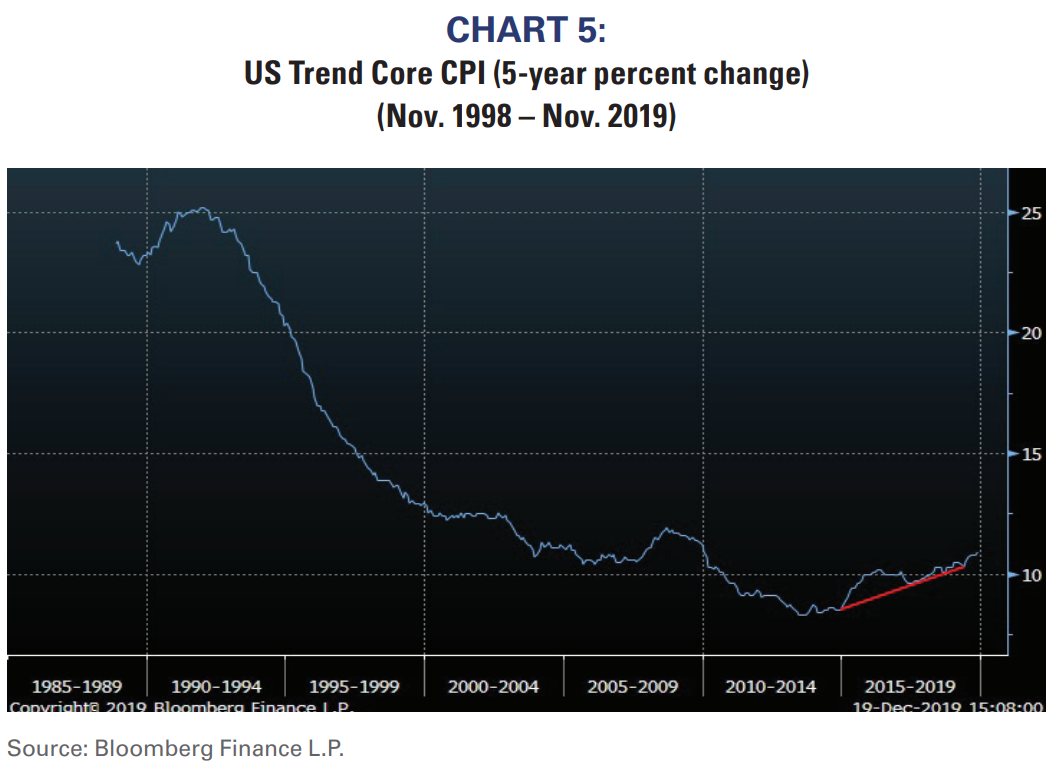

3) The five-year trend in core inflation is rising at the fastest pace in 30 years (see Chart 5).

