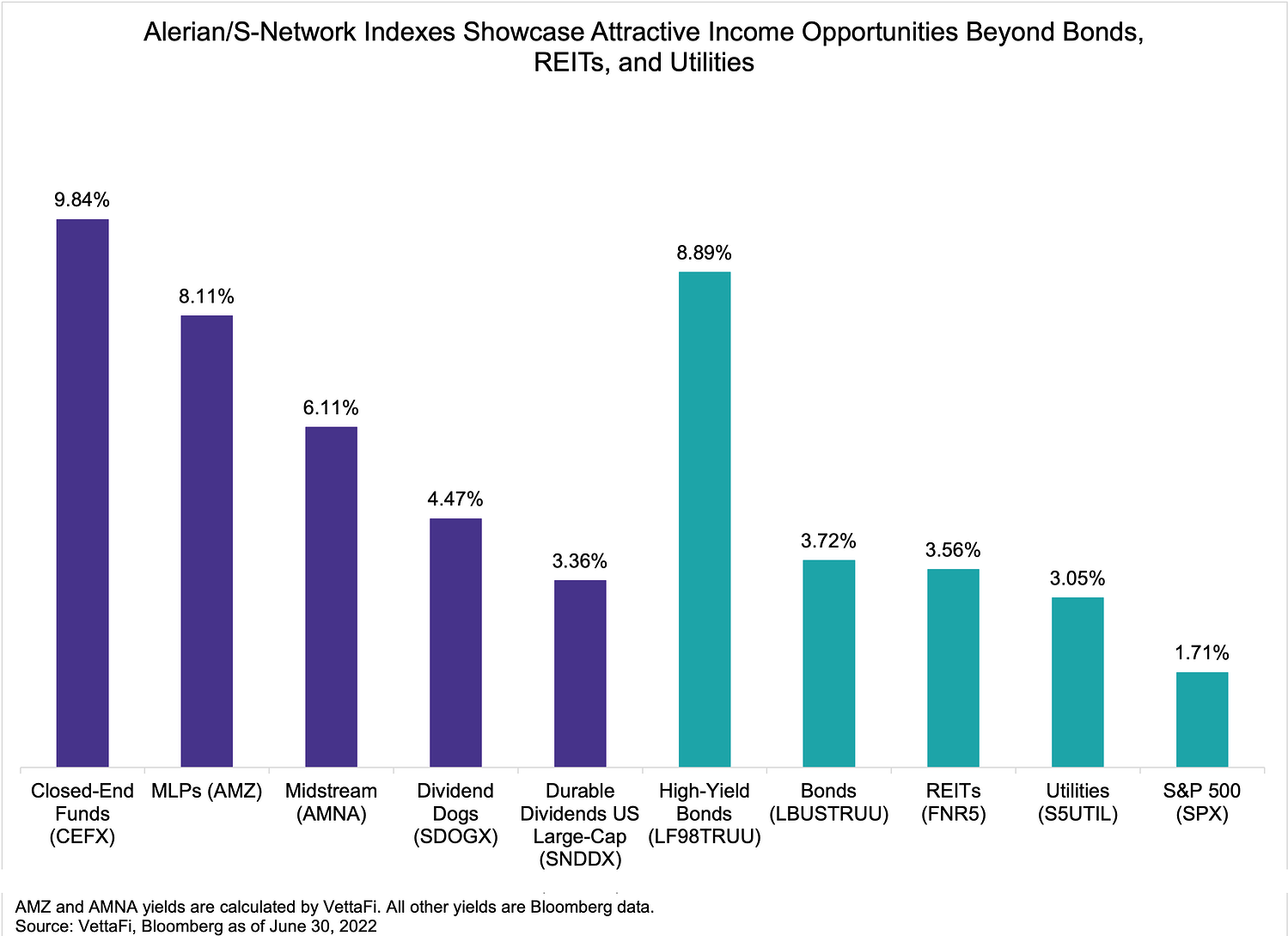

The first half of 2022 has been dreadful for investors with broad equity markets off by more than 20% as inflation has proven persistent and the prospects for a soft landing have deteriorated. The 10-Year Treasury yield has increased from 1.51% at year-end 2021 to 3.02% as of June 30. Even energy – the only sector with price gains in 1H22 – experienced pressure last month as recession concerns (and profit taking) weighed on the space. With inflation at 8.6% and yields for many equity income investments around 3%, it is clearly a challenging environment for income investors. For those looking for higher yields, recent volatility in energy could be an opportunity to enjoy attractive yields from MLPs and complement existing portfolio exposures, namely utilities.

