By Rob Williams, Director of Research

This year has been a rough ride for fixed income investors. The good news is that we expect fixed income investors to be rewarded with positive returns in the near term and meaningful upside potential over the intermediate term. The following are a few compelling reasons to be bullish on fixed income.

- Strong Returns Ahead for Fixed Income. In the near term, we expect positive returns, which will be driven by more attractive yield carry and range-bound rates caused by recession fears. And in the intermediate term – the next 6 to 18 months – we see larger upside potential as rates have overpriced Fed rate hikes and wider spreads should lead to attractive valuation opportunities.

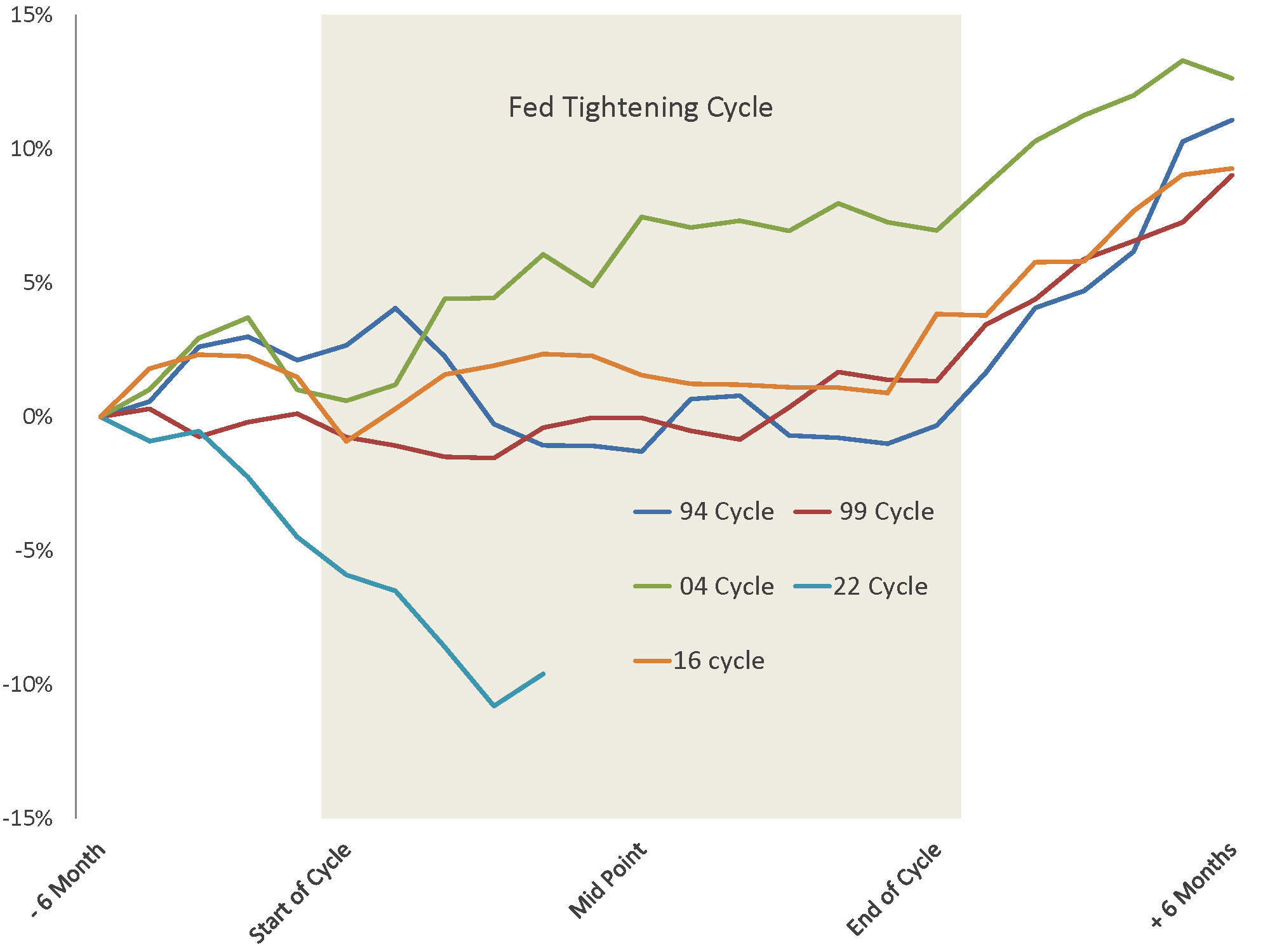

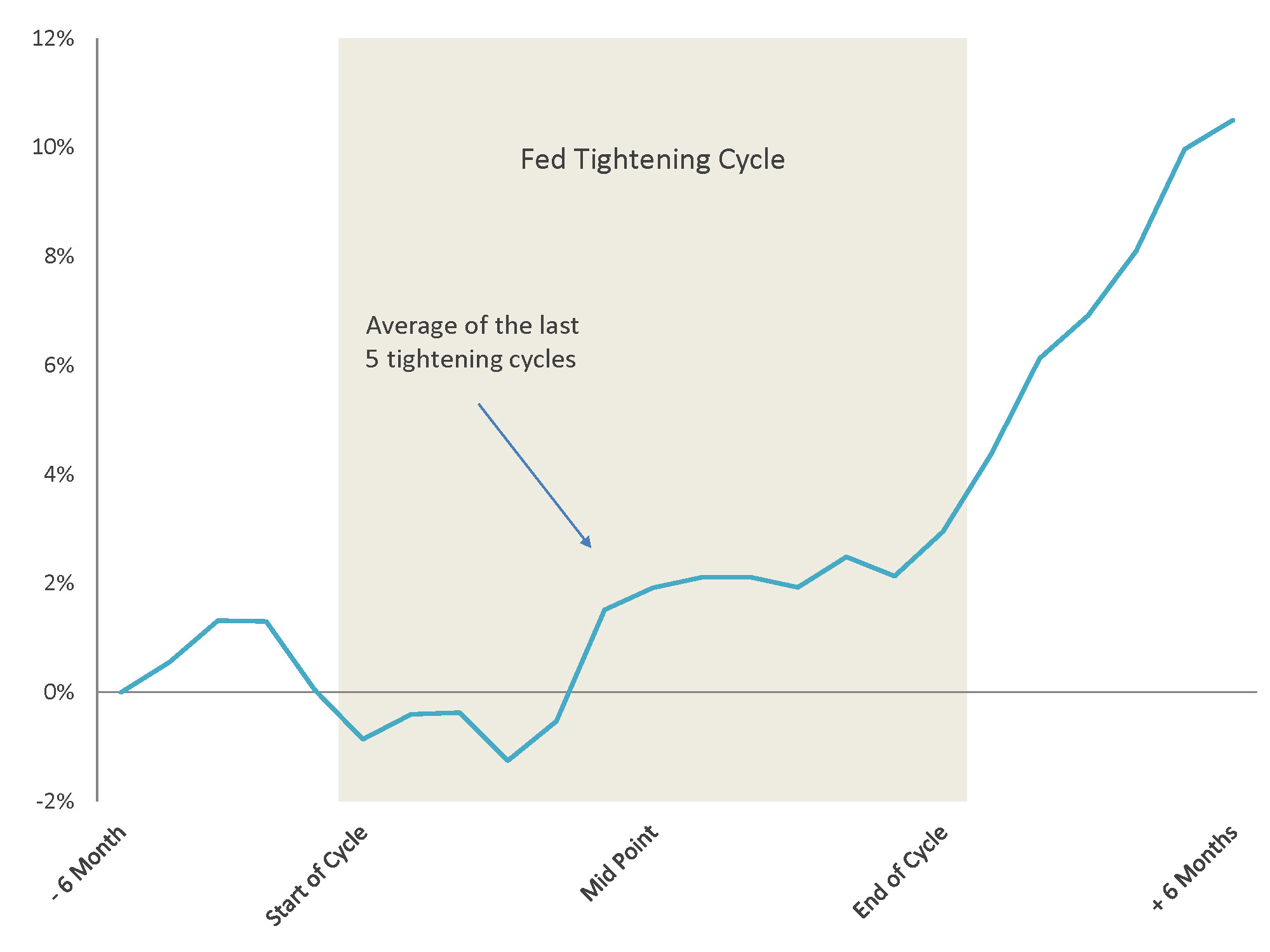

Aggregate Bond Index Returns During Tightening Cycles

Source: Sage, Bloomberg

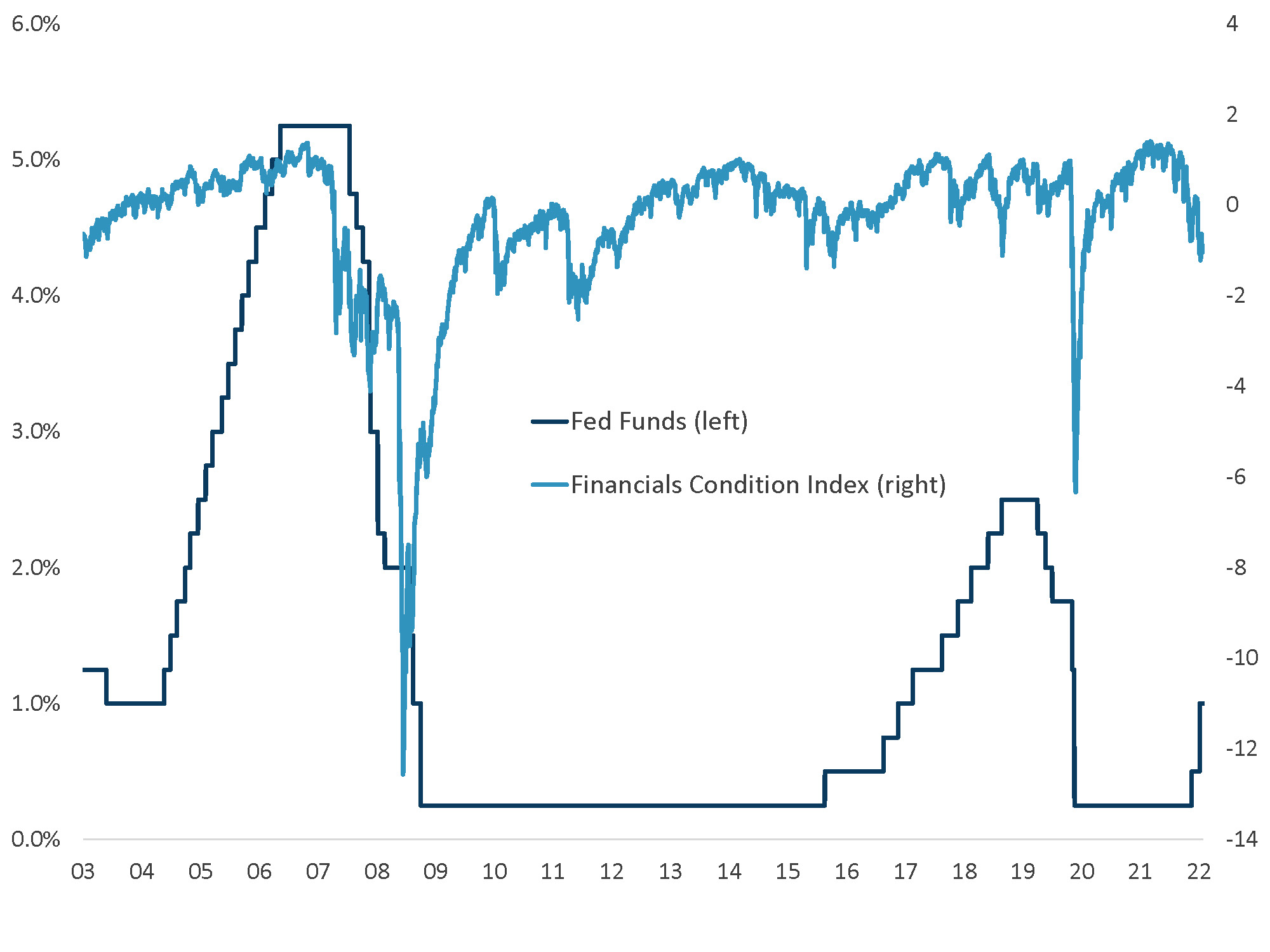

- Rate Markets are Overestimating Fed Hikes. Sinking markets, tightening financial conditions, and weakening growth will make it tough for the Fed to stay aggressive in its rate hiking plans. We believe it will be difficult for the Fed to hike above 2.25% or hike beyond 2022.

Fed Funds Target Rate vs. Financial Conditions Index

Source: Sage, Bloomberg

- We’re Entering the Part of the Rate Cycle Where Returns Usually Improve. Rates have already adjusted for Fed hikes, suggesting a downside rate move if the Fed is unable to follow through on all planned hikes. This isn’t surprising to us. It is not unusual for markets to overshoot, and we are in the part of the cycle where returns tend to improve.

Aggregate Bond Index Returns During Tightening Cycles

Source: Sage, Bloomberg

- Fixed Income’s Relative Attractiveness Has Also Improved. With yields moving higher, fixed income is more compelling vs. the dividend yields and earnings yields of equities. Large gains in equities since the onset of the pandemic coupled with the recent drawdown in fixed income and recession fears suggest asset allocation rebalancing and flows should favor fixed income in the coming months.

