By Michael Contopoulos, Director of Fixed Income

Given year-to-date fixed income returns, one would be forgiven if they never wanted to own the asset class again. Such a view, however, could prove costly as, for the first time in a year, areas of the market are starting to look attractive. We believe that through tactical management and a creative and active approach, positive returns are possible. Below we highlight some examples in the fixed income universe that we are adding to or watching closely just as investors give up and flee the asset class. Remember: returns are greatest where capital is scarce.

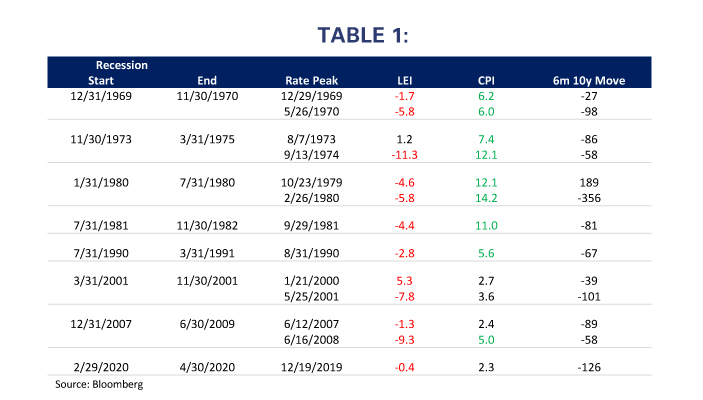

Rates fall when growth declines

In our experience, markets tend to under/overshoot fair value models. Case in point: investors grossly overpriced Treasuries throughout the previous year and a half, resulting in yields that were way too low. Today, however, investors have moved closer to fair value, and by some metrics, are underpricing Treasuries relative to our estimates. Given RBA’s fortunate position of being very underweight duration, and because of the move higher in yields, we increased interest rate risk while remaining underweight. It is becoming increasingly clear that the only path for the Federal Reserve is to tame inflation by bringing down demand. And growth, not inflation, is the biggest driver of longer-dated bond yields. Note the below table that shows the 10-year Treasury yield can reach a cyclical peak even with very elevated levels of inflation.

The Treasury math is getting interesting

Although we doubt the 10-yr yields have reached their apex for this cycle, we are probably closer today than at any time over the last 2 years. If one were to buy a 10-yr Treasury note today, yields would have to increase to 4.3% over the next 2 years before realizing a mark-to-market loss. Although this is possible, if we enter a recession between now and then, and yields fall to 1.5%, the returns stand to be 17-23%. Clearly the upside/downside has shifted, creating an opportunity for us that we have not seen in some time.

Cash-like, not cash

Complicating matters, however, is that the market will likely continue to overshoot between now and such an outcome. Therefore, we prefer managing duration prudently which is why we are now overweight non-index, floating rate instruments and added high quality investments with targeted credit exposure. Two such sectors that we increased recently offer attractive yields while allowing for some appreciation if spreads tighten and/or rates continue to go up. Floating rate investment grade corporate bonds and AAA-rated Collateralized Loan Obligations (CLOs) remain a superior use of capital vs cash as the yield advantage (100-200bp) and total return potential is substantial.

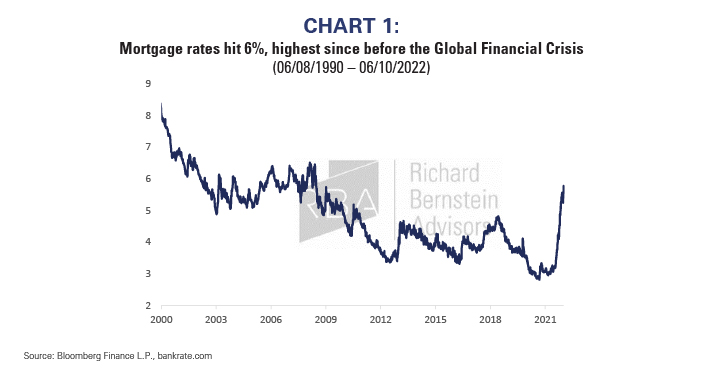

Agency mortgage debt: A good way to add duration

Although not at a level where we would overweight the asset class, agency mortgage-backed securities (MBS) are also quickly becoming an area of fixed income that looks enticing. Considering our medium to longer term horizon and capacity to add duration, we started to dip our toes into the agency space. With mortgage rates now approaching 6%, prepayment risk (being refinanced at a lower rate) has fallen dramatically and given the market’s backing by government-sponsored entities (GSEs), default risk is low. In reaction to the Fed’s quantitative tightening program, spreads have widened, putting yields near the cheapest in a decade. Though MBS is interest rate sensitive, given the recent move in Treasuries and the additional yield, we prefer adding duration through agency debt rather than doing so through Treasuries or corporates.

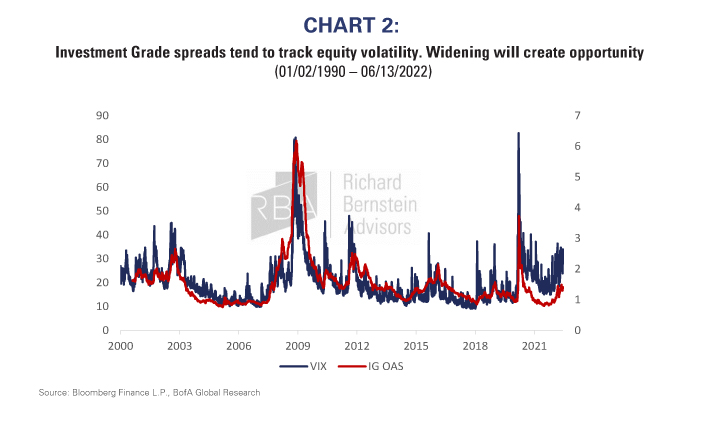

Credit likely to provide opportunity sooner rather than later

We believe we are nearing an inflection point in credit that could create tremendous opportunity over the coming years if tactically managed. Corporate balance sheets are strong, yet spreads seem poised to widen as economic growth slows and volatility persists. Though we are currently in the “pruning” credit risk stage of the cycle as shown by our recent reduction in high yield, we also believe we are not far from a time when wide spreads can create outsized total return potential. Having an active portfolio that can shift from being conservatively positioned for lower yields to being aggressively positioned to capitalize on credit spread tightening, will ultimately be the path to strong fixed income performance over the coming years.

The water is starting to get warm… don’t be afraid to at least dip a toe back in.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be inappropriate for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided “as is” without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.