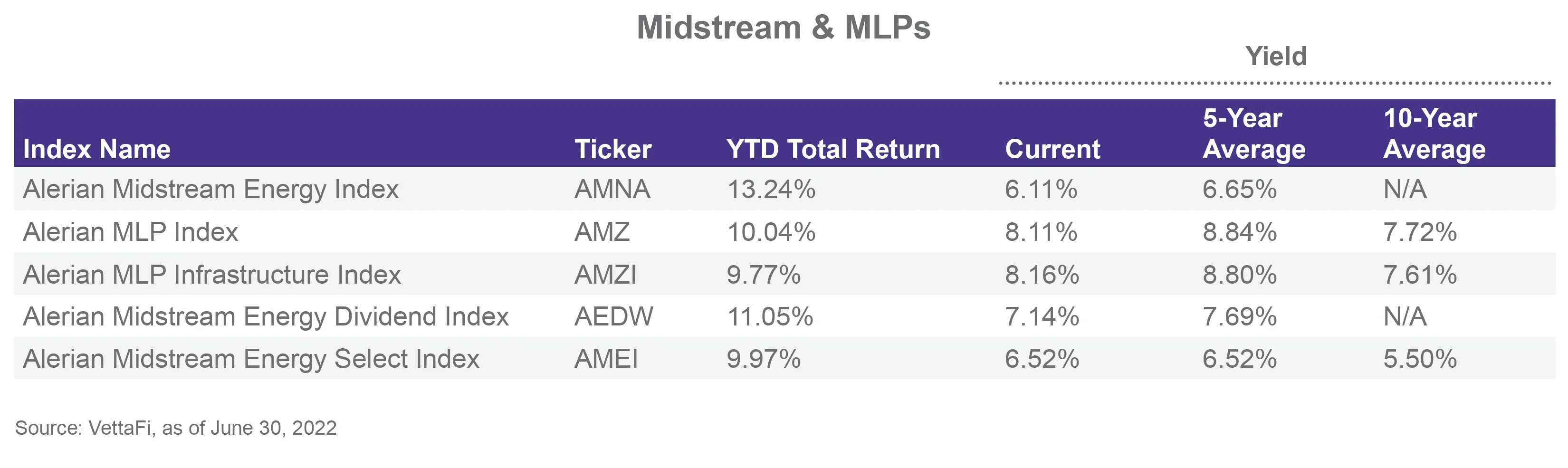

The broad energy sell-off in June has put MLP index yields above their ten-year averages for the first time since December 2021. The Alerian MLP Infrastructure Index (AMZI) was yielding 8.16% at the end of June compared to its ten-year average of 7.61%. Importantly, the outlook for MLP distributions remains strong given solid fundamentals, continued free cash flow generation, and commodity price levels that incentivize measured growth from US oil and gas producers. There have been no cuts across the Alerian energy infrastructure index suite for three straight quarters, and on a year-over-year basis, more than 80% of the AMZI by weighting has increased payouts (read more). Notably, bellwether MLP Enterprise Products Partners (EPD) announced a 2.15% sequential increase to its distribution today.

Little has fundamentally changed for MLPs over the last month, but MLP index yields are 110 basis points higher than at the end of May. The upcoming earnings season will give management teams an opportunity to highlight positive company-level trends and could help serve as a catalyst for the space. It also bears noting that MLPs (and energy infrastructure in general) should hold up better than other sectors of energy in a recession given their fee-based business models (read more).

