By Rob Stein

With the election behind us and increased visibility of life after the pandemic, I’ve had time to reflect on the economy, the markets and the impact of responses to the economic shut down.

Economists often get stuck in the theoretical or the academic reasons for market movements and economies cycles, often missing “the forest for the trees.”

2020 will be one of those years that will be marked on historical timelines like ‘87, ‘01, and ‘08. 2020 will roll off the tongue when recalling years that are burned in our memories.

Much will be written about 2020, as society saw a good look in the mirror. Change is clearly upon us and it’s been a long time coming, and these changes will certainly impact the economy. I want to be a bit more to the point in this missive, but I plan to cover many of these topics and their impacts on the economy and society more in depth in my 2021 outlook. (Stay tuned)..

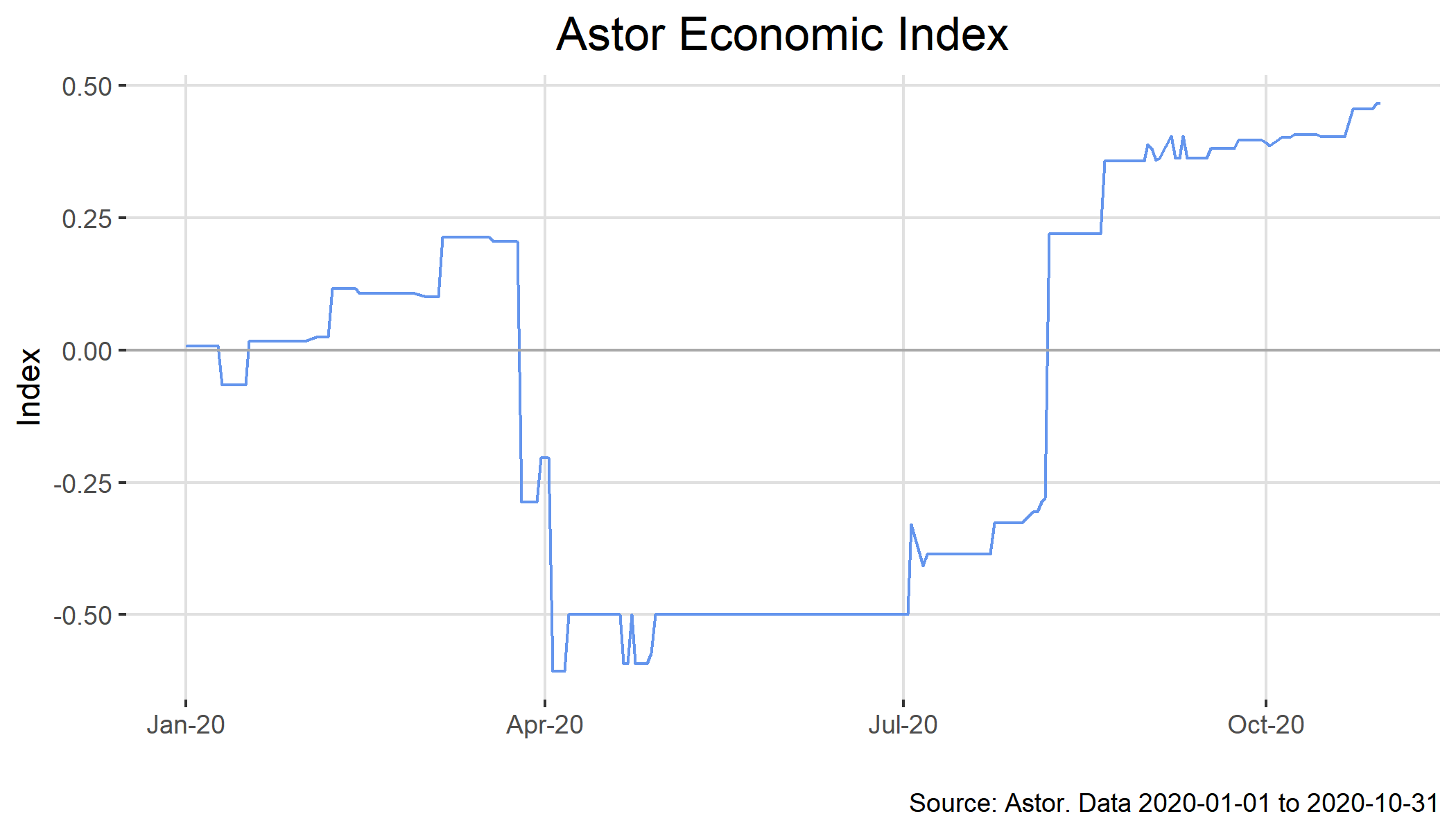

I often describe the economic cycles in terms of expansion, peak, contraction, and trough and use an aggregation of economic data process to identify where we are now. I believe this is a powerful tool to for asset allocation decisions, the most important investment decision I believe you can make.