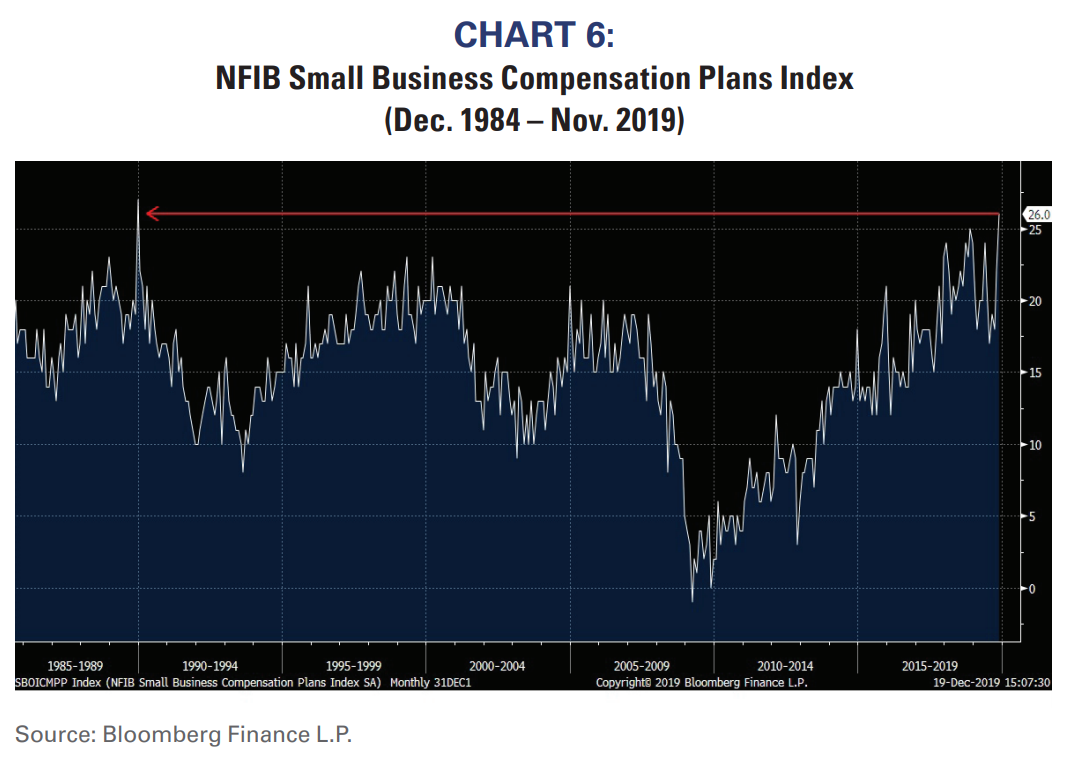

4) The NFIB compensation survey shows US small companies are planning to increase worker wages by the most in 30 years (see Chart 6).

EM vs. Venture Capital

In several earlier reports, we highlighted that Empirical Research Partners’ analysis showed nominal flows to venture capital and private equity funds have now eclipsed the flows into US equities during the late-1990s Technology Bubble. There is also roughly $2 trillion dollars of “dry powder” (i.e., capital committed by investors but not yet called by managers) waiting to be invested globally in venture capital and private equity.

One basic rule of investing is that return on investment is highest when capital is scarce. These recent data suggest that private markets are not starved for capital. Rather, these asset classes seem historically flush with capital. Financial theory argues that the high returns historically associated with venture capital and private equity

are highly unlikely to repeat.

