{kind=link}

Daily, Astoria monitors and tracks largely followed macroeconomic indicators to help us gauge the health of the US economy (please contact us if you’d like to be added to our distribution list). We look at the data that comes in versus consensus estimates, as well as if the data has improved or deteriorated relative to prior months. Such data assists in identifying which stage of the economic cycle we are in.

As readings have weakened significantly relative to the prior year, we are specifically paying attention to the rate of change and troughs in the data that suggest the economic environment is improving. Recognizing these trends is vital for our investment decision making process and aids in dictating Astoria’s views around portfolio construction.

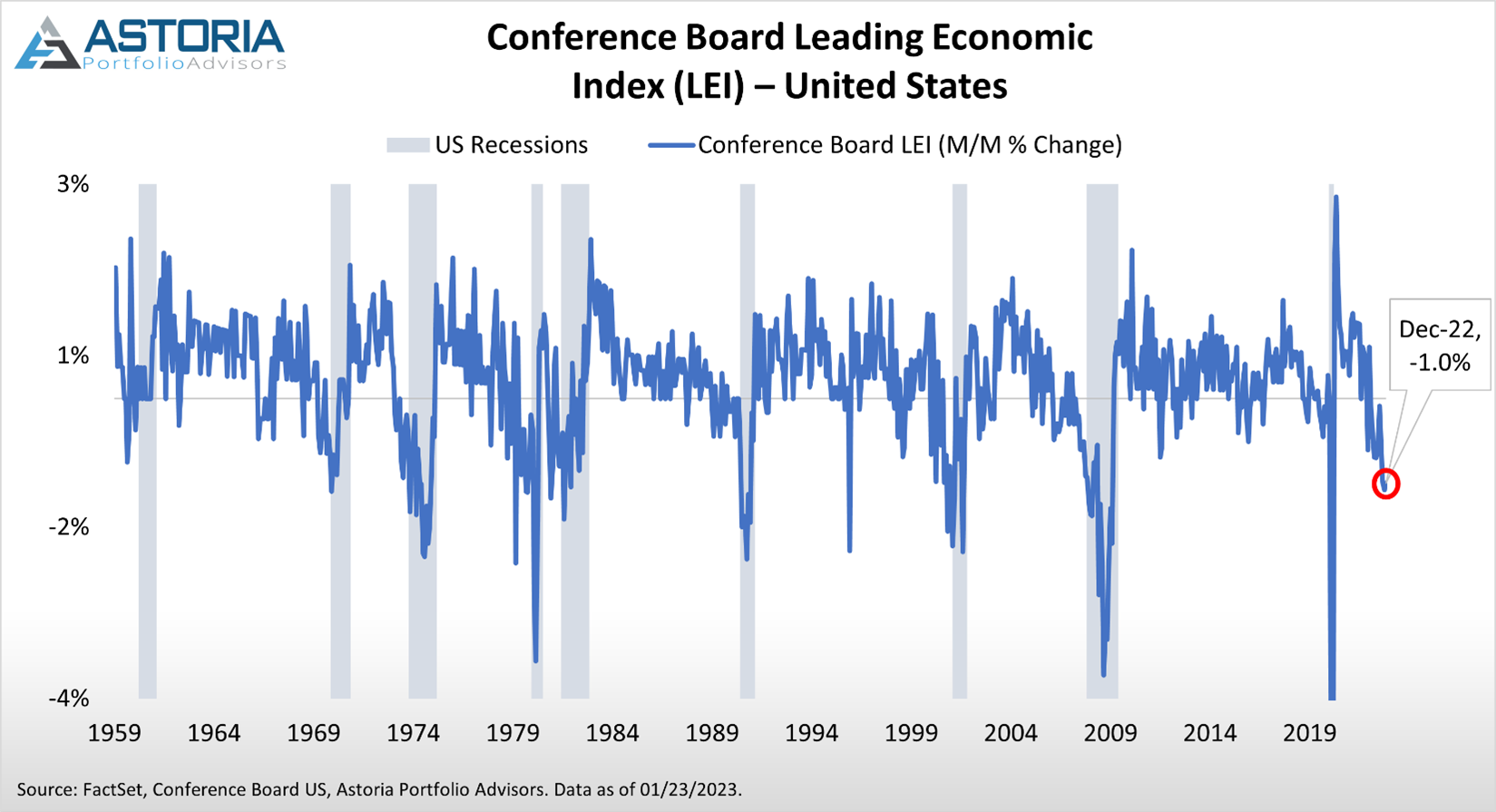

For example, the excerpt below provides an update on the latest Conference Board Leading Economic Index release, which is often seen as a highly important leading economic indicator. As published in our writing and research, Astoria feels that it’s hard to be constructive when leading economic indicators continue to roll over:

- The Conference Board Leading Economic Index (LEI) registered -1.0% MoM in December, lower than the expected -0.7% print but up slightly from November’s 1.1% decline. Marks the 10th straight monthly decline for the index and indicates a negative short term outlook for the US economy.

{kind=link}

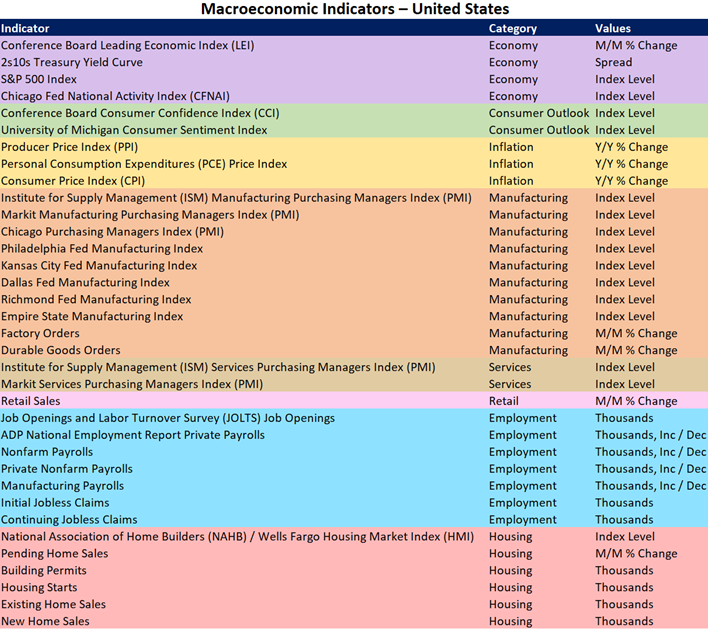

Below is a table displaying other key indicators we track, the category they provide significance for, and the respective values of the data.

{kind=link}

Each category suggests different implications as detailed below:

- Negative / positive short term outlook for economic activity or contraction / growth of economy

- Optimistic / pessimistic consumer outlook regarding the health of the economy

- Weakening / strengthening of manufacturing activity / servicing sector given declining / improving demand for goods / services

- Declining / improving retail demand given elevated / cooling inflation and high / falling borrowing costs

- Struggling / resilient labor market as total number of job openings or payrolls fell / grew

- Deteriorating / strengthening in the housing market as demand weakens / increases amid rising / declining mortgage rates

Although much of the data remains poor and signals a looming recession, we acknowledged that some of the indicators we track have begun to trough.