The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. The Astor Economic Index® is not an investable product and should not be used as the sole determining factor for your investment decisions. There is no guarantee the Index will produce the same results in the future.

That said, I would find it difficult to describe Q2 as a contraction and Q3 as an expansion. To me, it’s more like a bungee cord jumper who was pushed off the bridge, uncertain if the bungee cord will hold, if he would hit the ground, or how far he could recoil back.

But to be sure, the market’s reaction and the Feds response to the bungee cord will mark a pivotal change and a new cycle of monetary conditions. Never has there been a time when so much stimulus, relief programs, and money has been pumped into the system in such a short period of time. And more importantly, directly to people bypassing the traditional increase of money supply and liquidity through the banking system.

This rapid money supply growth will have a profound effect on the economy, markets, interest rates, and inflation in the not too distant future.

While the pundits and experts review, analyze, and calculate the meaning of life and markets, it’s perhaps simpler than we realize. Is there an outcome that seems obvious, even inevitable?

Trillions of dollars were injected into the economy with potentially more to follow. Literally unlimited liquidity to the financial markets which I believe ignited an unprecedented stock market moves.

Our monetary system is based on a Fiat currency; it has no value other than the trust and the value of the goods and services it can purchase. It would seem unreasonable for the nominal value of those goods and services to remain the same after the amount of that Fiat currency that has been increased by so much. In other words, it will take more dollars to buy the same number of widgets. Each unit of currency will be worth-less than before, it’s a form of inflation. We will have too much money chasing too few goods.