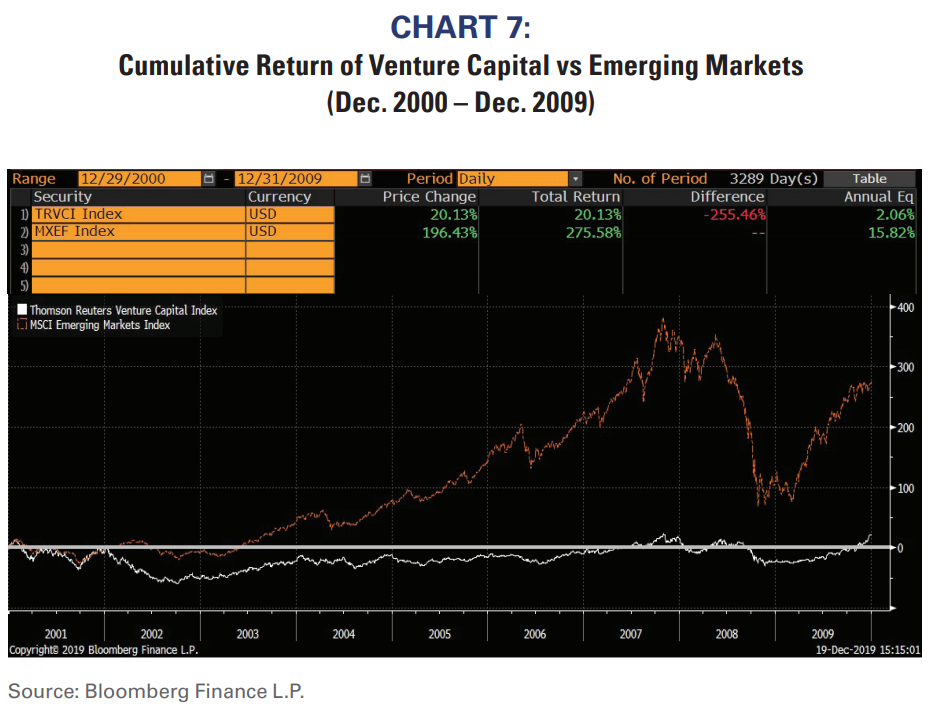

Charts 7 and 8 show how long-term performance trends can defy popular consensus. The first chart shows compounded returns for the Thomson Reuters Venture Index and for the MSCI Emerging Market Index from 2000 to 2009. 2000 (the start point in the chart) was the end of the Technology Bubble, but consensus remained that technology-related ivestments were a critical part of any growth

portfolio. Emerging Markets were at the other end of investors’ emotional scale because EM had suffered a series of financial catastrophes and were accordingly unpopular. However, Emerging

Markets subsequently outperformed Venture during the following decade by nearly 14 percentage points per year.

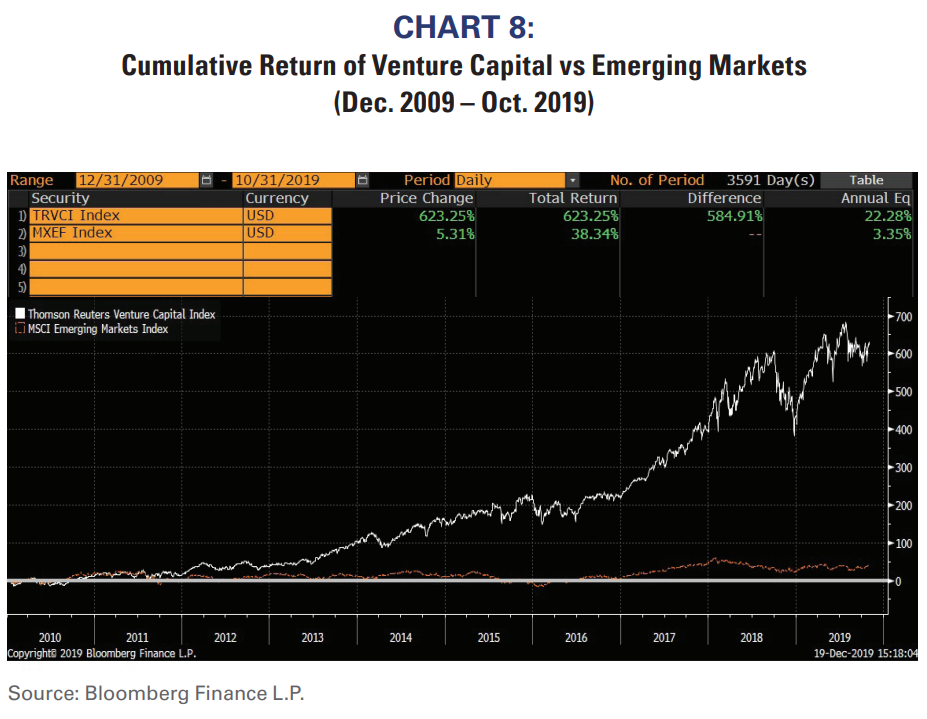

The situation was reversed by the end of the 2000s. Enthusiasm for Emerging Markets grew as the asset class outperformed, and by 2009/2010 Emerging Markets were considered a critical part of a portfolio. In fact, investors at that time were so enamored with Emerging Markets that many wouldn’t even consider our portfolios because those portfolios had little or no EM exposure. Technology related investments were largely unpopular because they had underperformed during the “lost decade for equities”. Venture Capital significantly outperformed EM over the subsequent decade by almost 20 percentage points per year.

Because technology-related investments significantly outperformed, Venture Capital is now once again considerably more popular than are Emerging Markets. Like the investment consensus in 2000, an allocation to Venture Capital today is widely considered essential by both institutional and individual investors.

There is no scarcity of capital in Venture Capital and returns are already starting to wane, but investors’ appetite for VC remains hearty.

Meanwhile, investors have largely shunned EM. It will be interesting to see how these two asset classes perform over the next decade, but history suggests that EM will outperform VC.