Income investors positioning for the worst have likely already shifted more of their portfolio into utilities given their defensiveness. Utilities have been largely resilient, only down 0.56% year-to-date through June 30 on a total-return basis as represented by the S&P 500 Utilities Index (S5UTIL). However, at the end of June, the yield for utilities was practically in line with that of the 10-Year Treasury (3.05% vs. 3.02%). Investors looking for higher yields could move some of their utilities exposure to MLPs dependent on their risk tolerance. The ten-year standard deviation for MLPs is about twice that of utilities, but within the energy space, MLPs are a more defensive subsector given their fee-based business models. In other words, MLPs generate stable cash flows, but equity values can be volatile as the space largely trades more in line with oil prices and energy stocks. A 70-30 blend of utilities and MLPs would have yielded 4.58% at the end of June. Additionally, five-year and ten-year correlations between S5UTIL and AMZI are modest at 0.35 and 0.30, respectively. For investors wanting both income and more defensive positioning, complementing utilities exposure with MLPs could be an interesting solution.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB).

Current Yields vs. History

In June, MLP yields increased to levels above their ten-year averages for the first time since December 2021. Midstream and MLP yields are below their five-year averages.

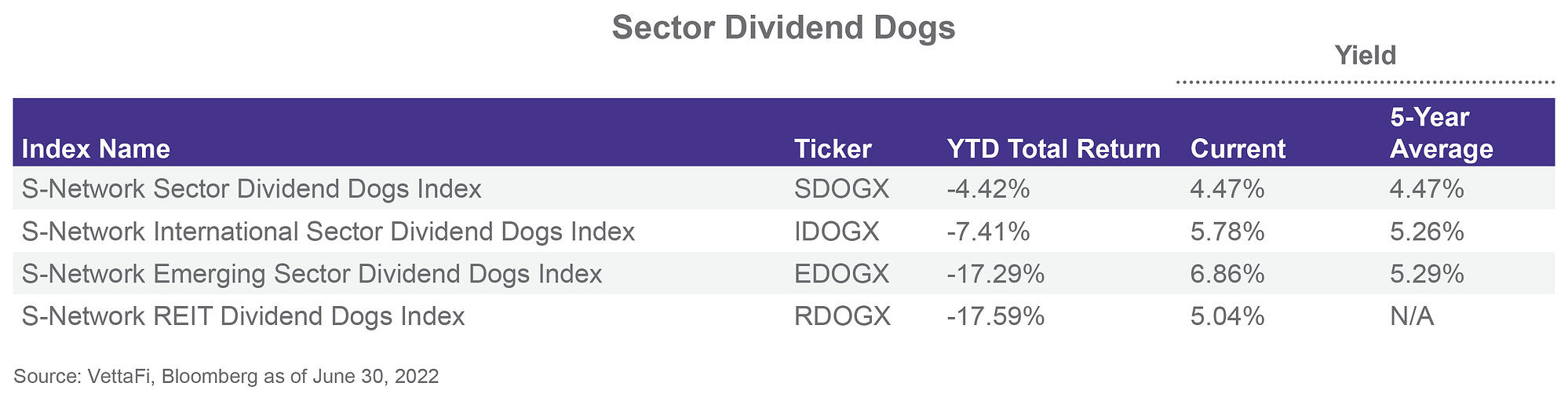

Yields for the Dividend Dogs index suite are generally above their five-year averages, except for SDOGX. SDOGX has been resilient this year thanks in part to its equal weighting scheme, which provides greater exposure to the energy and utilities sectors compared to broad equity benchmarks.