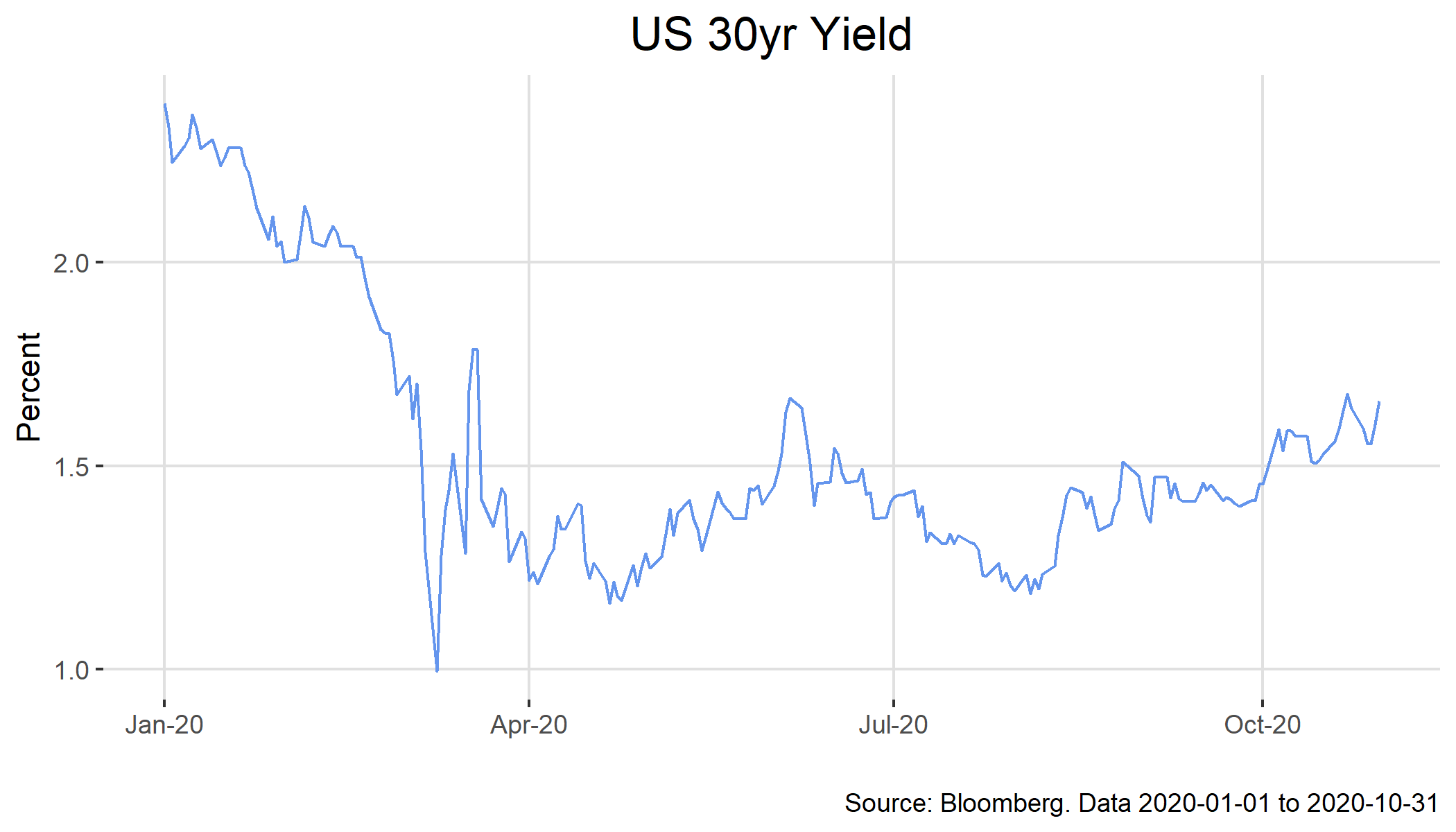

Additionally, there will be a huge amount of borrowing needed by the government and I expect a record amount of bonds to be issued. Clearly this will increase supply, and even with the Fed soaking up much of this supply I believe it will still drive rates higher! Yields are going to have to go up on the long end, in order to be competitive and attract capital. Even with the Fed making it clear that short term rates will be anchored near zero, their ability to control long-term rates is far less effective. Market forces are pretty powerful… Longer-term, I believe, rates are going up and the impact will be meaningful!

Initially it will appear as if we’ve solved the decade-long problem of the below trend inflation (with growth). The Fed has been worried that inflation hasn’t been able to get near the 2% point over the past 10-15 years. Recently they’ve gone so far as to change the mandate to say they’re not using an inflation target anymore, just in time for the target to be met and exceeded.

Equity Markets

The stock market has been responding more to interest rate differentials between stock dividends and risk-free assets then to earnings and revenue growth. Capital always finds its way to the highest yielding asset with the lowest risk, and for now that appears to be stocks.

