By Gary Stringer, Kim Escue and Chad Keller, Stringer Asset Management

In our view, the odds of a recession have increased from being a possibility to being a probability. The typical recession, like we saw from the third quarter of 1990 to the first quarter of 1991 and the first quarter of 2001 to the fourth quarter of 2001, tends to last just a matter of months and is then followed by robust economic growth driven by pent up demand.

We monitor several broad economic areas to develop our expectations for economic and market conditions. These areas indicate that the U.S. has entered the most challenging economic and market environment of the current business cycle, which goes back more than a decade. Importantly, regardless of the type of shock (e.g. economic damage from a pandemic, housing crisis, oil market shock, etc.), the ramifications tend to be felt across this broad spectrum of leading economic indicators.

The largest equity market declines are historically associated with recessionary environments. During a typical recession, corporate earnings decline 25-30% from what would have been expected prior to the downturn. Likewise, stock prices tend to fall by a similar amount.

There are four broad areas that we track to form our expectations for economic and market conditions. We track these signals in real time to adapt our outlook and positioning as the economic and market environments change.

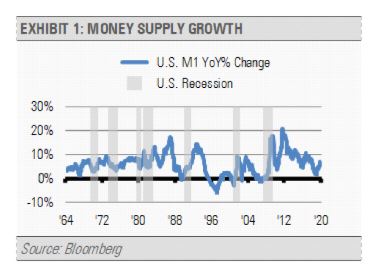

Liquidity, as reflected by monetary conditions, is first on our list. Monetary conditions are heavily influenced by the U.S. Federal Reserve’s (Fed) monetary policy. We can track the Fed’s policy decisions and their effects on monetary conditions.

One excellent way to do this is to watch liquidity growth as measured by M1 growth. This measure of liquidity, which includes hard currency and demand deposits, such as checking accounts, looks healthy so far. As you can see in exhibit 1, M1 growth accelerated last year and is still in a positive trend reflecting the Fed’s shift in policy to be more accommodative. We view that as a positive sign.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Pent up demand often results in a swift acceleration in the pace of economic activity. Though we think that the U.S. economy will grow over the long-term, the pace of the next couple of quarters will depend on the depth of the government and private sector responses to the coronavirus.

With odds of recession increasing, we recently reduced our exposures to economic risk and hold more cash and short-term Treasury bond ETFs depending on the Strategy. This active risk management can help to protect the downside while leaving dry powder to pick up some great values when our work suggests that the time is right.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.