Dan Weiskopf, ETF Professor

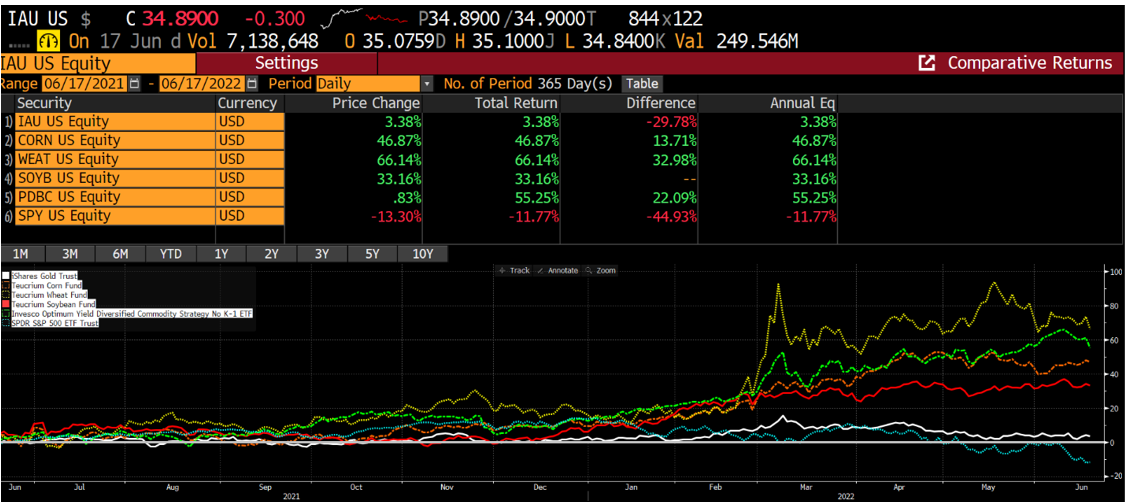

Gold, on a relative basis, has performed well this past year. GLD as an example is up 3.27% versus the decline of 12.77% by the S&P500. Conversely, since it has underperformed relative to soft commodities such as Corn, Soybeans and Wheat, some people seem to question whether gold is in fact an inflation hedge. Arguably, this is a function of what you use as your input in tracking inflation, which at 8.6% may be an extreme number. The strength of the US dollar is perhaps the biggest issue. To this point, Mike McGlone, the Bloomberg Intelligence Commodities Strategist, points out that since gold is not breaking out and near all-time highs like inflation, it is useful as a currency debasement tool and a true diversifier. He highlights that in terms of yen (2.7% away) and pounds (4.7% away), it is close to new highs. Frankly, these days anything close to a new high would seem to be a homerun.

Regardless of this question, it is worth noting that global gold ETFs have taken in some $9 billion in the first five months of 2022. Clearly, some people are making the bet that gold will do its natural thing. Those paying attention to the ETF Think Tank will note that we have hosted Twitter Spaces with Axel Merk and his Team at Merk Investments (ASA) and canvassed the role that gold plays in this investment environment. Similarly, we have also hosted interesting discussions with WisdomTree on Twitter Spaces on the macro conditions and the potential tokenization of gold. Whoever owns gold directly may be squeamish about such an opportunity, but at Consensus2022, it became clear that such innovation has legs despite what some people might say is a cultural dichotomy. Glad to see innovation remains alive and well at WisdomTree.

Hiding in Gold as a Diversifier

Ironically, few asset classes have provided a place to hide under current market conditions, so diversification is arguably a home run. The question, however, is what will happen if the dollar weakens. Will that be the catalyst that leads to a breakout in gold? A weak dollar could also signal further weakness in equities, so this could be pivotal to the portfolio value of the price action of a breakout. How you play it is a different question and one that involves how “structure matters.” Either way, we think Mike McGlone’s work is something that should be followed closely on Twitter, and we also plan to host him on Twitter Spaces at 5pm on Tuesday June 28th.

Summary

Gold is an asset class long believed to be correlated with inflation. It is for this reason some investors have been disappointed by its performance relative to 8.6% inflation. Long-term investors may just need patience or be measuring it against the right currency. Moreover, if the US Dollar ever weakens – buckle up and put your structure matters thinking cap on! The miners may rock!

Disclosure

All investments involve risk, including possible loss of principal.

This material is provided for informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

The value of investments and the income from them can go down as well as up and investors may not get back the amounts originally invested, and can be affected by changes in interest rates, in exchange rates, general market conditions, political, social and economic developments and other variable factors. Investment involves risks including but not limited to, possible delays in payments and loss of income or capital. Neither Toroso nor any of its affiliates guarantees any rate of return or the return of capital invested. This commentary material is available for informational purposes only and nothing herein constitutes an offer to sell or a solicitation of an offer to buy any security and nothing herein should be construed as such. All investment strategies and investments involve risk of loss, including the possible loss of all amounts invested, and nothing herein should be construed as a guarantee of any specific outcome or profit. While we have gathered the information presented herein from sources that we believe to be reliable, we cannot guarantee the accuracy or completeness of the information presented and the information presented should not be relied upon as such. Any opinions expressed herein are our opinions and are current only as of the date of distribution, and are subject to change without notice. We disclaim any obligation to provide revised opinions in the event of changed circumstances.

The information in this material is confidential and proprietary and may not be used other than by the intended user. Neither Toroso or its affiliates or any of their officers or employees of Toroso accepts any liability whatsoever for any loss arising from any use of this material or its contents. This material may not be reproduced, distributed or published without prior written permission from Toroso. Distribution of this material may be restricted in certain jurisdictions. Any persons coming into possession of this material should seek advice for details of and observe such restrictions (if any).