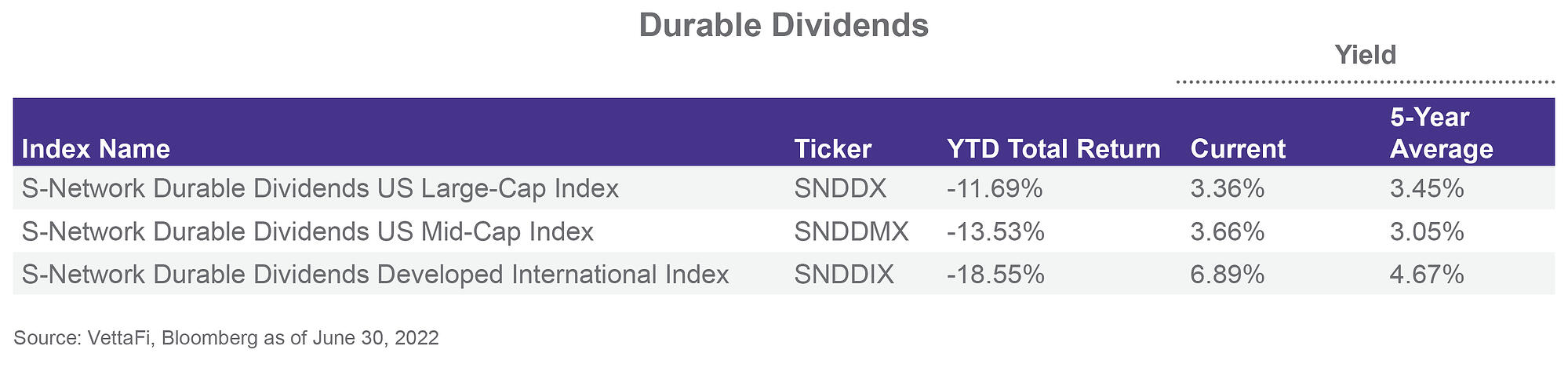

Multiple screens for dividend durability, including evaluating cash flows, EBITDA, and debt-to-equity ratios, help ensure reliable income from the durable dividend indexes.

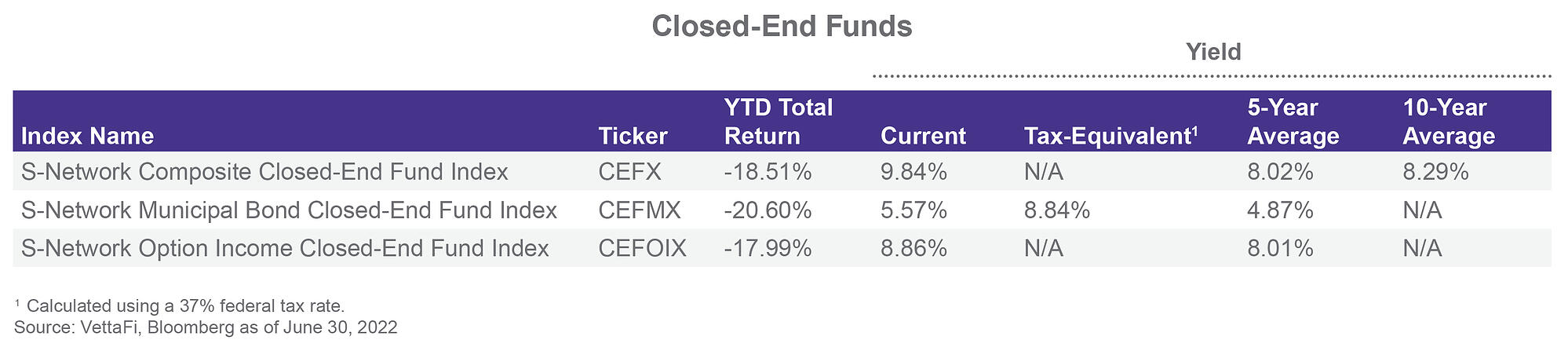

Closed-end funds have been pressured by the rising interest rate environment, and the current yields for the three CEF indexes are above their historical averages.

Related research:

Recession Fears Roil Energy: What Investors Should Know

MLP ETFs and Finding the Right Fit For Your Portfolio Goals

Income Opportunities with International Equities

Income Investments Outperforming Board Equities as Rates Rise

SDOGX Fetches Higher Yields and YTD Outperformance

Income Opportunities: MLPs, CEFs, and Return of Capital

Income Opportunities: Examining Price and Total Return in 2021

Income Opportunities: Finding Income in an Inflationary Environment