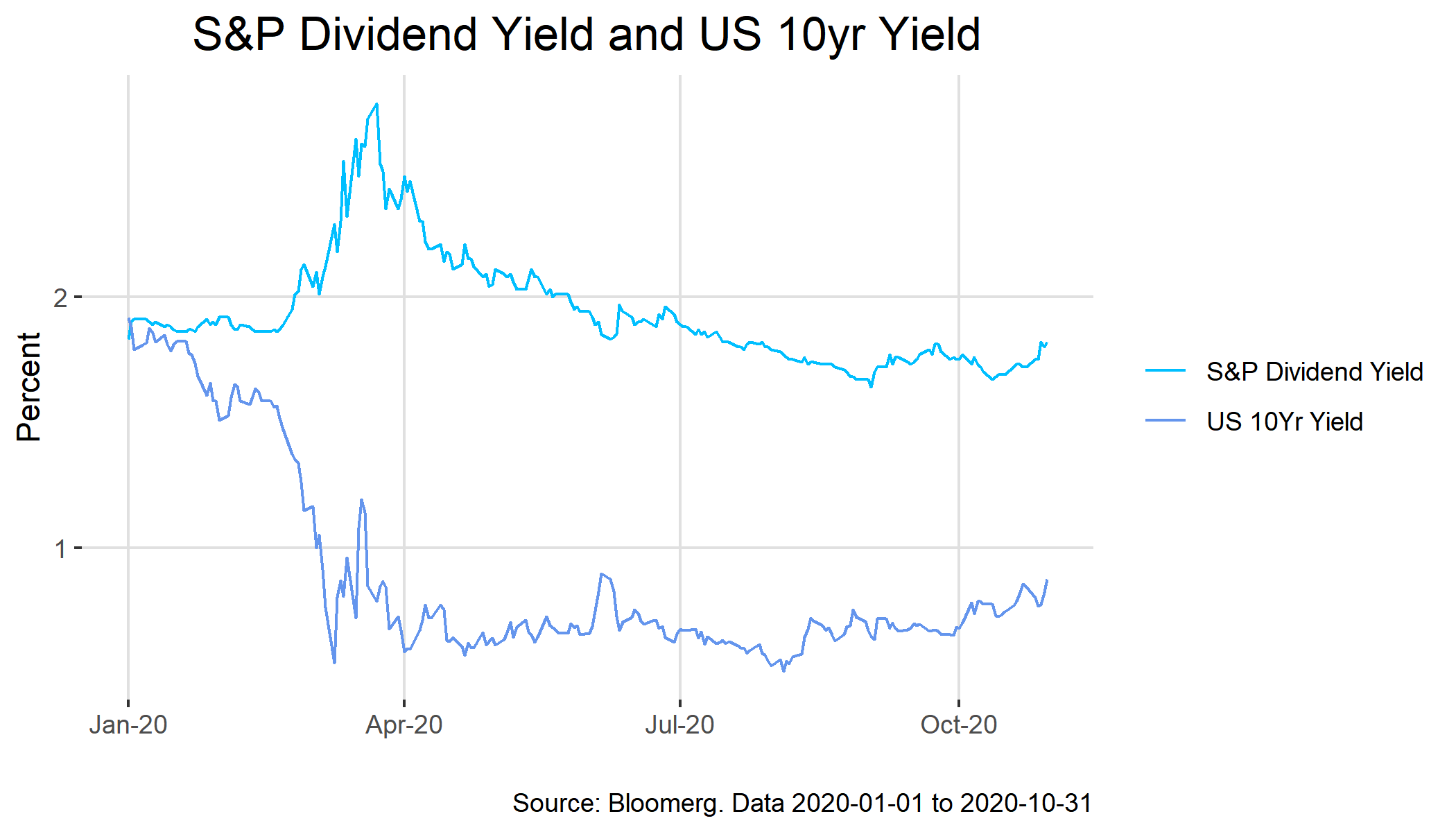

With a market sell-off of 20-30% earlier this year, and the Fed swiftly lowering rates to zero, this created an ~ 150-200 basis point differential between dividend yield on stocks and rates on treasuries. That’s a lot of cushion for the higher return higher risk investment. Investors considering the risk of equities if held for 10+ years seems reasonable. At the market low, what were the odds of the market being 15% lower 10 years from now? I guess it was a pretty good bet and continued to be a good idea even as stocks appreciated and the “cushion” became smaller. However, now with a 50% rally off the lows in major averages (and more for technology sectors) the story is a little different.

