By Doug Benning, Vice President & Senior Research Analyst

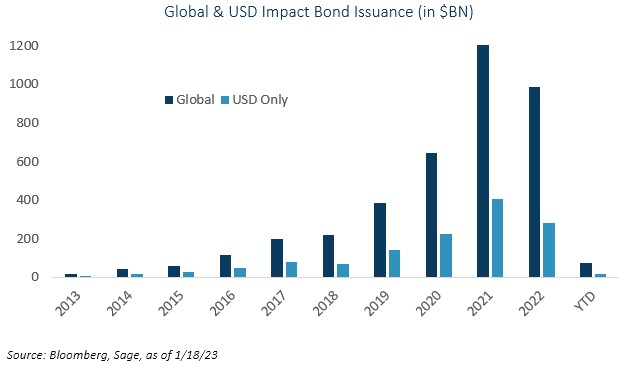

After a record-breaking approximately $1 trillion of green, social, sustainability, and sustainability-linked bonds (GSSS bonds) in 2021, the biggest impact bond story of 2022 was that new issuance fell for the first time in almost a decade. While ESG investing has come under fire from all sides in recent months, the primary culprit for the slowdown in the market for sustainable debt issuance was the same as it was for global fixed income markets overall: a surge in inflation and the Fed’s attempt to combat it by raising interest rates made it more expensive for businesses to raise capital through debt issuance.

{kind=link}

Market turmoil amid economic reopening, the war in Ukraine, and balance sheets already firmed up by the prior year’s record issuance all contributed to the conditions that discouraged borrowing in the market at higher rates this year. On a positive note, we believe that the damage in fixed income has already been done. Furthermore, it increasingly appears that we’re approaching the end of the rate hiking cycle in early 2023, leaving high-quality, long-duration bonds with a great risk/return profile going forward.

With 2022 in the rear-view mirror, some analysts are predicting a pronounced rebound in impact bond issuance in the new year. In November, Barclays predicted that 2023 issuance will match the high watermark of 2021. S&P noted in September that GSSS bonds outstanding had topped $3 trillion in 1H22 for the first time. The Inflation Reduction Act’s support for the transition to Net Zero emissions will help fund and encourage projects to decarbonize the economy in the coming decades, and it was recently reported that Bank of America has been hitting the phones to encourage impact bond issuance. Additionally, investor demand remains high for impact bonds globally despite the recent disappearance of the “greenium,” or green premium, due to a combination of greenwashing claims and tightening borrowing conditions dampening enthusiasm.

Impact Bond Universe

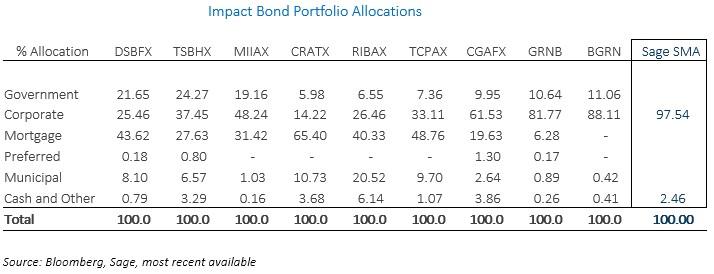

There is considerable variability in investment approaches undertaken in the impact bond space, making return comparisons difficult. The table below contains several mutual funds that market as impact bond funds, but a look beneath the hood reveals varying levels of focus for those bonds.

{kind=link}

Funds choose to report holdings with varying degrees of delay, so in this analysis we use the most recent available. The 8/1/22 prospectus for the Nuveen Core Impact Bond Fund (TSBHX), for instance, reveals that as of 3/31/22 only 41.2% of the fund’s portfolio aligned with its impact framework to provide direct exposure to impact investments. As of the 9/30/22 holdings per Bloomberg, the Praxis Impact Bond Fund (MIIAX), the Domini Impact Bond Fund (DSBFX), and TSBHX reported 18% to 23% sovereign bond allocations, vs. 7% to 8% in the Blackrock iShares Green Bond ETF (BGRN) and the VanEck Green Bond ETF (GRNB). The CCM Community Impact Bond Fund (CRATX), the Touchstone Impact Bond Fund (TCPAX), and DSBFX all reflected 12% to 17% CMBS exposure. The RBC Impact Bond Fund (RIBAX) had a 21% allocation to municipal bonds, twice as much as any other fund on the list. As of 8/31/22, CRATX was allocated 65% to mortgages, and only the Calvert Green Bond Fund (CGAFX) and BGRN had more than a 10% allocation to REITs.