Equity Earnings Yields and Fixed Income Yields

Source: Sage, Bloomberg

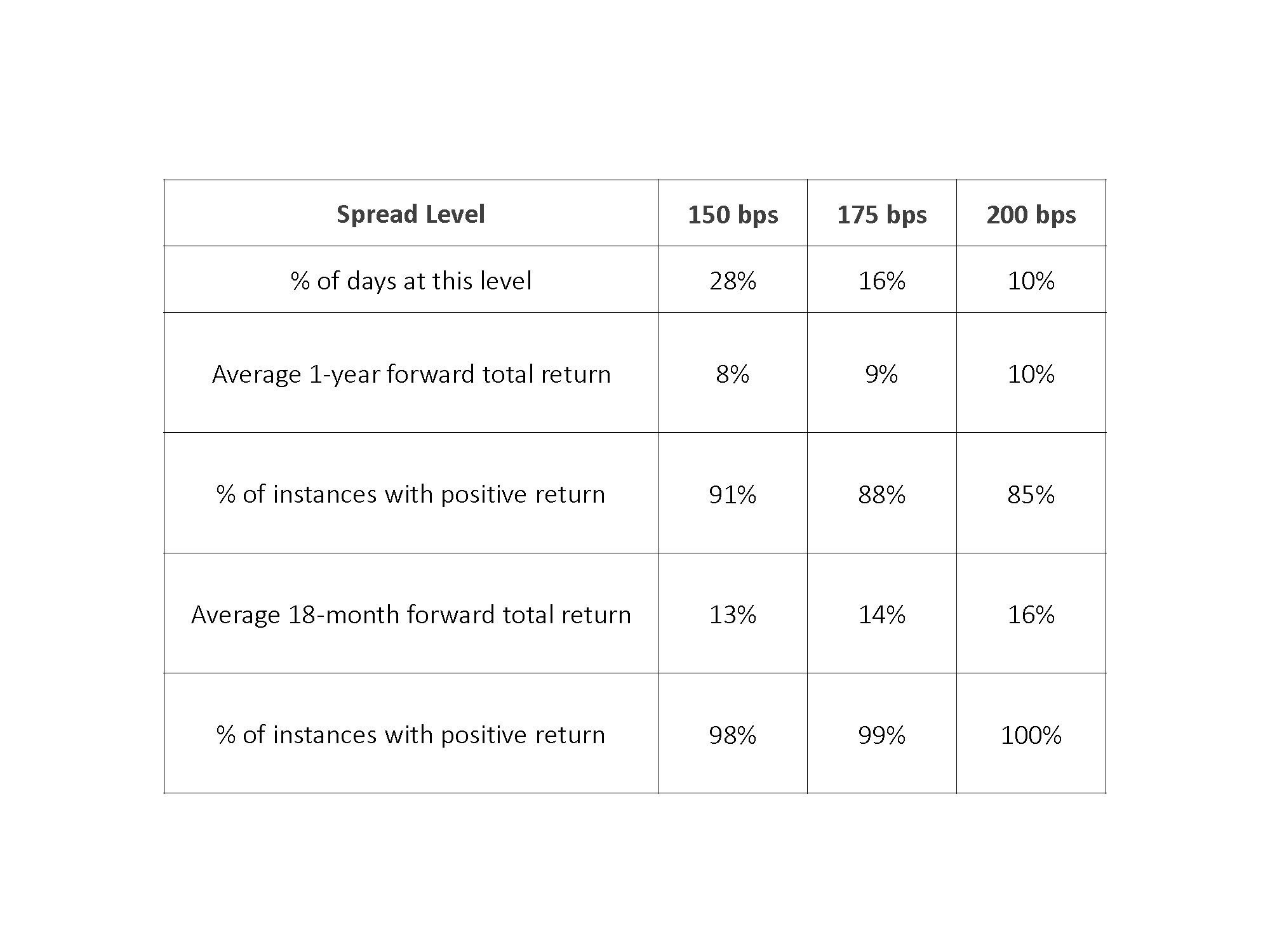

- Credit Spreads are Entering the “Interesting” Zone. While growth concerns and balance sheet tightening could continue to pressure spreads in the near term, valuations are better compensating for these risks and suggest upside opportunities. When spread levels pass 150 bps, there is an increased likelihood of positive returns, and the level of returns starts to become attractive for 1 year-plus holding periods.

Return Expectations Given Spreads

Source: Sage, Bloomberg

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.