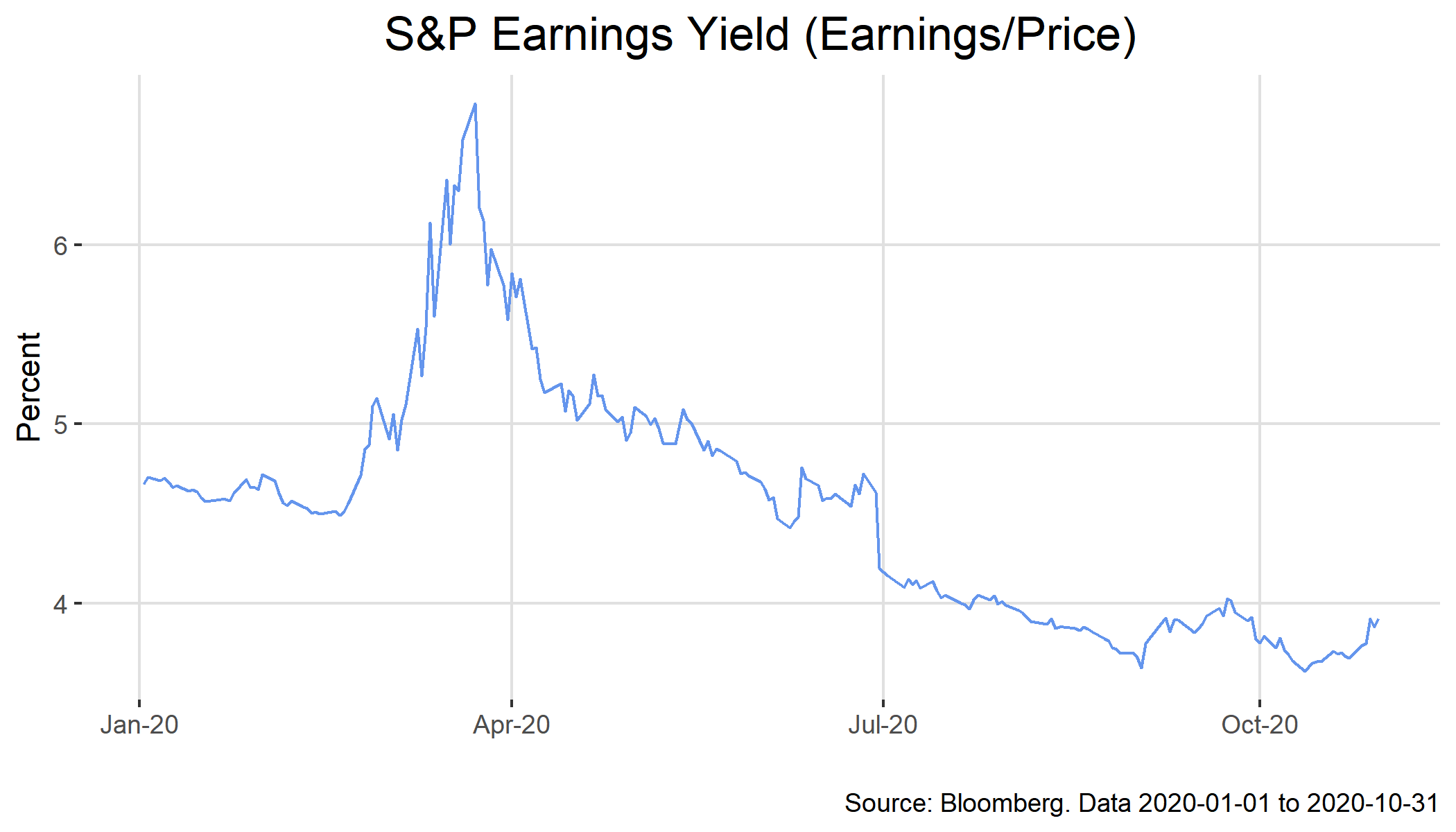

The chart below is the inverse yield PE ratio on stocks, a way to compare the yields.

Note when you compare that to yields on treasuries, it still looks compelling. The stock market is trading like a high-yield bond comparatively with the knowledge that the Fed will be there at some point to support it, basically moving stocks up on the capital structure sort looking like bonds. To make it even simpler, let’s look at the yield on the SP yield vs. 10-year bonds. You get more yield with potentially more upside overall as stocks are positively sloped over time. Now its not normal for stocks to yield more. It might sound like I’m saying there’s a free ride here but I’m just illustrating how we got to this point.

Eventually, I think the pendulum swings back and money flows into the better return asset for the risk. In my opinion, stocks could appreciate to the point where the dividend yield falls making rates on treasuries competitive, or yields on treasuries rise enough to be competitive with yields and performance of stock; even with Fed support below. If this happens, I don’t foresee a market crash, rather a consolidation at what I could call fair value. Equity indices could sit in this range for many years. However, if the economy starts to contract at the same time, look out, a bear market and painful recession could follow.

So, keep an eye on dividends, P/E yields and treasury rates and I will keep an eye on that the economy. We believe the Astor Economic Index® (AEI) is an excellent tool for that!

S&P Dividend Yield: The combined dividends per share of the S&P 500 Index over the last 12 months divided by the closing price of the S&P 500 Index. The S&P 500 Index measures the performance of 500 large cap stocks in the United States.

Originally published by Astor Investment Management, 11/20/20

The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points: including output and employment indicators. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. When investing, there are multiple factors to consider. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. The Astor Economic Index® is a tool created and used by Astor. All conclusions are those of Astor and are subject to change.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Factors impacting client returns include, but are not limited to, choice of custodian, individual investment objectives and risk tolerance, choice of investment program, account structure, timing of account inception, client- imposed restrictions, and fees. The investment return and principal value of an investment will fluctuate and an investor’s equity, when liquidated, may be worth more or less than the original cost. An investment cannot be made directly into an index.

Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

AIM-11/19/20-OP229

All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. Astor and its affiliates are not liable for the accuracy, usefulness or availability of any such information or liable for any trading or investing based on such information. Please refer to Astor’s Form ADV Part 2 for additional information regarding fees, risks and services.