We expect interest rates to move higher with continued modest inflation increases and potential normalization of real (inflation-adjusted) interest rates. For example, while real interest rates have remained low throughout this expansion, they have moved up recently, driving the rise in nominal long-term rates in September and early Q4. Meanwhile, the Federal Reserve continues to tighten monetary policy, which is pushing up short-term interest rates.

International trade policy also presents risk. We anticipate, however, that a sustained escalation in the trade dispute with China is unlikely, as deals reached with the European Union and with NAFTA trade partners suggest the Trump Administration is willing to compromise rather than suffer too great a negative economic impact. Short of a prolonged escalation of the trade dispute with China, material impacts on the U.S. economy should be limited to specific segments, such as manufacturing and agriculture, given the positive U.S. fundamentals.

Another source of uncertainty is the upcoming midterm elections. While we are not making a prediction on whether Republicans lose control of one or both houses of Congress, the specific degree of the outcome is less important than directional shift in power. Democrats are likely to gain seats in the House. A pickup of seats in the Senate is less likely, however, given the number of Democratic incumbents running for reelection in states President Trump won in 2016. With a Republican President and less-than-overwhelming Republican majorities in Congress, any Democratic gains would reduce the government’s already-limited ability to pass major legislation. Thus, absent surprise strength by Republicans, the net result of the elections should increase gridlock and have limited impact on our broad outlook.

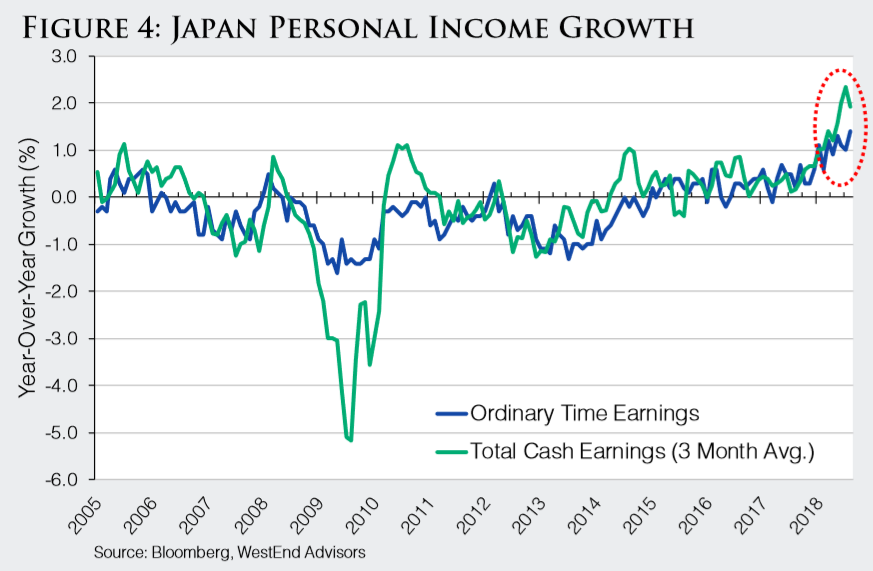

International Outlook: Outside the U.S., European economies remain constrained by structural challenges, such as Italy’s debt load, and have recently shown signs of cyclical headwinds. Euro Area GDP growth has slowed notably so far this year compared to 2017. In contrast, in Asia, the long-suffering Japanese economy is showing some signs of improvement, including improved personal income growth (Figure 4) and a pickup in business capital expenditures on the back of increased corporate profitability.

Economic growth in some key emerging economies, like China, has been slowing for some time. Still, economic growth rates are notably higher in emerging markets, on average, than in developed markets. Asian economies, in particular, should continue to benefit from positive secular drivers. There has been a fundamental shift over the last decade in the composition of economic activity in these markets, and Information Technology is now the largest equity sector within Asian emerging markets. This gives emerging Asia a fundamentally different profile than emerging markets in other regions, such as Latin America, where commodity-related industries are key drivers. Thus, Asian emerging markets should receive a tailwind from many of the same long-term trends that are benefitting the Information Technology sector in the U.S.

