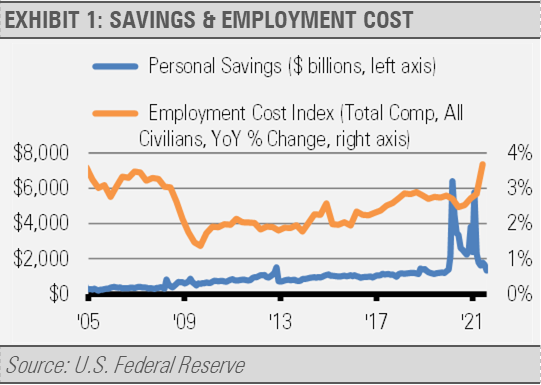

As we visit with investors, we are frequently asked about our outlook for the economy and how it might affect the markets in the near-term. Typically, those conversations focus on jobs growth, inflation, and the impact of the U.S. Federal Reserve (Fed) tapering its bond purchases over the coming months. As we detail below, we think that future monthly jobs reports will build on the strength we saw in the October report released in early November. A combination of factors will likely propel strengthening jobs creation in the months ahead. COVID numbers are much improved over last summer when the pace of jobs creation eased. Furthermore, with job openings remaining near record highs and jobs hard to fill, business surveys suggest that wages will continue to move higher. In fact, a record percentage of small businesses reported increasing compensation according to the National Federation of Independent Businesses. Additionally, the Employment Cost Index (ECI) reached the fastest year-over-year growth rate since 2005. Meanwhile, individuals and families are spending down the windfalls received from fiscal stimulus policy response. As the excess savings decline, we expect that the shortage of available workers will ease, and jobs creation will accelerate.

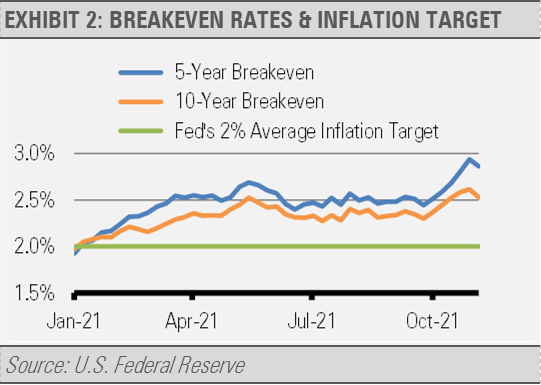

We have been writing extensively about inflation throughout the economic recovery and still believe inflation will remain more persistent than policymakers expect. There are multiple dynamics working together to keep inflation from falling back as quickly as policymakers anticipate including supply chain bottlenecks pushing input costs higher, consumer demand running much higher than the previous cycle trend, and the massive amount of monetary stimulus resulting in roughly $4 trillion in excess cash and cash equivalents in the U.S. financial system. The Fed is targeting an average inflation rate of 2% but markets expect significantly higher inflation. As measured by breakeven spreads, markets are pricing in higher inflation on average than the Fed’s target over the coming five- and ten-year periods.

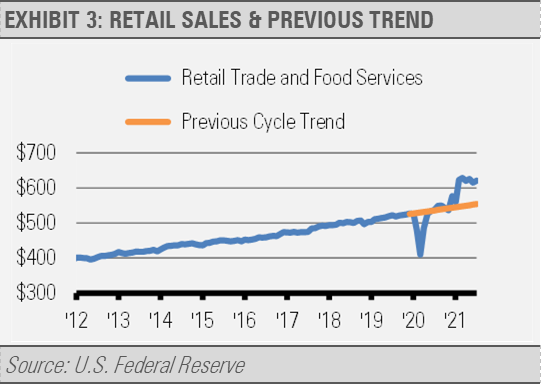

The recent supply chain storages are not only a result of COVID lockdowns crimping supplies due to the strong demand component to the supply chain story. In fact, demand is also running far stronger than during the previous business cycle. As the following chart illustrates, retail sales spiked as the U.S. economy reopened and has remained elevated. At the end of September, retails sales were $67 billion or 12% higher than they would have been without the pandemic based on the previous cycle trend. Further exacerbating supply chain issues are the changes in consumer preferences. With the shift to more home schooling and work from home, spending on goods, such as laptop computers, has increased faster compared to spending on services, such as dining out. For example, spending on services is 2.8% higher than before the pandemic hit while spending on goods is 21.71% higher. In short, U.S. trends in consumer spending on goods are so strong today that demand far outstrips the global supply chain’s capacity.

This massive amount of demand will likely continue into the new year. The growth rate of retail sales is stabilizing and may remain flat for some months going forward. Over the coming 6-12 months, we expect consumers and businesses to adapt to the changing environment. As the economic reopening continues and consumers get back to historical spending patterns favoring services over goods, supply chain issues should ease as businesses navigate their current challenges.

These combined factors have resulted in our outlook of an environment that can support both continued economic growth and persistent inflation. At this time, our expectations are for increased jobs creation, higher corporate revenues, and higher long-term bond yields.

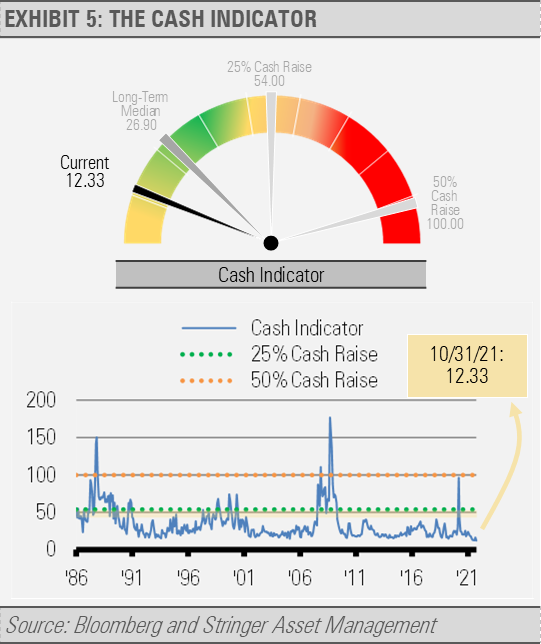

THE CASH INDICATOR

The Cash Indicator (CI) has been an integral volatility forecasting tool for us for more than a decade. In addition to its ability to provide us with an early warning system for high impact market events, it has also been particularly useful in measuring market complacency. Historically, the CI at its current low level has suggested that we should expect higher volatility in the near-term. Our work suggests that we should view any market pullbacks as buying opportunities and necessary to maintain healthy markets.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.