As the sector distribution in the table illustrates, none of the funds in the Impact Bond universe allocates to the same types of fixed income securities or uses the same investable universe. Returns on a mostly mortgage-backed strategy will consistently differ from a mostly (or entirely) corporate bond strategy. As such, investors should conduct a deep analysis to understand how each fund is implementing their respective impact bond strategy.

Sage Advisory’s Impact Bond Strategy

At Sage, we have long incorporated ESG factors into multiple strategies, including our Impact Bond Strategy, which includes GSSS bonds available in the US market that are issued in US dollars (USD). The Sage Impact Bond Strategy is offered in a separately managed account (SMA) format that focuses on investment grade corporate bonds that have an impact bond label and are of sufficient size to ensure adequate liquidity. The SMA format allows clients customization and negotiable account minimums (offered as low as $250k) and fees. For example, accounts holding individual bonds can be used for tax loss harvesting and duration targeting, as well as adjusting credit level restrictions. The ability to customize a smaller bond portfolio can be a powerful tool for clients seeking sustainable investing options.

The Sage Impact Bond Strategy is informed by both Bloomberg and Environmental Finance Bond Database reporting and includes framework alignment with the ICMA Principles and guidelines for each member of the GSSS family, employment of second party opinions (SPOs) by providers such as Sustainalytics and ISS, and assurance made publicly available on issuers’ websites, increasingly provided by accounting firms or SPO providers.

Sage applies its ESG Leaf Score® methodology to bond issuers considered for investment, and the Leaf Scores are reported quarterly. Sage primarily invests in companies that have a Leaf Score of 3 or greater. Holdings that have a Leaf Score of 1 or 2 must exhibit strong intentionality and improving ESG characteristics, but Sage will exclude issuers that have ongoing controversies. One example is Wells Fargo, which was removed from consideration prior to its recent $3.7 billion settlement announcement for customer abuses, despite issuing multiple otherwise-qualifying impact bonds, including a $2 billion sustainability bond in August 2022.

Impact bonds tracking use of proceeds may be issued before or after completion of a qualifying project. Building a wind farm for generating clean energy or an apartment building for affordable housing are examples of projects that may be financed by green or social bonds. Projects can include planned future work as well as refinancing of projects already completed. Most frameworks that address refinancing limit the lookback period to three years or less. A complicating factor is that some impact bonds allow projects to be swapped in and out over the life of the bond if they subsequently are not found to qualify by assurance providers or at the issuer’s discretion. Quarterly reporting helps identify how much of a bond’s proceeds are allocated, and to what ends.

Increasing scrutiny in the impact bond market enables managers with robust processes to better analyze investments for suitable sustainability characteristics and avoid accusations of greenwashing. With bonds likely to offer outsized opportunity in the near-term due to the coming end of the current rate-hiking cycle, impact bonds in particular offer investors the ability to create a sustainability-focused portfolio that offers competitive returns. This is one way Sage Advisory enables clients to invest well and do good.

Source List

1) Mutua, David Caleb. Global ESG Bond Issuance Headed for First Full-Year Decline Ever. Bloomberg. Dec. 7, 2022

2) ESG Bond Weekly: Barclays Sees Issuance Bouncing Back Next Year. Bloomberg. Dec. 2, 2022

3) Global Sustainable Bond Issuance Likely to Fall in 2022. S&P Global Ratings. Sept. 20, 2022

4) BofA Reps Hammering the Phones to Push ESG Bonds. Financial Advisor IQ. Dec. 8, 2022

5) Son, Hugh. Wells Fargo agrees to $3.7 billion settlement with CFPB over consumer abuses. CNBC. Dec. 20, 2022

6) Mazumdar, Ronojoy and Subhadip Sircar. India Enters Green Bond Market With $1 Billion Debut Auction. Bloomberg. Jan. 24, 2023

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.

For more news, information, and analysis, visit the ESG Channel.