At the same time, U.S. interest rates rose substantially, reducing a key risk to Consumer Staples stocks. As investors refocus on fundamentals in the current moderate economic growth environment, we believe stable earnings growth in the Consumer Staples Sector should support positive relative returns.

To fund the increase in Consumer Staples, we reduced exposure to the U.S. Health Care Sector, though we still maintain a very positive view of Health Care, which remains our largest U.S. sector overweight. The U.S. Health Care Sector provided strong absolute returns over the past year-and-a-half, roughly in line with the broad market. It had also materially outperformed in the second half of Q2 after the announcement of the Trump administration’s Blueprint to Lower Drug Prices reduced some investor uncertainty toward the sector. Overall, our allocation adjustments represented an opportunity to take advantage of recent market shifts without changing our aggregate target exposure to less economically-sensitive U.S. sectors.

![]()

International Outlook: We have seen some economic deceleration abroad recently, which is in line with our international outlook. For example, while Eurozone real GDP growth had briefly converged with the U.S. in recent years, the boost to Europe’s growth came largely from a rebound by its peripheral countries. We now are seeing European economic growth ease again, and a range of economic data has begun to disappoint relative to elevated market expectations. Structural challenges, like restrictive labor market regulation throughout Europe and political volatility in the periphery, present headwinds to sustained growth in the region.

We have been skeptical about how quickly the European Central Bank (ECB) would move off its highly accommodative monetary policy. Now, in fact, the ECB is undershooting broader investor expectations for normalization. In June, the ECB indicated it would not begin raising its overnight lending rate target until at least the summer of 2019. As the ECB keeps rates low, while the Fed continues to gradually tighten U.S. monetary policy, the differential between short-term interest rates in the U.S. and Europe will likely expand. This could drive capital flows from Europe to the U.S. and add to upward pressure on the U.S. dollar. That, in turn, could make European returns even less attractive for U.S. investors. Given these and other headwinds, such as the impact of Brexit and political uncertainty in Germany and Italy, we continue to underweight Europe in global portfolios.

Asia has its own structural headwinds, not least of which is continued consumer malaise in Japan. While Japanese equities have had occasional periods of outperformance in recent years, we have yet to see convincing signs of material sustained improvement in Japan’s economic fundamentals. Further, its ties to emerging Asian economies—notably China and South Korea, which face their own challenges—could make a meaningful turnaround even more challenging for Japan in the near-term. Emerging markets remain under threat from U.S. dollar strength.

Many emerging markets are dependent on foreign investment to fuel economic growth. A rising dollar also weighs on returns for foreign investors, making capital flight a risk. Additionally, key fundamentals in some emerging markets have deteriorated recently.

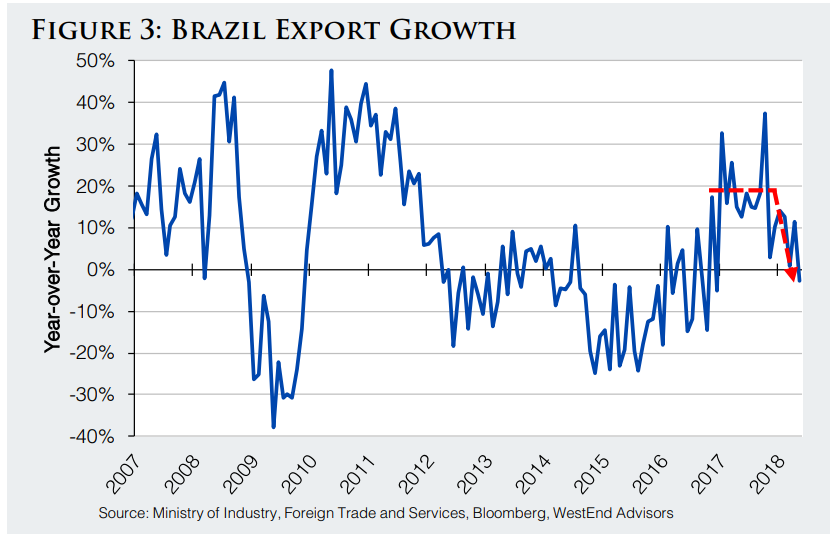

For example, the Chinese economy is increasingly reliant on internal consumption, but year-over-year growth in Chinese retail sales slowed to 8.5% as of May 2018, the slowest pace of growth since 2003. Separately, in Brazil, year-over-year export growth has slowed to 2.1% as of June from average growth of 18% in 2017 (see Figure 3).