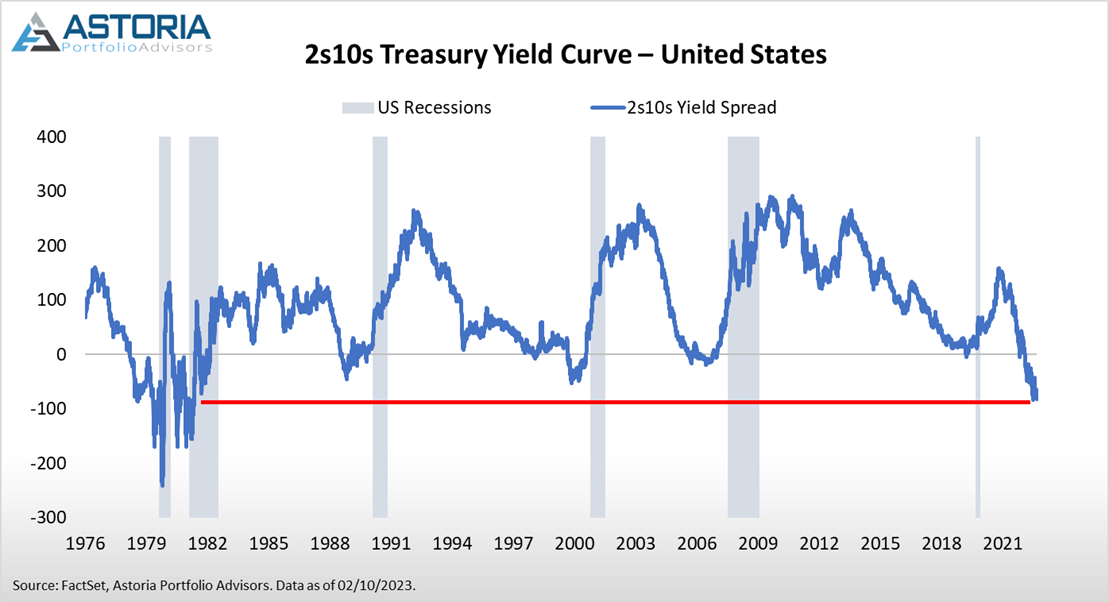

For instance, as previously noted, the Conference Board LEI continues to show signs of economic weakness. Additionally, one of the economy’s most renowned leading indicators, the yield curve, continues to invert. Such inversions have historically preceded recessions. As pictured below, the spread between the 2-year and 10-year US Treasury yields recently notched its most inverted level in approximately 40 years.

