Thought to ponder…

“To ‘leave the jersey in a better place’ means to work incrementally towards a better collective outcome. It means to be a custodian of the future, an architect of tomorrow, a steward of society. It means to live with respect, humility and excellence. It means mana.”

Legacy – What the All Blacks Can Teach Us About Business and Life

– James Kerr

The View from 30,000 feet

The only comparable periods for the dynamics of last week were the complete shut down of economy during the early days of the pandemic or the initial window of disarray associated with the Great Financial Crisis. Last week’s banking journey was the familiar path of crisis economics, where failing institutions mark the streets like potholes, while central banks scurry around speeding traffic, with yellow vests and shovels, dispensing an alphabet soup of asphalt to try and patch the potholes before they interfere with traffic and begin to cause accidents. To further complicate central banker’s plight as the warden of road maintenance and safety, inflation and growth data provided little reprieve, increasing the hazards of a misstep. Last week’s pace of action was so frantic a date stamp needs to be placed on any commentary, because in 24 hours it might be obsolete.

- The latest inflation and growth data shows little progress in the measures the Fed is targeting but at the margin it’s possible to tell a better story

- Like Joseph Campbell’s Hero’s Journey, most recessions have a similar story told with different plots and players

Market Technical Update – time to buy or be defensive? - The most Frequently Asked Question from client’s this week: Does the current banking crisis change the Fed’s path?

The latest inflation data and growth data shows little progress, but at the margin a better banking story

- CPI was up 0.4% month over month and 6.0% year-over-year, matching consensus estimates for a steady glide path downward for inflation.

- There was little to no progress in key areas that the Fed has stated they are targeting.

- The Cleveland Fed Median CPI increased from 7.08% in February’s release to 7.20% in March

- The Cleveland Fed Trimmed Mean decreased from 6.55% in February’s release to 6.50% in March

- The Atlanta Fed Sticky CPI increased from 6.67% in February’s release to 6.70% in March

- The Dallas Fed Trimmed Mean decreased from 4.66% in February’s release to 4.63% in March

- Core Services Less Housing (Super Core) decreased from 6.19% in February’s release to 6.13% in March

- Atlanta GDPNow estimate for Q1 2023 has accelerated to +3.2%, well ahead of the Fed’s estimates for growth which, according to the latest Summary of Economic Projections, is forecasting 2023 full-year growth to be +0.7%.

- The good news is there are signs of disinflationary momentum building in the background that should drive downward pressure in the banking composite inflation index in the coming quarters.

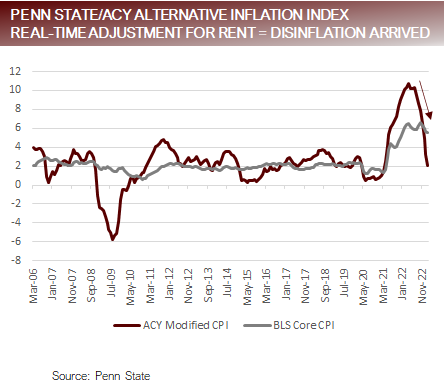

- Shelter inflation made up over 70% of the increase in headline inflation last month, but indicators of shelter inflation that lead by two to three quarters, such as Zillow and Apartment List indices, are showing disinflationary pressures.

- The Penn State/ACY Alternative Inflation Index is constructed by replacing the shelter component with a real-time indicator of shelter costs to create a modified CPI that reflects aggregate inflation without the lagging of BLS measures. The Penn State/ACY Alternative Inflation CPI measured inflation as 2.1% in its latest reading, returning to the trendline of the decade previous to the pandemic.

- Bottom line: The Fed’s case to move to a more dovish tone is complicated by persistent inflationary pressures and upside surprises to growth. There is good reason to think that as actual shelter costs propagate through the BLS inflation calculation there will be a measurable drop in inflationary pressures. The story the Fed tells will depend on which data they emphasize and how they factor in newly identified risks.