While the global economic picture has not shifted dramatically this year, a deterioration in investor sentiment toward international equities, and especially emerging markets, has led to a significant valuation discount of certain international equities compared to U.S. stocks. Asian equity markets, in particular, are at essentially all-time low P/E valuations compared to U.S. stocks.

In our view, some of the concerns that have weighed on emerging markets are overdone. Trade tensions, for example, are likely to ease. If they do, Asian stocks should benefit, and the U.S. dollar is likely to weaken, which would provide an additional tailwind for emerging markets. If, on the other hand, trade tensions continue or intensify, they should pose less of an economic headwind than is widely anticipated. China, for example, is the primary target of U.S. tariffs, but only about 19% of Chinese exports go to the U.S. The Chinese government is also likely to take measures that can mitigate some of the negative economic impact of tariffs, while other emerging markets in Asia are likely to benefit if trade shifts away from China. We recognize there are material risks associated with shifting U.S. trade policy, but we currently believe equity markets have substantially discounted those risks, which makes the risk/reward profile of emerging Asian stocks much more attractive today than at the beginning of the year.

Conclusion

We expect moderate economic growth will continue in the U.S. and abroad into 2019. Our portfolios are positioned in U.S. sectors that benefit from certain cyclical trends, such as U.S. consumer strength, as well as secular trends, like the shift to digital media. We continue to manage portfolio risk, in part, through avoidance of the most economically-sensitive U.S. sectors and, in balanced portfolios, by limiting exposure to longer-duration fixed-income securities. We have also made minor allocation adjustments in our global strategies to take advantage of expected improvement in sentiment toward Asia, where we now view valuations as misaligned with fundamentals.

We remain vigilant in our analysis of global macroeconomic and market conditions. As we write this, an uptick in market volatility is highlighting a range of investor uncertainties, but does not change our fundamental outlook. Please feel free to contact us with any questions on our outlook or portfolios, and thank you for your continued interest in WestEnd Advisors.

Disclosures:

This report should not be relied upon as investment advice or recommendations, and is not intended to predict the performance of any investment. These opinions may change at any time without prior notice. All investments carry a certain degree of risk including the possible loss of principal, and an investment should be made with an understanding of the risks involved with owning a particular security or asset class. Portfolio characteristics and/or allocations are generally averages and are for illustrative purposes only and do not reflect the investments of an actual portfolio unless otherwise noted. Portfolios that are concentrated in a specific sector or industry may be subject to a higher degree of market risk than a portfolio whose investments are more diversified. While every effort has been made to verify the information contained herein, we make no representation as to its accuracy. We invite you to view additional information about our strategies, including a full set of disclosures, on our website at www.westendadvisors.com. Additional information may also be obtained by phone at 888-500-9025, or by email at [email protected].

The MSCI ACWI consists of 47 country indexes comprising 23 developed and 24 emerging market country indexes. The total return of the MSCI ACWI (Net) Index is calculated using net dividends. Net total return reflects the reinvestment of dividends after the deduction of withholding taxes, using (for international indices) a tax rate applicable to non-resident institutional investors who do not benefit from double taxation treaties. The MSCI Emerging Markets Index represents a subset of the MSCI ACWI, comprising 24 emerging market country indexes. The Standard and Poor’s 500 Stock Index includes approximately 500 stocks and is a common measure of the performance of the overall U.S. stock market. An index is unmanaged and is not available for direct investment.

Holdings, Sector Weightings, and Portfolio Characteristics were current as of the date specified in this presentation. The listing of particular securities should not be considered a recommendation to purchase or sell these securities. While these securities were among WestEnd Advisors’ holdings at the time this material was assembled, holdings will change over time. There can be no assurance that the securities remain in the portfolio or that other securities have not been purchased. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities presently in the portfolio. Individual clients’ portfolios may vary. Upon request, WestEnd Advisors will provide a list of all recommendations for the prior year.