This recent bout of relative performance has been the worst since right before the 2007 bear market and then the subsequent rally off the 2009 lows. (Is this also a sign that we are nearing an equity market top similar to that of 2007? We will save that question for another day!)

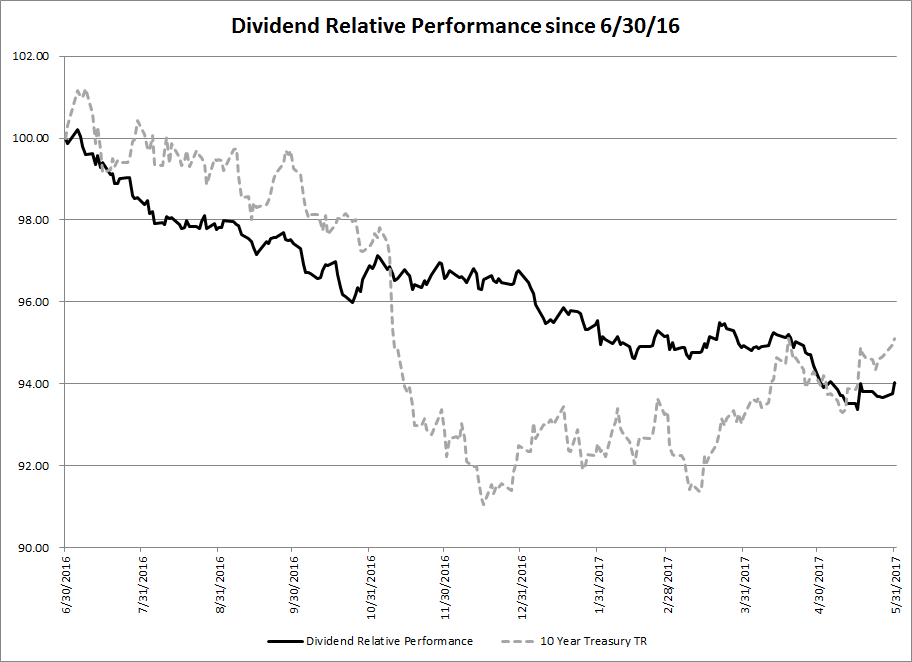

One cause of relative performance of dividend stocks/indices as compared to the broad market is their higher correlation to interest rates. This has been one cause of the dispersion since the middle of 2016, as interest rates have climbed since that point (and hence the total return of treasuries has declined). For reference, here is the same chart as above with the 10-year Treasury total return overlaid:

So while it is definitely not a perfect correlation, the two series for the most part move in tandem. So does this then beg the question of whether or not the dividend relative performance is warranted since rates have climbed since the aforementioned 6/30 date? Here is a shorter-term view of the relative performance since said date:

Unlike treasuries, the relative performance of dividends did not bottom out after the post-election spike in rates. Conversely, dividends also have not seen a turnaround in performance once rates started to fall again. So while there is some minor dispersion at the end of this chart, the performance overall is somewhat in line.

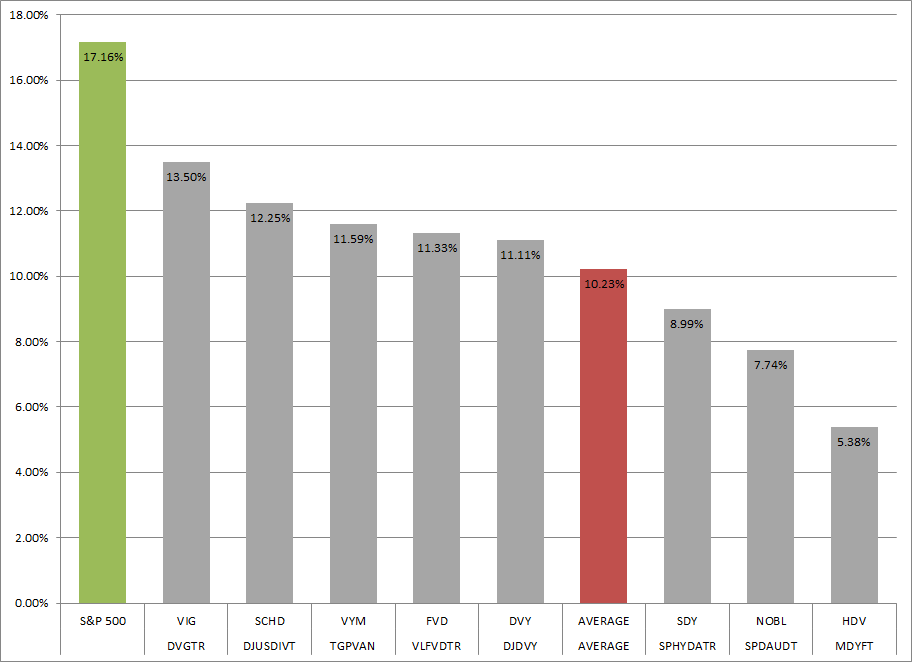

As mentioned, the above analysis was done using the average of eight different indices. Nevertheless, it is also important to note that there has been some rather large dispersion in the performance of these indices since 6/30/16.

While there are numerous differences that are causing the dispersion (e.g., GICS sector exposure, market cap, dividend yield, base index provider, etc.), it should be noted that some of these names have held up better than others. So while one of these names (or any of the ETFs available in the market) may or may not be better than another, further research is warranted on which vehicle to use if an investor thinks a move into dividend exposure is warranted at this time.

Clayton Fresk is a Portfolio Manager at Stadion Money Management, a participant in the ETF Strategist Channel.

Disclosure Information

Past performance is no guarantee of future results. Investments are subject to risk and any investment strategy may lose money. The investment strategies presented are not appropriate for every investor and financial advisors should review the terms and conditions and risks involved. Some information contained herein was prepared by or obtained from sources that Stadion believes to be reliable. There is no assurance that any of the target prices or other forward-looking statements mentioned will be attained. Any market prices are only indications of market values and are subject to change. Any references to specific securities or market indexes are for informational purposes only. They are not intended as specific investment advice and should not be relied on for making investment decisions. The S&P 500 Index is the Standard & Poor’s Composite Index of 500 stocks and is a widely recognized, unmanaged index of common stock prices. One cannot invest directly in indexes, which are unmanaged and do not incur fees or charges. Founded in 1993, Stadion Money Management is a privately owned money management firm based near Athens, Georgia. Via its unique approach and suite of nontraditional strategies with a defensive bias, Stadion seeks to help investors—through advisors or retirement plans—protect and grow their “serious money.” Contact Stadion at 800-222-7636 or www.stadionmoney.com. SMM-062017-588