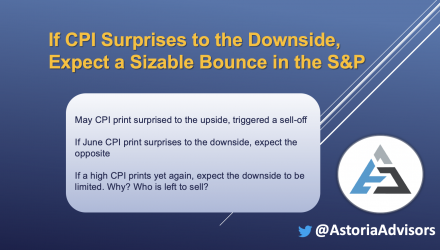

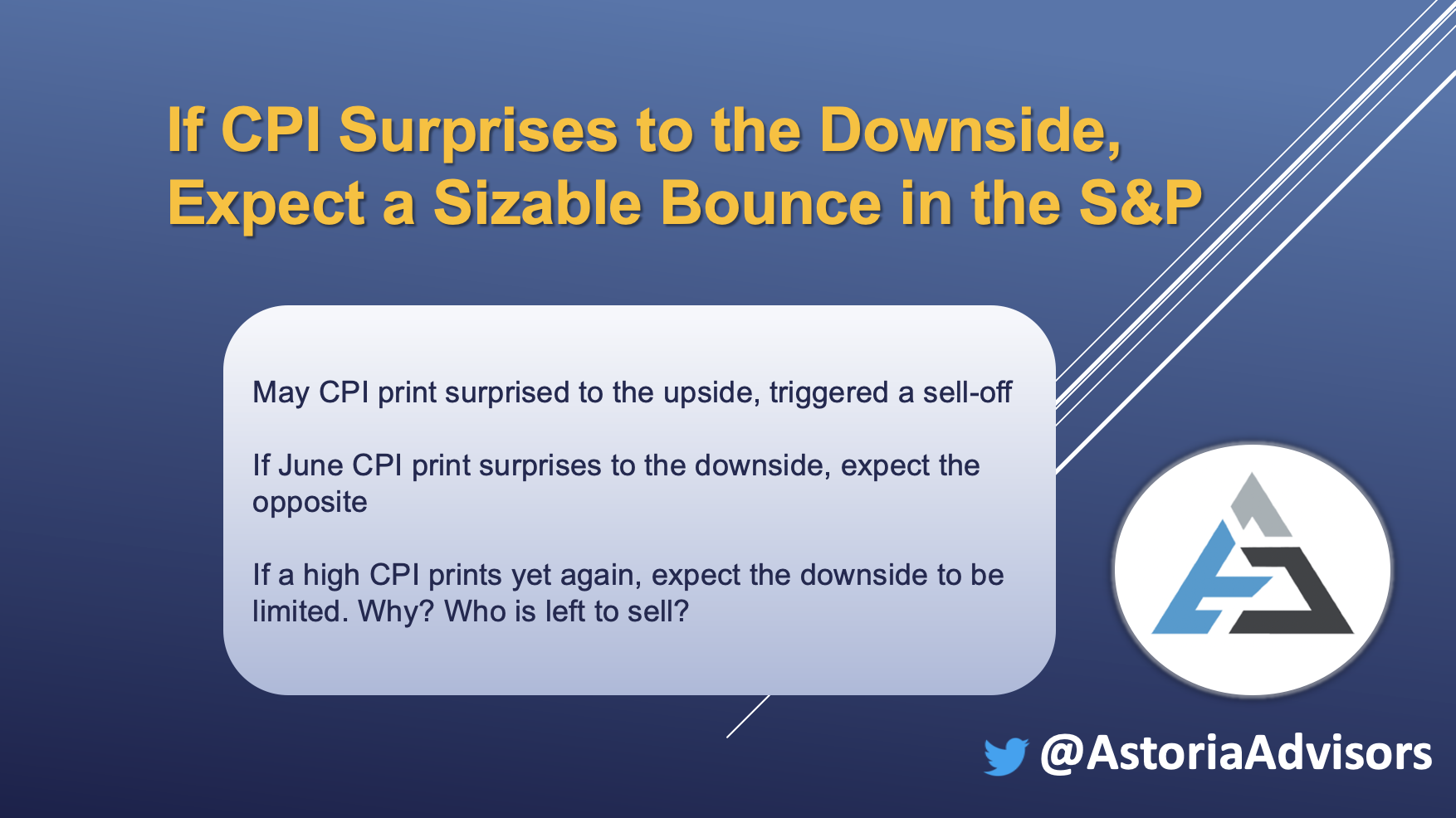

On June 9th, we distributed a piece (click here) arguing that if CPI surprised to the upside, the S&P would fall precipitously. This came to fruition as June was disastrous for risk assets.

Just as the markets sold off on last month’s unexpected CPI overshoot, they could equally move sharply higher if this week’s CPI report surprises to the downside. Why? YTD, we’ve seen near-record market outflows in stocks and bonds, overwhelming bearish sentiment indicators, and meaningful leverage has been taken out of the system between day traders, crypto, & SPACs. In our view, current market positioning is advantageous for any downside surprise to this week’s CPI.

Contrarily, if CPI surprises yet again to the upside, we expect the downside to be limited. Why? Who is left to sell?

There are record shorts in S&P 500 futures (see chart below from @MacroCharts using data from CFTC).

We wrote in last week’s Q3 investment outlook (click here) that Astoria believes we are at peak negative sentiment, fund positioning, & peak Fed hawkishness.

Thus far, 2022 has proven to be the antithesis of 2021. Whereas last year was characterized by easy money, peak economic growth, and peak corporate profits, 2022 has seen a tightening of financial conditions, lower economic growth, and slower corporate profits. According to Morgan Stanley research, this is the worst first-half return for the S&P 500 (-20%) since 1962, US High Yield bonds (-10.2%) since 1989, Japanese Yen (-15.2%) since 1989, and US 10Y (-10.8%) since the 1970s.

We now think sellers have exhausted themselves, and the market could rebound swiftly if CPI comes in softer.

The damage has already been done by the Fed’s draconian rate hikes. Commodities nearly across the board have seen a sizable correction. Since June 8th, XLE (Energy super majors), PDBC (energy/oil commodity-centric ETF), and USO (crude oil futures) are down 18-24%.

Astoria’s bottom line: the market has experienced its worst 1st half in nearly half a century. All asset classes have now seen meaningfully historical P/E contractions; that’s a good thing. We’re not ready to back up the truck just yet, but we think it is time to start nibbling on stocks/credit (this was the title of our Q3 outlook).

The thin summer liquidity of markets will exacerbate volatility to any upside or downside surprise in CPI/PPI.

Astoria offers two Risk Managed solutions to help investors navigate turbulent markets. Click below for our factsheets.

Multi-Asset Risk Strategy Fact Sheet

Risk Managed Dynamic Income Strategy Fact Sheet

Click here for original publication

For more news, information, and strategy, visit the ETF Strategist Channel.

Astoria Portfolio Advisors Disclosure: As of this publication Astoria Portfolio Advisors held positions in XLE, PDST, and USO on behalf of its clients. Past performance is not indicative of future performance. Any third-party websites provided on www.astoriaadvisors.com are strictly for informational purposes and for convenience. These third-party websites are publicly available and do not belong to Astoria Portfolio Advisors LLC. We do not administer the content or control it. We cannot be held liable for the accuracy, time-sensitive nature, or viability of any information shown on these sites. The material in these links is not intended to be relied upon as a forecast or investment advice by Astoria Portfolio Advisors LLC and does not constitute a recommendation, offer, or solicitation for any security or investment strategy. The appearance of such third-party material on our website does not imply our endorsement of the third-party website. We are not responsible for your use of the linked site or its content. Once you leave Astoria Portfolio Advisors LLC’s website, you will be subject to the terms of use and privacy policies of the third-party website. Refer here for more details.

Photo Source: Astoria Portfolio Advisors