By Doug Sandler, CFA, Head of Global Strategy

SUMMARY

In a Bear Market:

- Defense matters – We have lowered stock weightings.

- Position sizing matters – Due to the greater volatility.

- Yield matters – Hence our preference for ‘PATTY’ themes.

Here’s how this Reality has Played out in our Balanced Portfolios for Bear Markets

The Major League Baseball (MLB) conference championships have begun with the winners going to the World Series and the losers going home. Games with high ‘stakes’ demand strategies that differ from those used throughout the 162-game regular season. Investment strategies should also adapt to the size of the stakes, in our opinion. Studies show that investors feel losses twice as acutely as gains, bear markets carry higher stakes than bull markets. We believe this can lead to loss aversion behavior that causes one to abandon an appropriate financial plan at or near market bottoms.

Given that financial markets are officially in ‘bear’ territory, our strategies have adjusted in three ways, which have affected the positioning of RiverFront’s balanced portfolios.

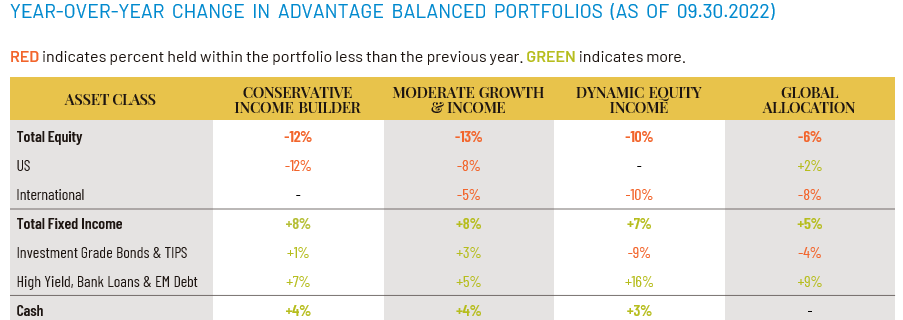

1. Defense matters: The statement that ‘defenses win championships’ is not only true in baseball, but also investing, in our view. The simplest way to be defensive is to allocate fewer dollars to riskier assets, like stocks. Each of RiverFront’s balanced portfolios have reduced their stock allocation throughout the last 12-months and currently carry fewer stocks than they would in a bull market. Our stock reductions have ranged from 6-13% over the last 12-months, with the largest reductions occurring in our shorter horizon, more conservative portfolios (see table below).

{kind=link}

{kind=link}

Change is calculated based on portfolio holdings from 09.30.2021 versus 09.30.2022. Past performance is no guarantee of future results. Shown for illustrative purposes only. Holdings subject to change.

2. Get on base: There are times to ‘swing for the fences’ and there are times to target getting on base. We believe the latter is a better strategy in the play-offs and during bear markets. In the play-offs, only the best pitchers pitch and they are often throwing their best stuff. According to a 2018 MLB study, the average play-off fastball in 2017 was a full one mile-per-hour faster than those thrown during the 2017 regular season. Therefore, ‘swinging for the fences’ in the post-season carries a higher risk of striking out.

Shifting to investing, bear markets also present unique and difficult challenges. Stock and bond markets that move in value by multiple percentage points in a day or swing wildly from positive to negative over a short period of time, are great examples of these challenges. In these types of markets, we place particular emphasis on sizing our positions appropriately so that no one position, or trade, has outsized (‘strike-out’) impact on our portfolios. A few areas that we currently like include:

- We like higher yields on bonds: It has been painful for investors this year in fixed income. However, as a result of yields rising, we see opportunities in bonds to benefit from current yield levels – the Bloomberg Aggregate is yielding 5.15% as of October 21, 2022.

- We like US stocks relative to International: The US is still the strongest major economy in the world with less exposure to geopolitical issues in Europe and Asia, in our view. International stocks, while looking more attractive from a valuation perspective, possess structural growth concerns and contagion risks are higher.

- We like the US Dollar: We believe that the US Dollar will continue to appreciate against most foreign currencies, and we are hedging a portion of our non-Dollar exposure in our portfolios.

- We like ‘stock picking’: We continue to favor more granular security selection, favoring investments that we think can benefit or quickly adjust to the new geopolitical reality – a ground war in Europe and a ‘cold war’ in Asia.

3. Favor the players that can deliver: Hall of Famer Reggie Jackson was nicknamed ‘Mr. October’ because he could be relied upon in the post-season. He may not have always played his best in the regular season, but when the stakes went up, he consistently shone. We believe that financial markets have their own version of Reggie Jackson, which we have nicknamed ‘PATTY’. PATTY stands for Pay Attention to The Yield, which is another way to say: favor the investments that are delivering results when it counts. Not every stock or bond fits this classification. A few examples of investments that fall into either category include:

- Favor: Inflation recovery plays: We anticipate that the earnings of companies in the energy and mining industries will be resilient because they typically respond positively to inflation and nominal growth. Additionally, we favor countries and regions like Canada, Australia, Norway, and Latin America that export commodities while avoiding the conflict in the Ukraine and tensions with China.