The story of inflation is about of spin – it’s possible to spin the story as inflationary or disinflationary

{kind=link}

{kind=link}

Like Joseph Campbell’s Hero’s Journey, most recessions have a similar story, different plots & players

- The Hero’s Journey, made famous by Joseph Campbell, is the story of a protagonist or antagonist who embarks on transformational adventure, and acts as the foundation for many of the stories we know and love.

The stories of recessions are similar in that they begin with a market inefficiency that creates a mispricing of assets and a supply/demand imbalance. Eventually, there is a banking catalyst that exposes a weak link (sometimes it takes more than one catalyst) that sparks a repricing of assets and normalization the supply/demand balance. - The most liquid assets are subject to the initial repricing, but as less-liquid assets are discovered or derivatives of the assets that were mispriced are discovered, the repricing continues to spiral through system. Confidence plays a major role as market banking participants become increasingly worried about contagion. The ultimate lows are always a function of time and price.

- Recent Recessions:

- Great Financial Crisis: Loose lending standards and low rates leads to a mispricing in housing.

- Dotcom Crash: Euphoric tech mania and low rates leads a mispricing in tech stocks.

- Current Recession?

- Post-Pandemic Recession: Excess cash balances and low rates leads to a mispricing in housing, while simultaneously uncovered there has been build up of duration and low-quality financial assets as a result of a decade of low zero-interest rate policy.

- Dynamics Under the Surface:

- Low rates forced investors to either increase duration or take credit risk to hit return targets. Post-pandemic, banks had too much cash on their Balance Sheets, in other words they were over reserved. They invested excess cash in long duration assets to generate yield, which caused a build up of duration on their Balance Sheets. They also loaned money, specifically to speculative commercial real estate areas and low quality CCC bank loans, because investors were demanding alternatives that generated more return in their portfolios, so their underlying loan books are littered with potentially risky commercial real estate and CCC debt.

Build up in duration and debt on Balance Sheets make them sensitive to rising rates

{kind=link}

{kind=link}

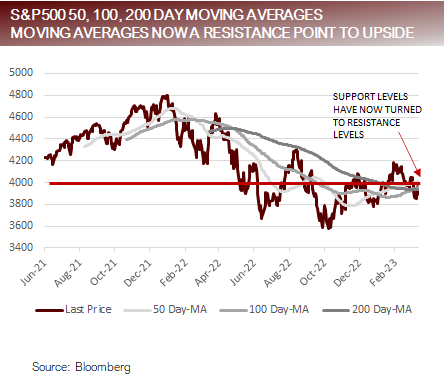

Market Technical Update – time to buy or be defensive?

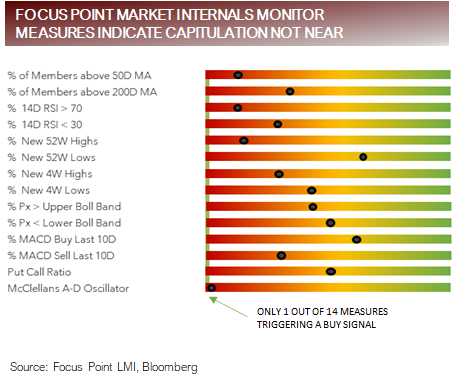

- The Focus Point Market Internals Monitor signaled oversold conditions indicating potential of a tradable low in June and October of 2022. In each of these occasions the market experienced significant rallies. Past performance is not a guarantee of future results.

- The Focus Point Internals Monitor combines 14 indicators to measure the depth and breadth of selloffs to determine if there is sufficient movement to designate capitulation and tradable low. When over half of the indicators of market internals signal deeply oversold conditions within a seven-day window the model signals capitulation and a tradable low.

- Although several measures are nearing the lower bound, only 1 of the 14 measures has signaled a tradable low in the last seven days, making us skeptical that the selling pressure in equities is over from a technical perspective.

- It should be noted that the selling pressure is being driven by fears of contagion risk in the banking system. It’s our view that the only thing may satisfy markets will be a government intervention program sufficient to provide confidence that there is a backstop against systematic risk. Government intervention may happen before market depth and breadth indicators trigger a tradable low.

Market action indicates downward trend with signals of capitulation not near

{kind=link}

{kind=link}

FAQ: Does the current banking crisis change the Fed’s path?