{kind=link}

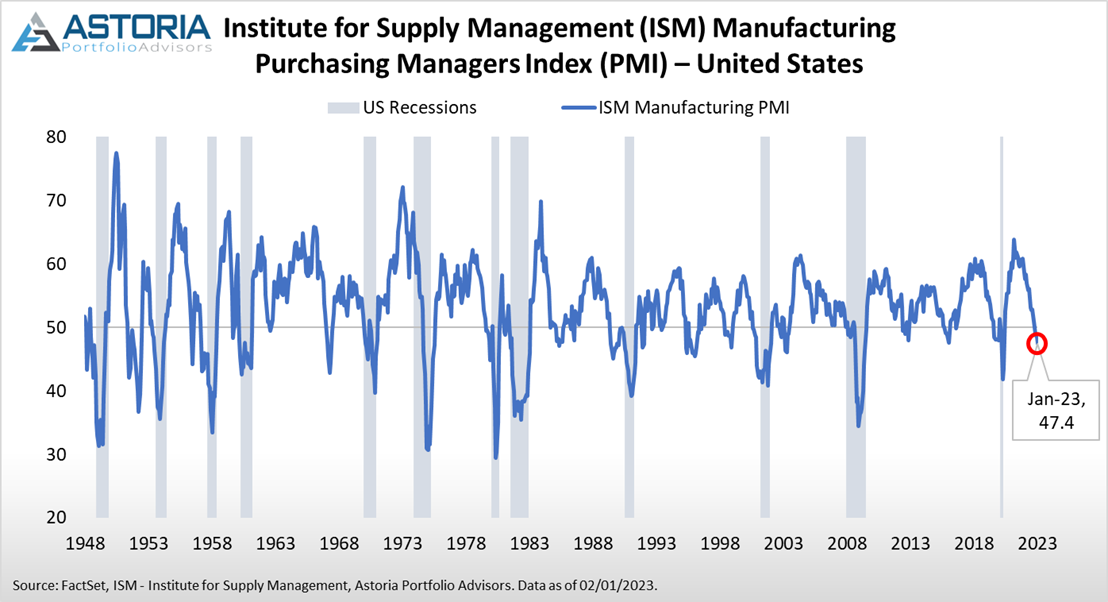

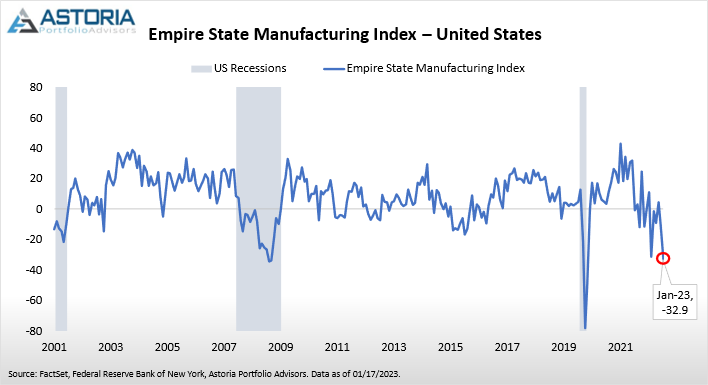

Moreover, the following indicators continue to worsen:

{kind=link}

{kind=link}

{kind=link}

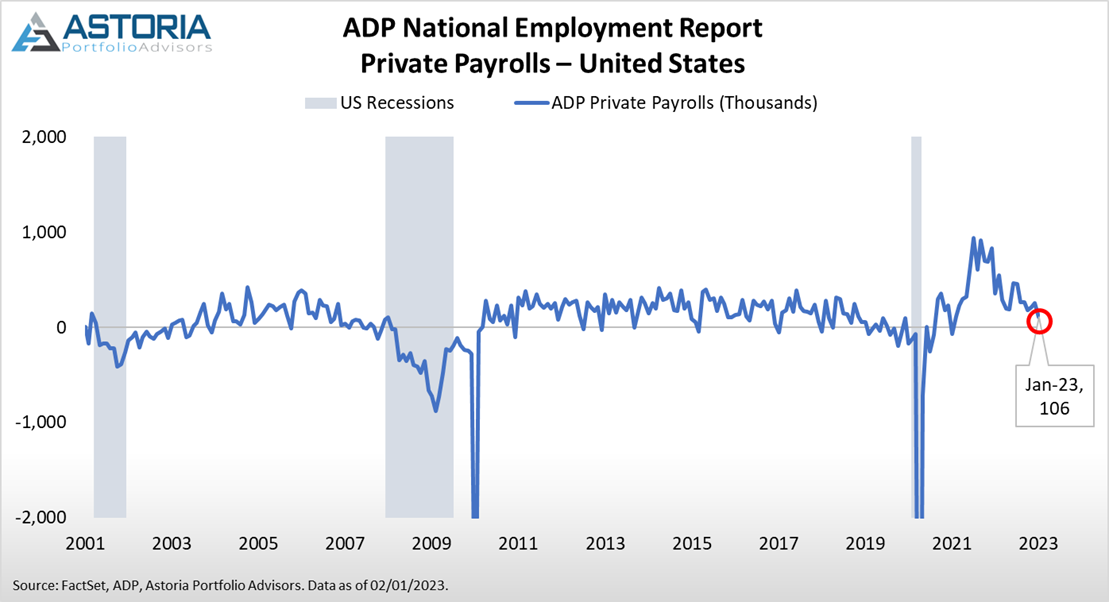

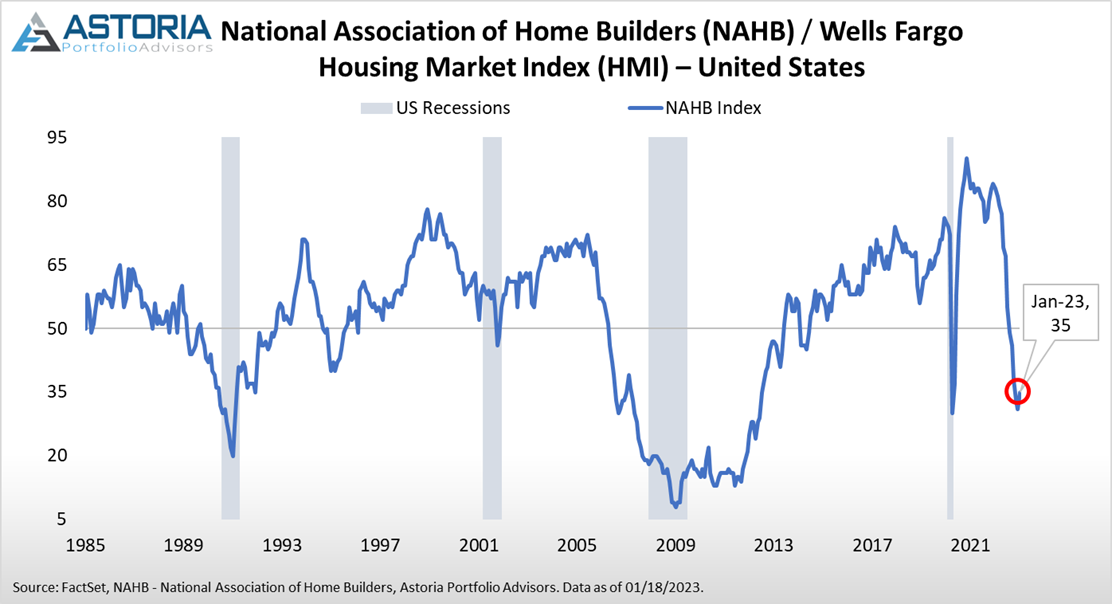

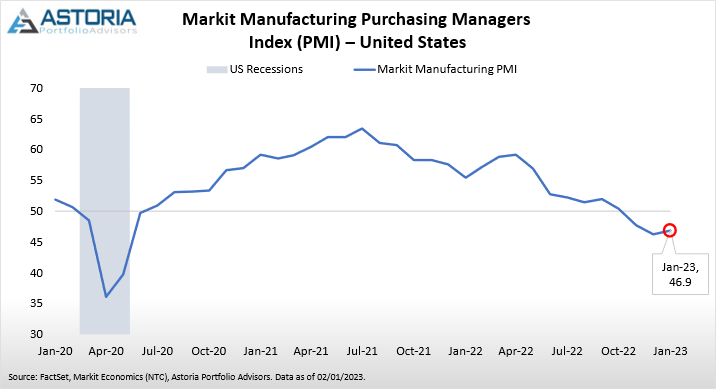

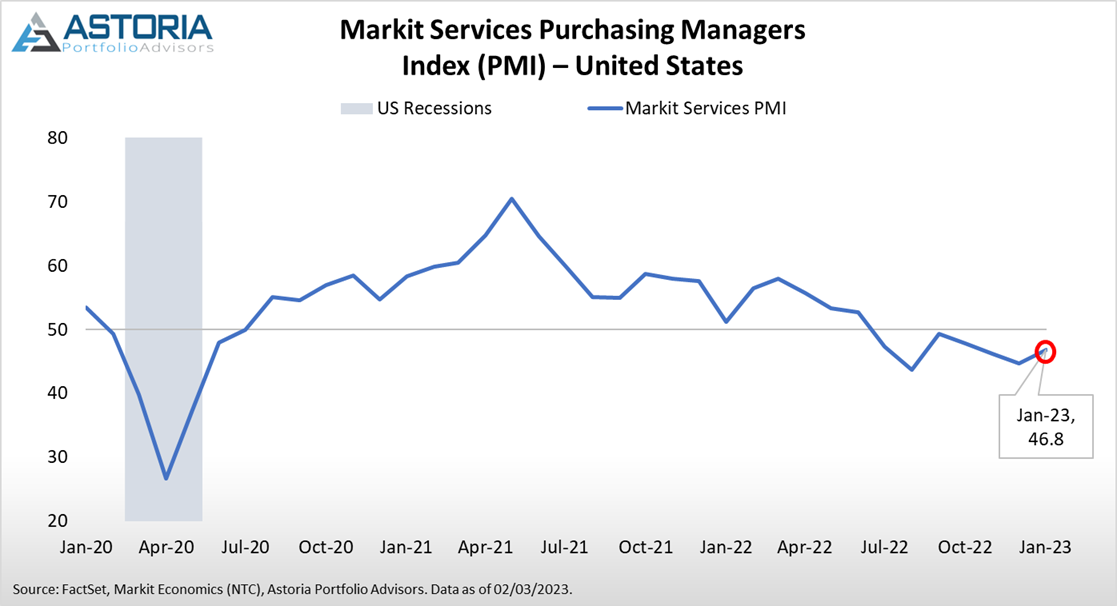

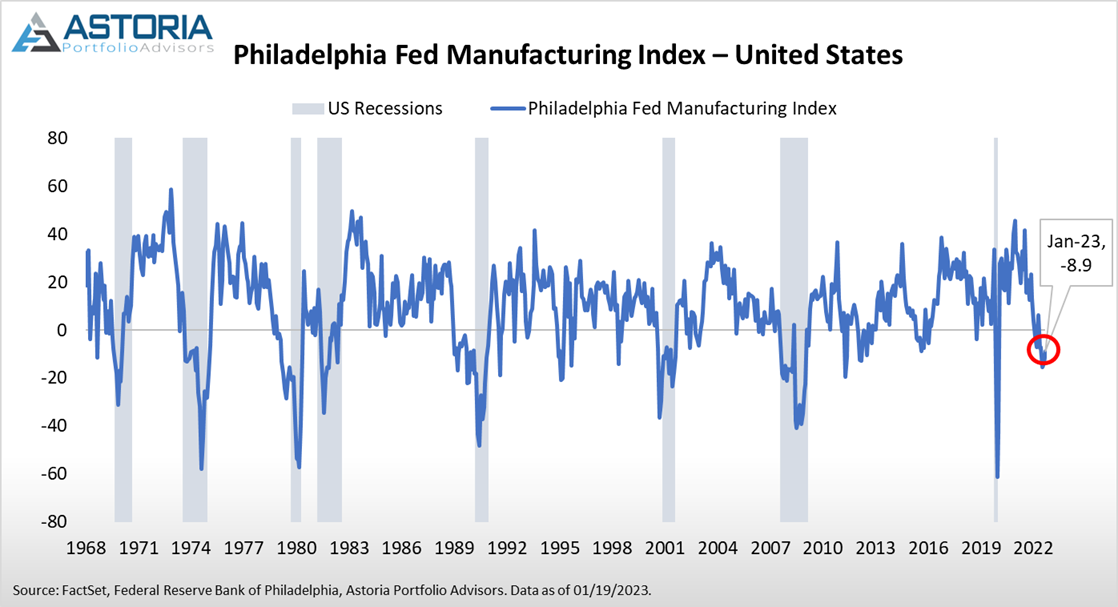

Meanwhile, the below indicators seem to have troughed but remain in contractionary territory:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Keep in mind that economic turnovers have historically occurred after the Fed pauses, which proposes that the economy may still experience more hardship in the months to come. Astoria is currently more defensively positioned, though not as extreme as we were in 2022. We have lengthened our bond duration, maintain a healthy allocation to alternatives, and remain titled away from growth and towards value/quality-centric assets. For a more in depth view of our current portfolio construction views, please refer to our 2023 Outlook Report (click here).

Best,

Nick

Source: FactSet. Data accessed at the time and date of indicator’s latest release as of February 14, 2023.

Past performance is not indicative of future performance. Any third-party websites provided on www.astoriaadvisors.com are strictly for informational purposes and for convenience. These third-party websites are publicly available and do not belong to Astoria Portfolio Advisors LLC. We do not administer the content or control it. We cannot be held liable for the accuracy, time-sensitive nature, or viability of any information shown on these sites. The material in these links is not intended to be relied upon as a forecast or investment advice by Astoria Portfolio Advisors LLC and does not constitute a recommendation, offer, or solicitation for any security or investment strategy. The appearance of such third-party material on our website does not imply our endorsement of the third-party website. We are not responsible for your use of the linked site or its content. Once you leave Astoria Portfolio Advisors LLC’s website, you will be subject to the terms of use and privacy policies of the third-party website. Refer here for more details.

Photo Source: Astoria Portfolio Advisors