Emerging market economies tend to be more reliant on exports than developed economies. This can make them particularly sensitive to even a modest deceleration in international economic growth. It also means that trade policy uncertainty in the U.S. (a key end-market for goods) can weigh heavily on emerging economies and markets.

U.S. Interest Rates: The trajectory of U.S. monetary policy is little changed over the past several quarters, and, looking forward, we still see the Fed gradually increasing the Fed Funds rate. This should continue to push up short-term interest rates in the U.S. Long-term interest rates have also moved up substantially from mid-2016 lows (though less than short-term rates) as inflation expectations increased and core inflation approached the Fed’s 2% long-run target. Normalization of real (after inflation) long-term interest rates, however, which remain low by historical standards, could sustain upward pressure on nominal longer-term rates.

In this environment, we are emphasizing short-duration securities in portfolios with fixed-income allocations. This protects against capital loss from longer-duration fixed-income securities as rates rise. Further, as the yield curve has flattened, the opportunity cost of this interest rate risk protection has declined because the amount of income forgone by holding short-term rather than long-term fixed income has decreased significantly.

Conclusion

Our intermediate-term economic outlook remains positive. In particular, many U.S. fundamentals appear to be in good shape.

We believe our strategies are well-positioned to take advantage of anticipated outperformance of select sectors in the U.S., such as Heath Care, Information Technology and Consumer Staples.

At the same time, we are always watching global economic and market risks. Many of the current risks are typical of a cycle that has progressed into its later stages, with interest rates rising and limited fuel for economic reacceleration. Other risks, such as the potential for a prolonged trade war, are unlikely to be realized in

our view, but we remain vigilant in our analysis of such factors.

As always, we will adjust portfolios as appropriate based on our evolving outlook.

Thank you for your interest and confidence in WestEnd Advisors. We invite you to contact us with any questions you may have on our outlook or portfolios.

This commentary was written by the team at WestEnd Advisors, a participant in the ETF Strategist Channel.

Disclosure Information

This report should not be relied upon as investment advice or recommendations, and is not intended to predict the performance of any investment. These opinions may change at anytime without prior notice. All investments carry a certain degree of risk including the possible loss of principal, and an investment should be made with an understanding of the risks involved with owning a particular security or asset class. Portfolio characteristics and/or allocations are generally averages and are for illustrative purposes only and do not reflect the investments of an actual portfolio unless otherwise noted. Portfolios that are concentrated in a specific sector or industry may be subject to a higher degree of market risk than a portfolio whose investments are more diversified. While every effort has been made to verify the information contained herein, we make no representation as to its accuracy.

The MSCI ACWI consists of 47 country indexes comprising 23 developed and 24 emerging market country indexes. The total return of the MSCI ACWI (Net) Index is calculated using net dividends. Net total return reflects the reinvestment of dividends after the deduction of withholding taxes, using (for international indices) a tax rate applicable to non-resident institutional investors who do not benefit from double taxation treaties. The MSCI Europe Index represents a subset of the MSCI ACWI, comprising 15 developed market country indexes in Europe. The Standard and Poor’s 500 Stock Index includes approximately 500 stocks and is a common measure of the performance of the overall U.S. stock market. An index is unmanaged and is not available for direct investment.

Holdings, Sector Weightings, and Portfolio Characteristics were current as of the date specified in this presentation. The listing of particular securities should not be considered a recommendation to purchase or sell these securities. While these securities were among WestEnd Advisors’ holdings at the time this material was assembled, holdings will change over time. There can be no assurance that the securities remain in the portfolio or that other securities have not been purchased. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities presently in the portfolio. Individual clients’ portfolios may vary. Upon request, WestEnd Advisors will provide a list of all recommendations for the prior year.