Admittedly, investors must balance the positive sentiment backdrop for EM with the potential negative of contracting global trade. Without being political, it is possible that the world simply

divides into the US and the non-US economies. The ongoing benefits of globalization might not be lost for EM in that case.

Tech becomes dreck

The Technology sector has been the biggest beneficiary of globalization.

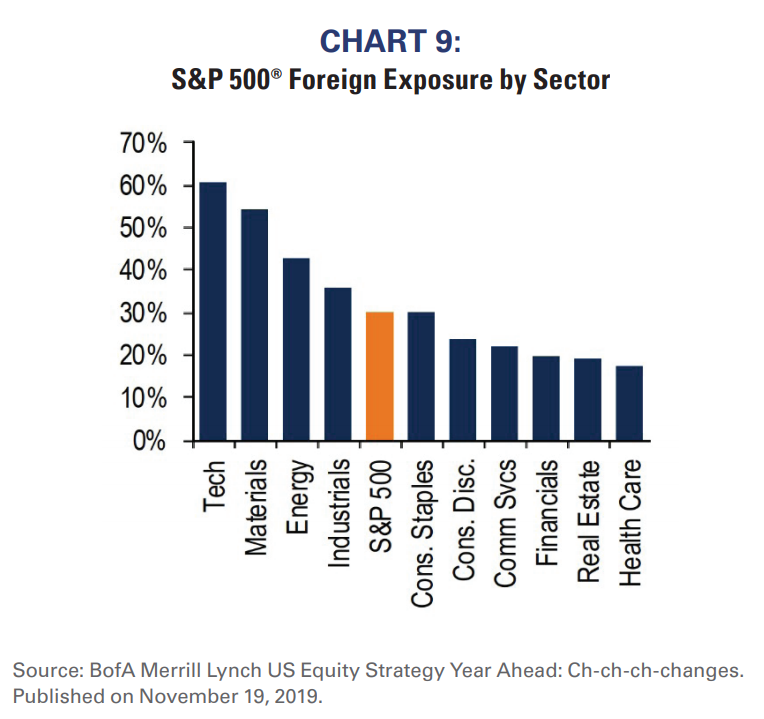

No other sector has such dispersed global supply chains or broad range of consumers around the world. A significant contraction in global trade could demonstrably change the profitability and growth trajectory of the sector. Chart 9 shows S&P 500® sectors’ foreign exposures (non-US sales as a percent of total sales). Technology is the most foreign exposed sector.

