The impact:

A blowup in the leveraged loan space would likely be symptomatic of a broader recession rather than the root cause. Nonetheless, the possible illiquidity of CLOs in a crisis would slow the redeployment of capital and perhaps exacerbate the deleveraging process.

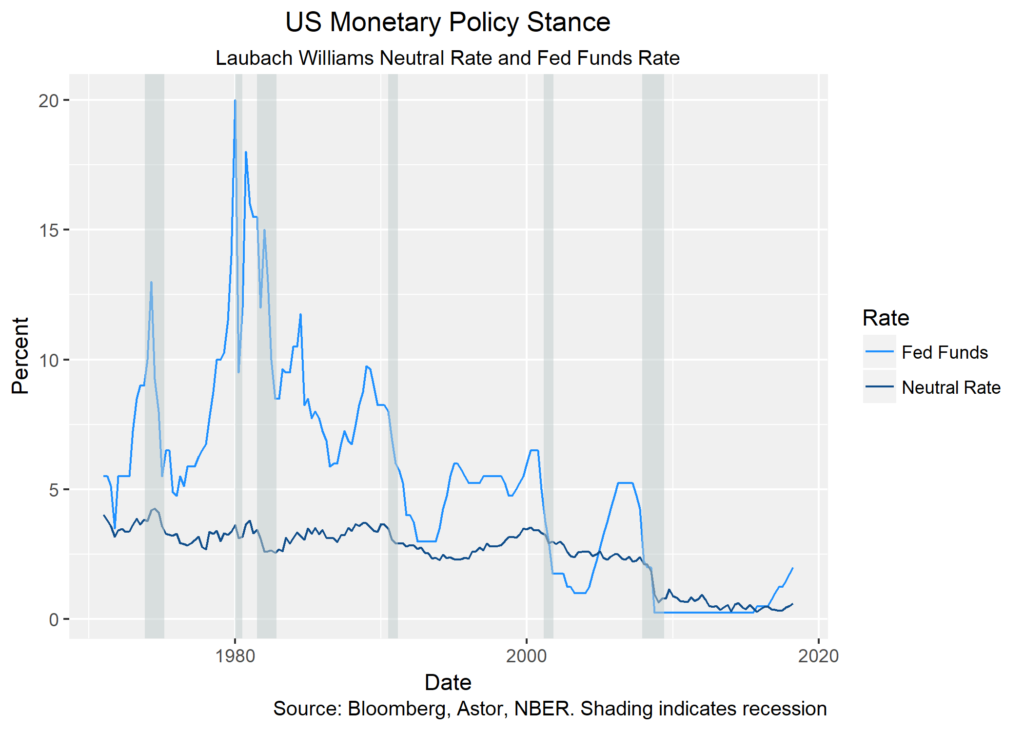

The Fed Clamps Down

Why it might happen:

Flashy predictions of tail risk events grab all the headlines, but the truth is often more mundane. A fairly standard credit cycle turn could be driven by the Fed hiking too much, too fast, despite promises from the FOMC to the contrary.

Why it might not:

The contrarian view, expressed less frequently these days, is that the Fed is behind the inflation curve and indeed should be tightening faster. If you subscribe to this narrative, you’re more likely to believe that a credit bubble fueled by low rates will be responsible for a recession, rather than overeager rate hikes.

The impact:

A Fed driven recession would probably be the most benign of the scenarios presented here. Following a domestic deleveraging and slowdown, economic growth would resume after 12-24 months if policy responses are appropriate and economic contraction does not reveal any greater structural weaknesses.

Conclusion

Unfortunately, we will only understand the next recession in hindsight. The only truly predictable event is that backward-looking analysts will deem the impetus as avoidable and obvious. At Astor, we will continue to watch global macroeconomic developments closely, and leverage our proprietary Astor Economic Index® to nowcast the state of the US economy.

All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. Astor and its affiliates are not liable for the accuracy, usefulness or availability of any such information or liable for any trading or investing based on such information.

2018-255