- Favor: Mega-cap, high cashflow technology: Companies with multiple connections to consumers and businesses can use their dominance and scale to maintain sales and pricing power, in our view.

- Favor: Bonds: With Treasury yields at 4% or better from 3-month bills to 30-year bonds as of Friday, we expect a significant shift from equities to fixed income. For example, retirement plans modeled to payout a 4% distribution, can fully ‘lock-in’ a portion of that future liability by purchasing Treasuries today.

- Favor: Healthcare: We believe healthcare-related investments can continue to deliver revenues, earnings and cashflow since their products and services tend to be non-discretionary and their business models are often protected by regulations.

- Avoid: China: China’s apparent crackdown on capitalism, uncomfortably close relations with Russia and its increasing isolation from the West have soured investors on investing in the region. We believe it will take many years to reverse this psychology and thus do not view China-related investments as fitting the PATTY profile.

- Avoid: Expensive growth stocks: Expensive growth stocks are the poster child for ‘non-PATTY’ investments. While we think there are plenty of great companies with good long-term potential in this category, many are unable to deliver earnings, dividends and/or cashflows today. For this reason, we expect them to attract less attention in bear markets, when investors demand greater certainty and reliability.

- Avoid: Consumer Discretionary: The US consumer is being battered by the high costs of essentials such as rent, food and gasoline. Therefore, the pressure on revenues, earnings and cashflow in the near-term will be significant, in our view.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Important Disclosure Information:

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Index Definitions:

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

Bloomberg US Aggregate Bond Index TR USD (Fixed Income Investment Grade) is an unmanaged index that covers the investment grade fixed rate bond market with index components for government and corporate securities, mortgage pass-through securities and asset-backed securities. The issues must be rated investment grade, be publicly traded and meet certain maturity and issue size requirements.

Conservative Income Builder Composite Benchmark (Benchmark): The Composite Benchmark is currently a blend consisting of 30% S&P 500 Index TR and 70% Bloomberg US Aggregate Bond Index TR that is rebalanced monthly. The S&P 500 Index TR measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market. The Bloomberg US Aggregate Bond Index TR is an unmanaged index that covers the investment grade fixed rate bond market index components for government and corporate securities, mortgage pass-through securities and asset-backed securities.

Moderate Growth and Income Composite Benchmark and Conservative Growth Composite Benchmark (Benchmark): The Composite Benchmark is currently a blend consisting of 40% S&P 500 Total Return Index TR, 10% MSCI EAFE Net Total Return (NR) USD Index and 50% Bloomberg US Aggregate Bond Index TR that is rebalanced monthly. The S&P 500 Index TR measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

Dynamic Equity Income Composite Benchmark (Benchmark): The Composite Benchmark is currently a blend consisting of 70% MSCI ACWI NR and 30% Bloomberg US Aggregate Bond Index TR that is rebalanced monthly. The MSCI ACWI NR is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. Net total return indices reinvest dividends after the deduction of withholding taxes, using (for international indices) a tax rate applicable to nonresident institutional investors who do not benefit from double-taxation treaties. The Bloomberg US Aggregate Index TR is an unmanaged index that covers the investment grade fixed rate bond market with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

Global Allocation Composite Benchmark (Benchmark): The Composite Benchmark is currently a blend consisting of 80% MSCI ACWI NR and 20% Bloomberg US Aggregate Bond Index TR that is rebalanced monthly. The MSCI ACWI NR is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. Net total return indices reinvest dividends after the deduction of withholding taxes, using (for international indices) a tax rate applicable to nonresident institutional investors who do not benefit from double-taxation treaties. The Bloomberg US Aggregate Bond Index TR is an unmanaged index that covers the investment grade fixed rate bond market index components for government and corporate securities, mortgage pass- through securities and asset-backed securities.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Using a currency hedge or a currency hedged product does not insulate the portfolio against losses.

Buying commodities allows for a source of diversification for those sophisticated persons who wish to add this asset class to their portfolios and who are prepared to assume the risks inherent in the commodities market. Any commodity purchase represents a transaction in a non-income-producing asset and is highly speculative. Therefore, commodities should not represent a significant portion of an individual’s portfolio.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit riverfrontig.com or contact your Financial Advisor.

Mega cap is a designation for the largest companies in the investment universe as measured by market capitalization. While the exact thresholds change with market conditions, mega cap generally refers to companies with a market capitalization above $200 billion.

Technology and internet-related stocks, especially of smaller, less-seasoned companies, tend to be more volatile than the overall market.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2022 RiverFront Investment Group. All Rights Reserved. ID 2551837

For more news, information, and strategy, visit VettaFi.com.