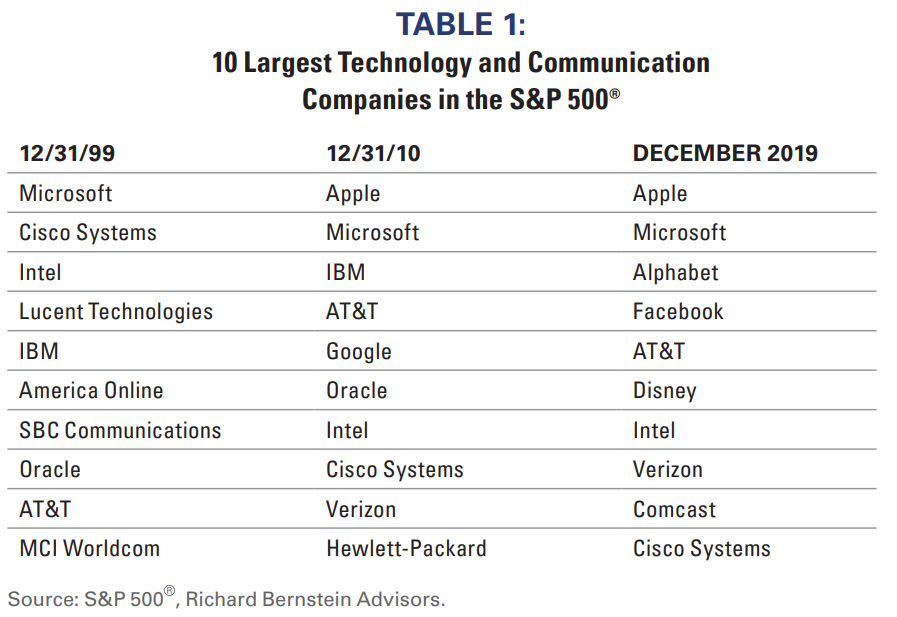

A contraction in global trade could make growth targets questionable for foreign exposed technology companies, but it is even harder to envision analysts’ lofty growth projections for the largest technology companies if antitrust regulation and disruptive capitalism continue over the next ten years. Table 1 shows the 10 largest Technology and Telecom companies within the S&P 500® as of December 31, 1999, December 31, 2010 and today. Only four companies appear in every column. Although some of the movement within the table is attributable to M&A activity, the table nonetheless reflects how difficult it is to maintain high valuations over long periods of time when success is based on significant and constant innovation.

Gold

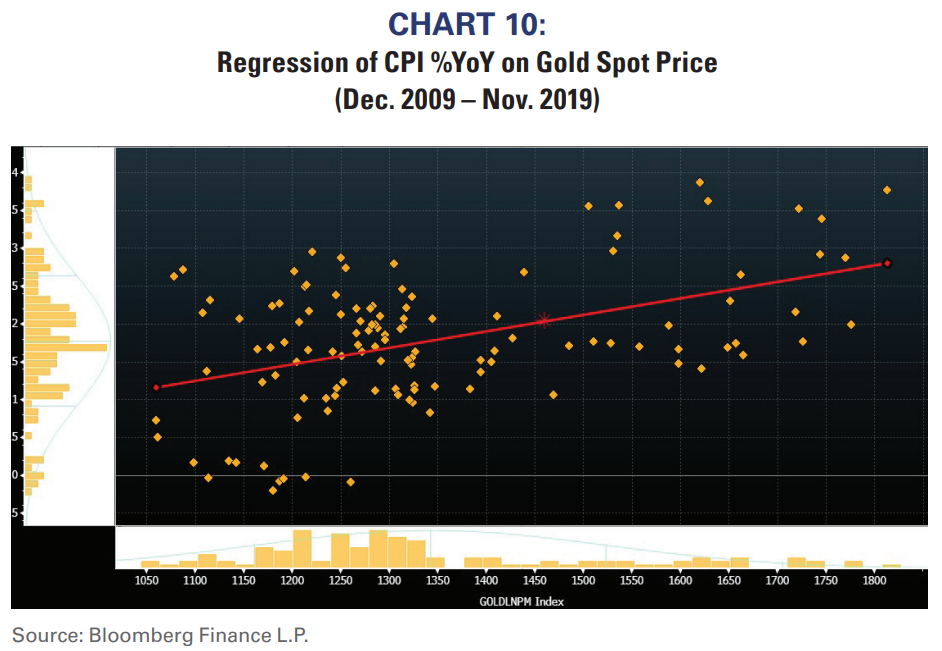

We’ve never been “gold bugs”, but it seems appropriate to hold gold if there is a secular contraction in globalization. First, as mentioned, limiting competition through trade barriers is inflationary and gold has historically hedged inflation well. Chart 10 shows that gold tends to appreciate as inflation rises. This certainly is not a perfect fit because there are many factors that influence gold prices. However, similar regressions for either stocks or bonds would yield a flat or negative relationship.

Second, our previous chart on trade uncertainty is one of many measures highlighting the current level of uncertainty is unprecedented, and gold has historically been a hedge against uncertainty and volatility. Third, gold could become a store of value in many parts of the world should the contraction in globalization become dire.

What’s in your time capsule?

Decades are all different, and the investment leadership in one decade has rarely been the leadership in the subsequent decade. We think the biggest investment theme over the next ten years could be the end of globalization.

If we could bury a time capsule and dig it up in ten years, we’d put EM and inflation-sensitive assets in that vault. There’s no guarantee that these themes will work, but we’re confident that the world will look

quite different at the end of the next decade and today’s popular investment themes (like venture capital, technology, and deflationary investments) will ultimately prove inappropriate.

Richard Bernstein Advisors is a participant in the ETF Strategist Channel.