- At the highest level, the Fed needs to focus on three mandates: Financial Stability, Price Stability and Full Employment.

- Prior to the realization of the issues in the banking system the Fed was trying to calibrate their model based on balancing Price Stability and Full Employment. They must now add and account for a new variable, a potential banking crisis that calls into question Financial Stability, which will force them to recalibrate their models and views.

- Returning to first principles, what is the Fed trying to accomplish: Cool the economy to slow inflation.

- Forces at Play

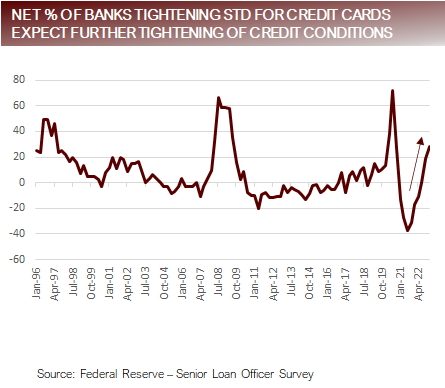

- Restrictive Force: Higher rates and QT now combine with a confidence crisis that will likely drive banks to further tighten lending standards and businesses and consumers to retrench as they worry about bigger problems than buying a third flat screen TV for their spare bedroom. Do you think anyone who had an account at SVB, Signature bank or Credit Sussie is worrying about hiring new employees or capex?

- Stimulative Force: The Fed has already added $152.85b of liquidity to the system through the Discount Window and made available $25b through the Bank Term Funding Program set up to allow troubled banks to loan their assets to the Fed at par to avoid having to reprice them and have them impact capital ratios. These are stimulative measures, viewed as QE that is offsetting the impacts of QT.

- Bottom Line: It’s complex to try and separate and measure the stimulative forces applied as a result of the Fed’s emergency liquidity facilities put in place over the last week from the restrictive forces anticipated from bank tightening and business and consumer retrenchment likely to take place as a result of the banking crisis, but it’s likely the latter will cause a significant slowing of the economy. The big question is – Will these new restrictive forces be enough to offset the inflationary pressures and growth dynamics currently in the system in the face of a Fed who will increasingly find it difficult to continue raising rates and conducting QT to combat inflation and slow growth?

Markets are pricing a dramatic economic slowdown and rate cutting cycle driven by banking crisis

{kind=link}

{kind=link}

Putting it all together

- The current bout of inflation was caused by too much money, fueled by government stimulus programs, combined with cheap debt, fueled by the Fed, while supply chains were shut causing access to goods and services to be limited. Each time it looked like there is a path to lower inflation, a new deterrent to disinflationary forces rears its ugly head.

- Persistent Supply Chain Challenges – Ends Fed hopes for “transitory” inflation

- Russia invades Ukraine – Drives spike in energy prices and friction in global trade

- China zero-COVID Policy – Prolongs supply chain difficulties

- Banking Crisis – Forces Fed to reduce hawkish position to reduce pressure on banking system

- The hiking cycle is entering a new, more complicated phase because it’s becoming apparent that excess capital and low rates created a Duration Bubble along with the potential for a low-quality Credit Bubble.

- The last two week’s developments have shined a spotlight on underestimated risks lurking in the financial system.

- Banks and financial institutions are holding vast amounts of long duration paper on their Balance Sheets with large mark-to-market losses.

- Regional banks are especially exposed because of their lack of regulatory oversight, relatively inexperienced management teams and lack of systems to track and understand risks.

- Banks with less than $250b in assets, who were less regulated, account for almost half of commercial and industrial lending and over half of commercial real estate lending. With increased worries about their Balance Sheets, they are likely to severely limit access to credit in the coming months.

- Up until two years ago if a CCC borrower needed to refinance, the capital markets were open for business and rates were likely lower than at the original issuance. With over 40% of the Russell 2000 running business that are losing money, as these borrowers need to refinance, they may face challenges with access to banking capital markets and pricing may make business model untenable.

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at info@focuspointlmi.com

Copyright 2023, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

Important Disclosures

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied. FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.