Things We’re Watching In Addition To Stock Prices And COVID-19 Metrics

We have been surprised at the magnitude of the stock market recovery since the March 23rd low. With so many uncertainties related to the COVID-19 pandemic, the current recession, and the upcoming election, it is tempting to worry that the economy will continue to struggle. However, we believe equity prices are the best leading indicator for the economy, and the recent stock market rally suggests that the economy will eventually strengthen despite all the obstacles in its way. Other than stock prices, we think there are several alternative data items that investors should be monitoring right now. This week, we would like to cover a few of them and discuss how we’re positioning our portfolios after the rebound in equities.

Consumer And Business Sentiment: Stronger Than You Might Think

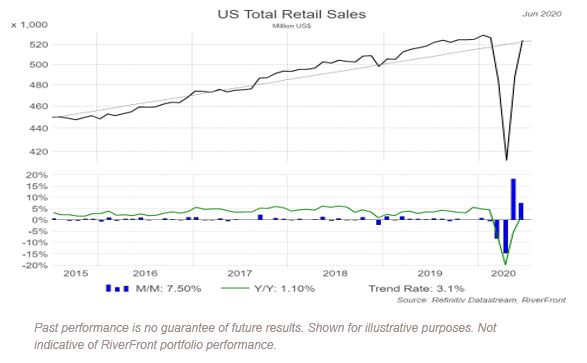

Consumer Sentiment: The consumer accounts for about two thirds of United States GDP and we believe the return of the consumer will be key to a sustainable recovery. One way to measure the strength of the consumer is to analyze their spending habits. It has been remarkable how quickly retail sales, a measure of purchases online and at stores and restaurants has improved. As you can see from the chart, they are back to their recent uptrend and are now close to pre-COVID-19 levels.

Specifically, we have been encouraged that spending has increased for durable goods, which include items such as automobiles and furniture. In our view, these purchases rely on consumers feeling confident about their financial situation since they are typically bigger ticket items. Recently there has been a shift away from non-store retail compared to the data reported at the height of the pandemic. This category fell in the latest report which reinforces that consumers are leaving their homes and spending money instead of ordering everything online due to health concerns. We will continue to watch to see if these trends reverse as COVID-19 concerns have recently picked up again in the US.

Business Sentiment: The National Federation of Independent Business (NFIB) compiles a survey to track the confidence of small business owners and to gauge their outlook on the US economy. For the second month in a row, confidence rose as the country continues to reopen and there is a growing expectation that the recession will be short-lived. We think this is an important metric to watch because small businesses account for half of the private sector jobs in this country. Therefore, we will continue to track consumer and business sentiment over the coming months as signs of whether the recovery is still on track.

Initial And Continuing Jobless Claims: More Progress Needed

One of the key components of the economic recovery will be how long it takes to get employees back to work. Every week investors are provided some insight into that timeline with the reporting of initial and continuing jobless claims. Encouragingly, initial jobless claims have slowed since March, with about 1.3 million people filing for unemployment last week.

Unfortunately, 1.3 million people recently unemployed is still extremely high relative to pre-COVID-19 levels of roughly 200,000 and highlights the fractures in the labor market. Furthermore, continuing jobless claims (people that remain on unemployment) have stayed at elevated levels even as the economy has reopened. Millions are set to lose their unemployment checks on July 31st when the government stops paying an additional $600 per week to jobless self-employed people and contractors who do not qualify for regular state unemployment benefits. We are also concerned that a second round of shutdowns may shift temporary furloughs into permanent job losses.

We are hopeful but not yet convinced that the job market is stabilizing. Until initial and continuing jobless claims decline below the 2009 peak of 665,000 we will remain concerned about the labor market.

Housing Market Trends: Surprisingly Resilient

The housing market has many trickle-down effects for the economy and is also a major component of an individual’s net worth. For these reasons, it is encouraging that home prices have remained resilient. We believe there are two main drivers for the strength in housing. First, mortgage rates are at record lows with the average 30-year mortgage rate falling below 3%. With monthly interest payments meaningfully lower, the ability to finance a higher-priced home becomes much more manageable. The second factor supporting home prices is the lack of inventory, or homes available for sale. According to Realtor.com, the number of homes on the market fell 27.4% in June from a year earlier.

In general, we think home prices reflect opinions about the future of the economy. In other words, the purchase of a home might be the ultimate “durable good” signaling stronger consumer confidence. We would argue that home purchase applications near an 11-year high demonstrates the confidence that homebuyers have in the economy despite the uncertain backdrop.

In addition to home buyers, home builders have also been feeling good about the recovery. For example, the National Association of Home Builders/Wells Fargo Housing Market Index, a monthly indicator based on a survey of home builders about their perceptions of current and future home sales, has been increasing since April. In fact, the most recent survey from July shows that confidence is back to pre-pandemic levels last seen in March! The combination of record low interest rates, lack of supply, and growing confidence should provide support to the housing market, which we think is critical for the sustainability of this recovery.

Mobility Trends: People Back In Motion

Our investment team has been monitoring “mobility” to forecast when or if consumers return to their normal routines. For example, Apple publishes daily mobility information that shows requests for directions in Apple Maps. This data is available for the entire country but is also available to view by region. This information is publicly available here: https://www.apple.com/covid19/mobility

These mobility charts highlight COVID-19’s negative impact on mobility, especially in March and April as the virus began to spread throughout the country. However, beginning in late-April, driving and walking trends improved and are now close to pre-pandemic levels. As you may have noticed in your hometown, road and highway traffic seems to be getting back to normal and the public parks and sidewalks are filled with folks trying to escape the confines of their homes…hopefully in a socially-distanced fashion.

While road and sidewalk traffic have increased, the destinations for travel have likely changed. For example, instead of driving into the city to work in an office, people might be driving to the local home improvement store to renovate their home office. Importantly, the people of this country seem to be leaving their homes again, which should provide a boost to economic activity.

What It Means For Our Portfolios: Positioned For Recovery

We think the economy will continue to rebound but in different ways than in past cycles. For example, although the mall in your town might have an empty parking lot, it might not mean that retail sales are struggling. Instead, we think this crisis will accelerate the trend towards online purchasing activity. Home prices may continue to rise, but the growth might not occur in the same neighborhoods that have experienced the most price appreciation for the last 10 years. Therefore, we need to consider both micro and macro trends as we come out of this health crisis.

Lastly, the items above are obviously not an exhaustive list of things our team is monitoring. As mentioned earlier, we think stock prices are the best leading indicator for the economy and that they reflect the collective wisdom of investors around the world. Luckily, our mantra of “process over-prediction” kept us focused on the positive message from the market in addition to some of the data referenced above. As such, we are slightly overweight equities with a preference for US equities relative to international stocks and bonds. Our team continues to monitor the items outlined in this piece and stands ready if our risk management process warrants action.

Important Disclosure Information

The comments above refer generally to financial markets and not necessarily to RiverFront portfolios or any related performance. Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Information or data shown or used in this material is for illustrative purposes only and was received from sources believed to be reliable, but accuracy is not guaranteed.

In a rising interest rate environment, the value of fixed-income securities generally declines.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

You cannot invest directly in an index

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

The NAHB/Wells Fargo Housing Market Index (HMI) is based on a monthly survey of NAHB members designed to take the pulse of the single-family housing market. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next six months as well as the traffic of prospective buyers of new homes.

The National Federation of Independent Business (NFIB) Small Business Optimism Index is a composite of ten seasonally adjusted components. It provides a indication of the health of small businesses in the U.S., which account of roughly 50% of the nation’s private workforce.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2020 RiverFront Investment Group. All Rights Reserved. ID 1250858