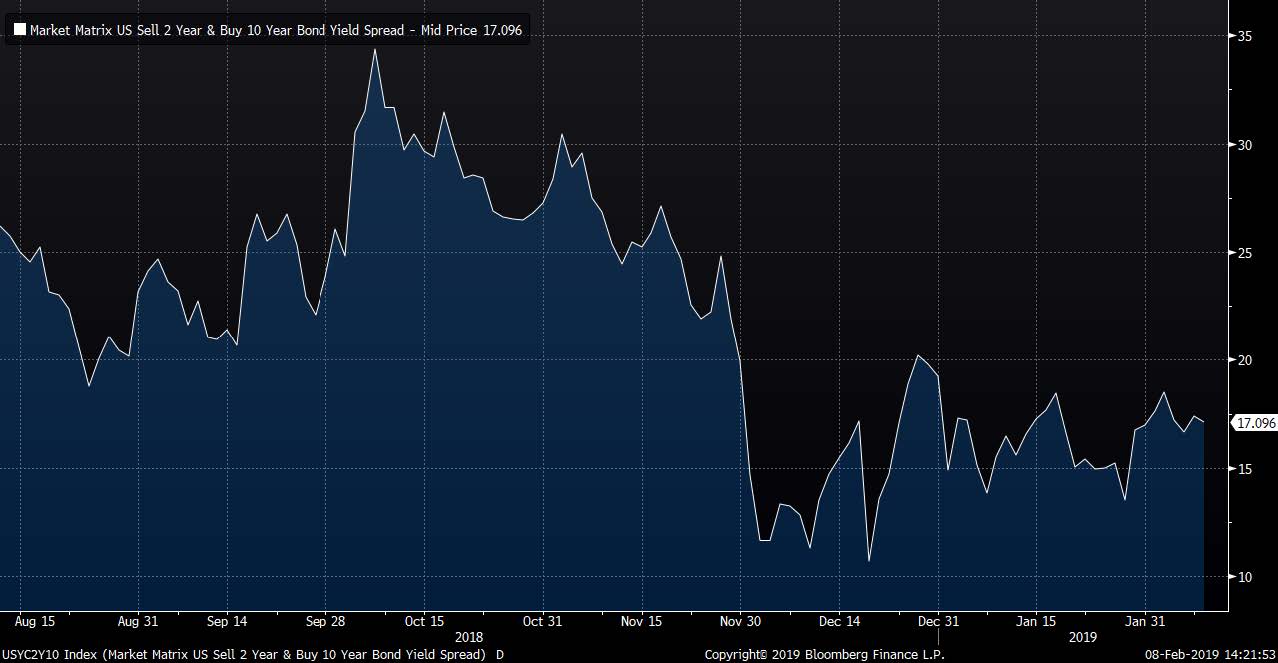

The slope of the yield curve, a reliable leading indicator of the economy, has continued to flatten. The yield spread between the 10-year t-note and the 2-year t-note was about 35 basis points before the fourth quarter’s financial market volatility. It is currently about 17 basis points, or roughly half as steep as it was before the recent period of increased volatility and concern. (See Chart 6.)

CHART 6:

Slope of the Yield Curve: 10-Yr Treasury – 2-Yr Treasury

(Aug. 2018 – Jan. 2019)

Source: Bloomberg Finance L.P.

A flat, but not inverted, yield curve has not historically been a warning signal. However, we find it curious that investors were very worried about the flattening yield curve when the 10-2 spread was twice what it is today, but today seem relatively unconcerned. The curve seems to be paying more attention to actual lending conditions (i.e., the loan officers) than to the Fed’s rhetoric.

RBA’s portfolios Our portfolios remain relatively conservative based largely on our view that profits growth will significantly decelerate during 2019. A further tightening of actual lending conditions would further support that positioning:

Our US equity positions focus on stability and quality of earnings growth because those factors tend to perform well when profits decelerate.

Outside the US, we are overweight Chinese stocks because China is the only major country attempting to stimulate its economy, and because China is one of only two major economies with accelerating leading economic indicators.

Our fixed-income portfolios are positioned with very short duration and very high quality. Lower quality companies’ cash flows are likely to come under increased pressure if profits decelerate and credit conditions continue to tighten.

To learn more about RBA’s disciplined approach to macro investing, please contact your local RBA representative. www.rbadvisors.com/images/pdfs/Portfolio_Specialist_Map.pdf.

This article was written by Richard Bernstein, Chief Executive and Chief Investment Officer of Richard Bernstein Advisors, a participant in the ETF Strategist Channel.