As a capital preservation metric, the pain index measures risk in losses. Specifically, it measures the depth, duration, and frequency of losses.

Measuring Risk in Dollars

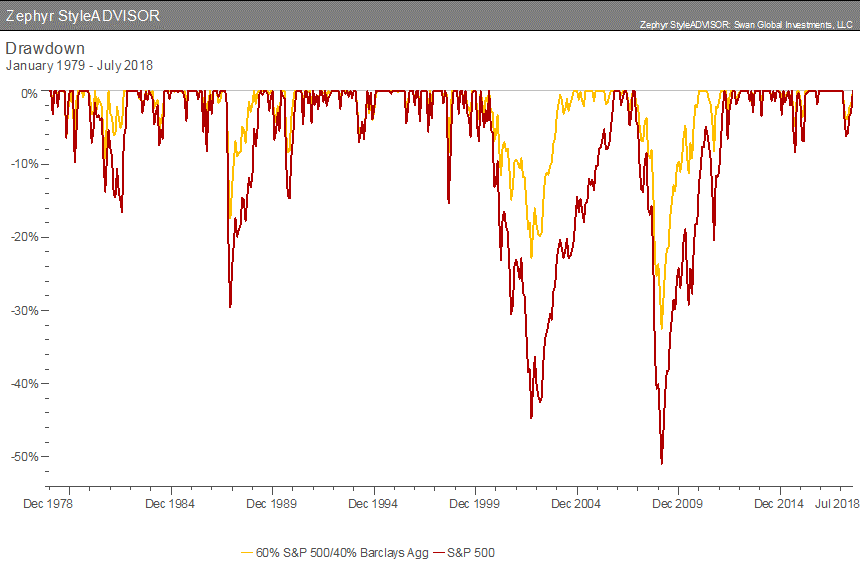

In the below graph, the red line represents the peak-to-trough losses associated with the S&P 500 from July 1997 to July 2018. If one were to fill in the entire area between the drawdown line and the break-even line, it would encapsulate three things: the depth of losses, the duration of losses, and the frequency of losses. These three results are exactly what the pain index measures.

Source: Zephyr StyleADVISOR

The pain index essentially measures the “volume” between the break-even line and the drawdown line. If the above lines are thought of as measuring cups, the pain index is the volume of liquid required to fill the drawdown space. The deeper the losses, the longer the losses and the more frequent the losses, the larger the volume of “pain.”

The steepest drawdown was the credit crisis of 2007-08 when the S&P 500 lost over 50%. However, the longest drawdown was the dot-com bust of 2000–2002. During that stretch, the market was down “only” 45% but took longer to recover its losses- 49 months for the dot-com bust, 37 months for the credit crisis, as we can see in the chart above.

Using the Pain Index Metric

When looking at the pain index measurement, the investor would prefer that volume to be as small as possible. The smaller the pain index, the better. A zero would be the best, indicating the manager never lost money.

The safest investments with the lowest pain indexes are likely to be those investments with scarcely any upside, like savings accounts, certificates of deposit, or money markets.

Measuring Risk how Most Investors Think about Risk

The pain index measures risk in terms most investors think about risk: how much money they might lose.

Putting risk in terms investors understand is important for helping them decide on funds and managers that suit their objectives and needs. Empathizing with their concerns and doing so with proper measurements can help you gain your clients’ trust and bolster your client relationship.

The pain index is great for investors who are more concerned with capital preservation above all else. But since investing is all about optimizing returns against risks, we ideally want a metric that measures the balance of the pain index against a measure of return. This is the purpose of the pain ratio, which I’ve discussed in a different post.

Marc Odo is the Director of Investment Solutions at Swan Global Investments, a participant in the ETF Strategist Channel.